by Dr. Chris Kacher

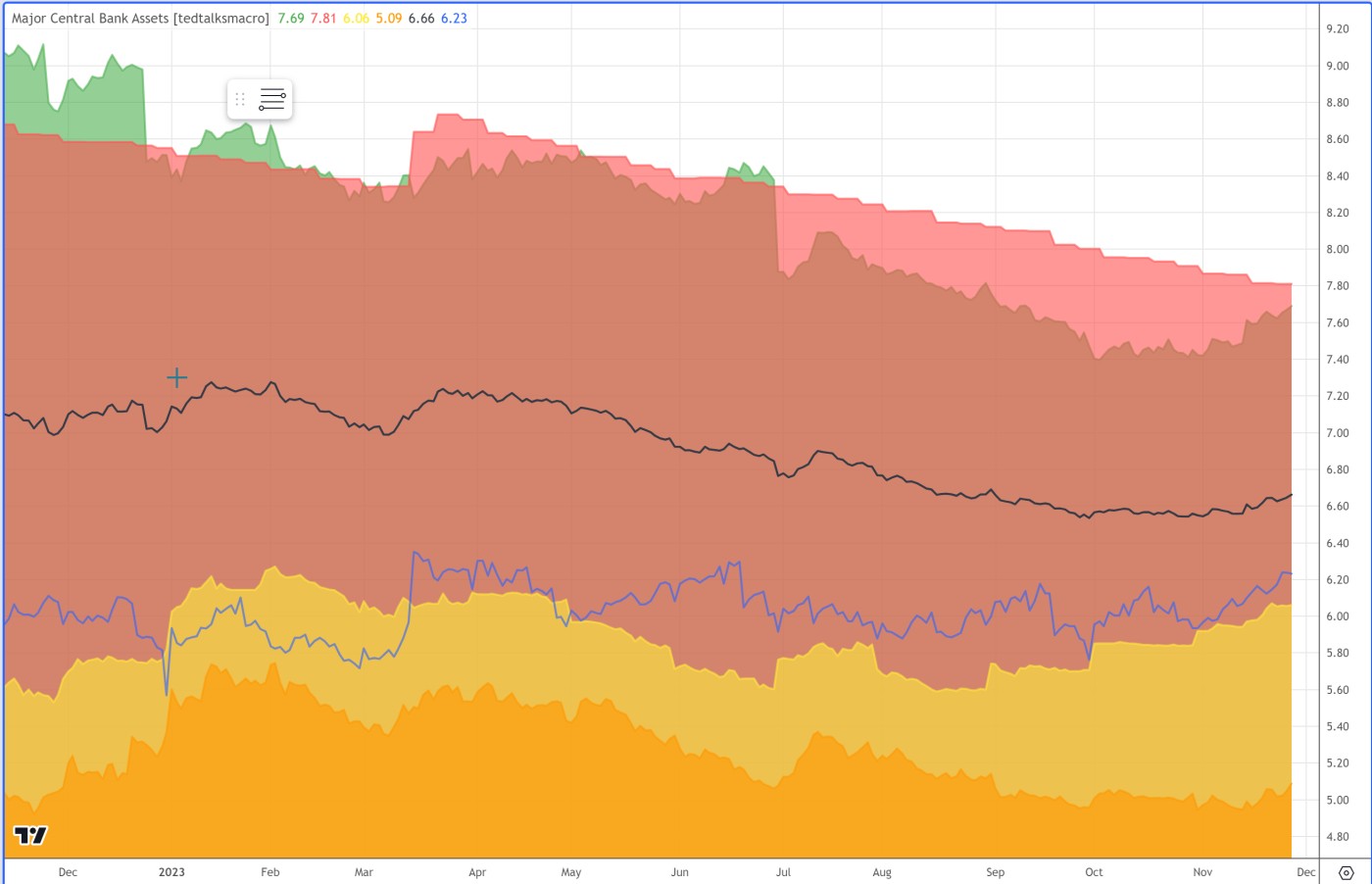

Liquidity on the rise

Net liquidity continues to rise. This is the chart of net RRP and TGA balance changes. Fed's balance sheet -TGA - RRP = net liquidity. This potentially bodes well for stocks and cryptocurrencies as well as bonds and hard assets such as real estate.

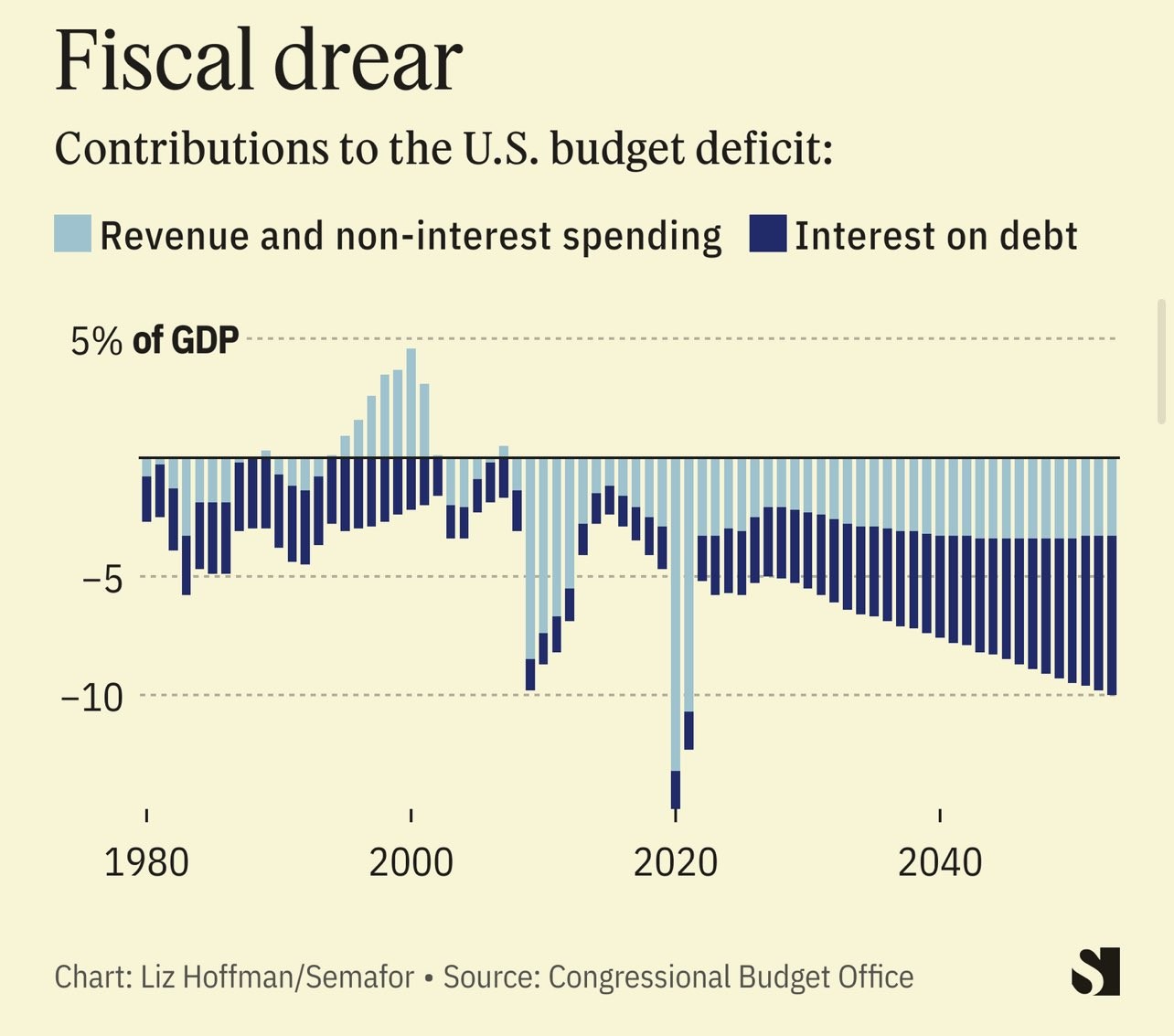

Already running huge deficits, the only way for the US Treasury to pay the interest — along with ambitious spending programs like the CHIPS Act and student-loan forgiveness — is to keep borrowing.

We are also seeing liquidity rise across all major central banks (as represented by the black line).

ECB'S Lagarde said they will re-examine their proposal to keep their pandemic emergency purchase programme (PEPP) active until the end of 2024. PEPP is a non-standard monetary policy measure initiated in March 2020 to counter the serious risks to the monetary policy transmission mechanism and the outlook for the euro area posed by the coronavirus (COVID-19) outbreak, but continues to be used in a stealth QE manner.

How much further can the MMANGA (Microsoft, Meta, Apple, Netflix, Google, Amazon) tech AI-meme stock juggernauts run? With their P/Es and current market caps such as Apple at $3 trillion, how can they continue their huge run ups in price? There is no room for disappointment. NVDA's earnings report came in ahead of expectations yet it sold off. The market is probably the most unforgiving at the current time. Nevertheless, because these massive companies have monopolies of sorts along with increasing stealth liquidity by the Fed, their run could continue. Markets are sometimes irrational thus explains bubbles where names grow to ludicrous valuations.

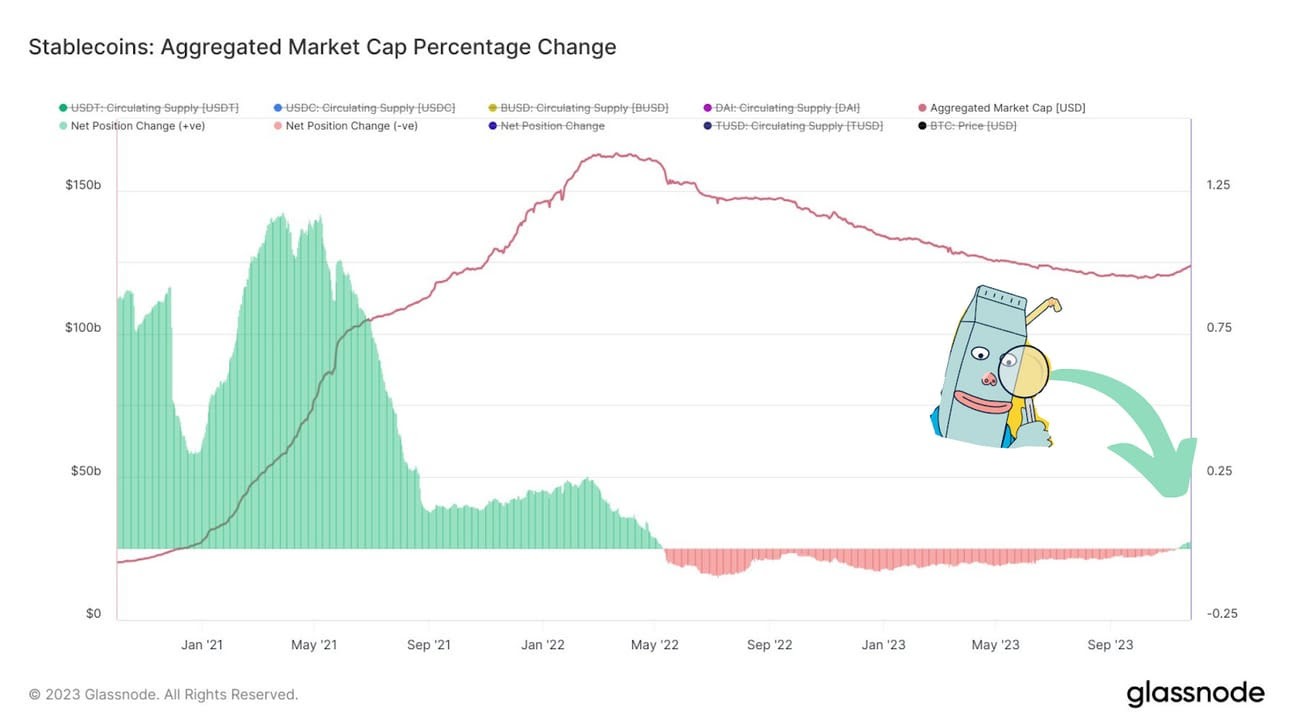

Over in cryptocurrencies, stablecoin supplies are also up $2.2B over the last 90 days. Earlier this month, the 90-day change in stablecoin supplies flipped positive. It was the first time that’s happened since May 2022.

| ||

Recession postponed?

Many continue to predict recession. The price of oil continues to fall. The higher the price of oil, the slower an economy grows. Like all voters, American voters vote on the basis of recent economic performance. According to statistics from the US’s National Bureau of Economic Research (NBER), since the end of World War I in 1918, the sitting US President has won re-election 11 times out of 11 if the US economy was not in recession within two years of an upcoming election. However, sitting US presidents who went into a re-election campaign with the economy in recession won only 1 time out of 7. In consequence, the Democrats will do all it takes to postpone recession beyond the voting day of November 5, 2024. This means more stealth QE to prop up the economy.

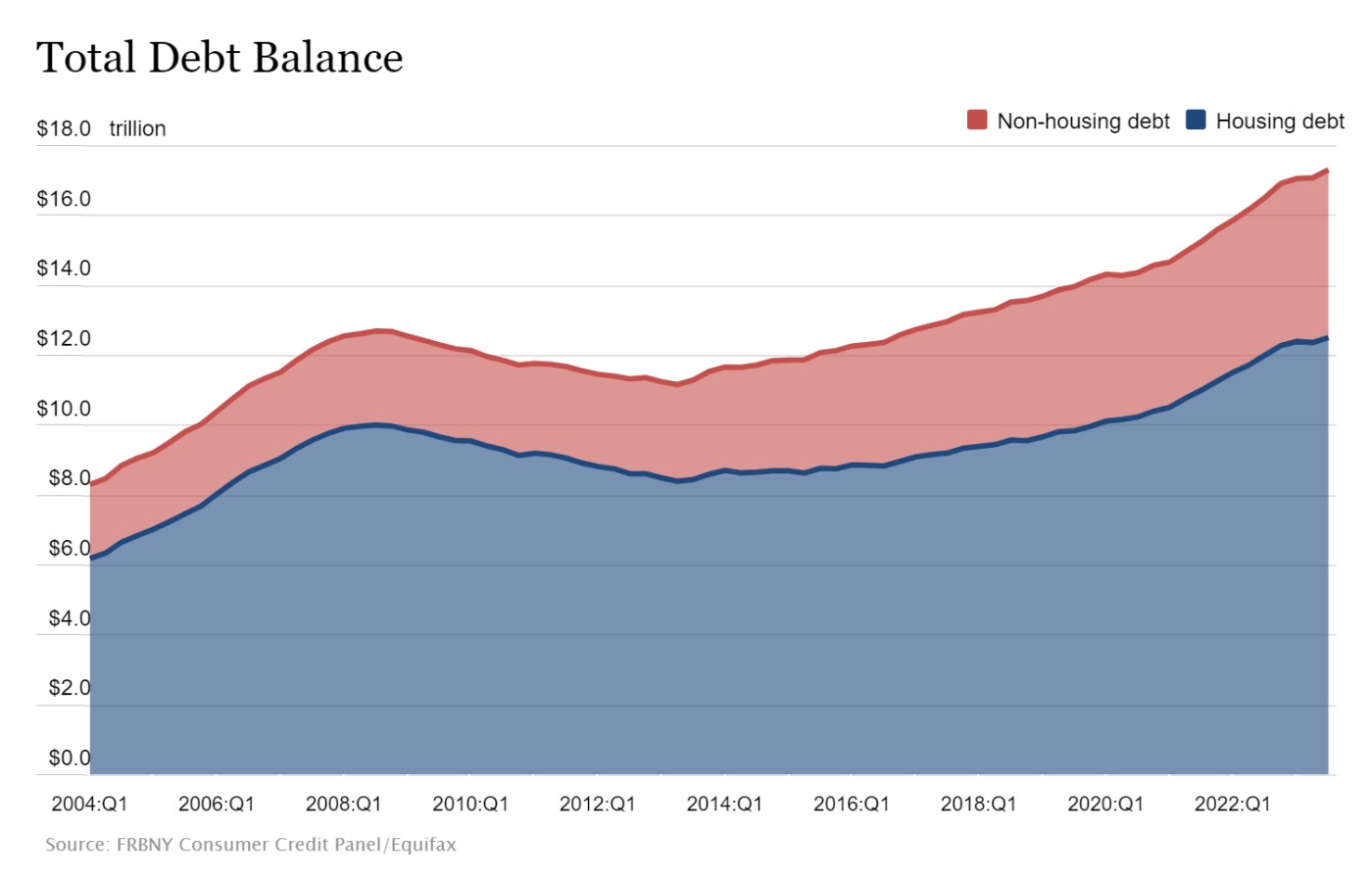

GDP came in at 4.9% in the prior quarter ahead of the 4.7% estimate, then was revised higher to 5.2%. What recession? The sharp increase was due to contributions from consumer spending, increased inventories, exports, residential investment and government spending. Black Friday was more robust than ever as the retail public continues to spend. Consumers spent a record $9.8 billion online on Black Friday, which marks a 7.5% increase over the year prior. This seems to go against the record levels of credit card debt which stand at $1.2 trillion. Household debt in total rose to $17.29 trillion led by mortgage, credit card, and student loan balances. Mortgage balances increased to $12.14 trillion and student loan balances to $1.6 trillion. Auto loan balances increased to $1.6 trillion, continuing the upward trajectory seen since 2011.

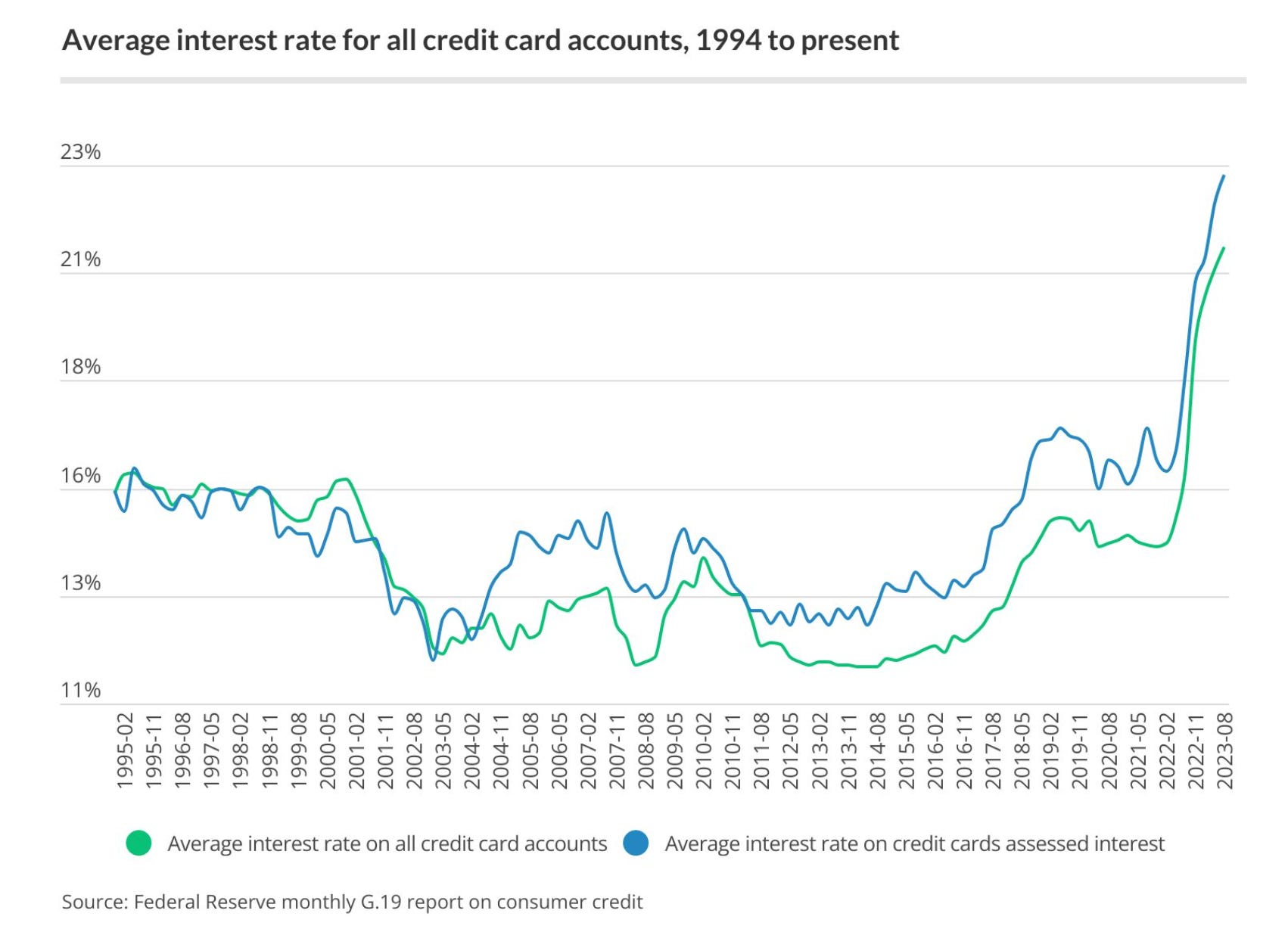

Also, we have record levels of credit card interest. We have become a nation of borrowers. There is no fiscal discipline at the government or individual level on average.

|

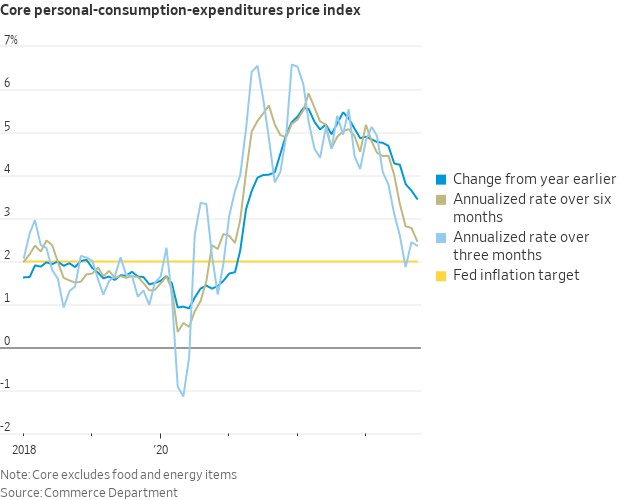

With record levels of household debt and government debt, the Fed will likely have to helicopter in money to Americans once again to avoid a cascading tsunamic wave of defaults as inflation in the things people need the most including food, energy, healthcare, and education continues to remain stubbornly high despite the CPI, PPI, and PCE all showing lower rates of inflation in other less critical areas. The core PCE index rose 0.16% in October, as expected, and was up 3.5% from a year earlier. Notably, the 6-month annualized core inflation rate fell to 2.5%, which is not far from from the Fed's 2% target. The 6-month annualized rate 6 months ago was 4.5%, a dramatic improvement.

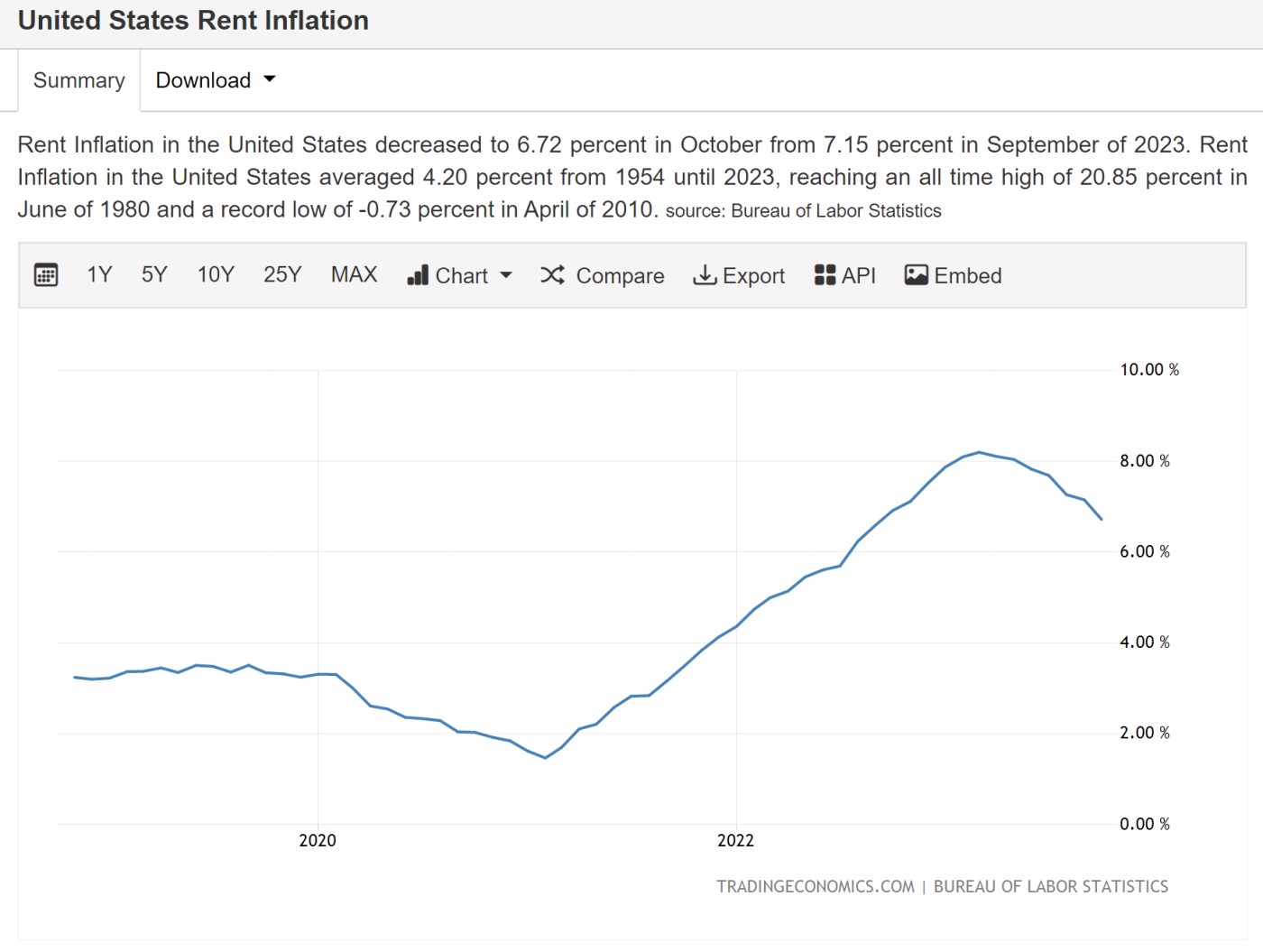

While rents have started to subside, they are still far higher than they were in 2020-2021. Property prices have actually increased overall in 2022-2023 in the US and UK due to those who are holding onto their properties because they financed at low mortgage rates prior to the aggressive rate hikes that began in early 2022. So while demand fell off due to higher mortgage rates, so did supply.

Suffice to say that the rise in US and global liquidity should continue to rise in the ensuing months which has a tendency to act as a tailwind for hard assets such as real estate, precious metals, stocks, bonds, and cryptocurrencies. In the meantime, nothing goes up in a straight line so we will also be on the lookout for opportunistic plays on the short side. The jobs report comes out Friday December 8. Should the unemployment rate tick appreciably higher, that would be another clue that unemployment is starting its accelerated ascent, though with all the ongoing manipulation of data, this rate is likely to be fudged downward to keep up appearances that all is well. Doctored data anyone?