by Dr. Chris Kacher

Stocks becoming cheaper?

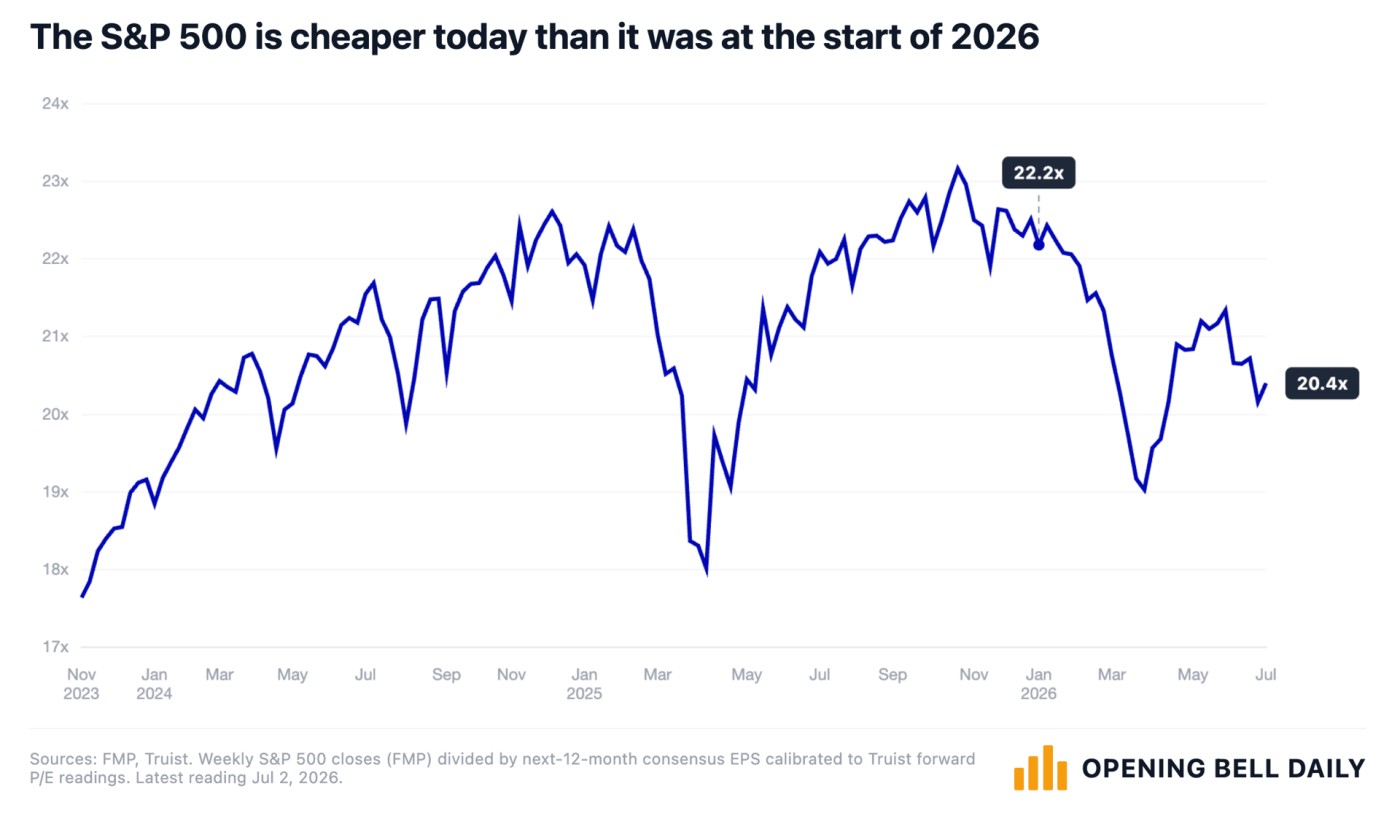

Investors warning of another dot-com-style bubble are focused on prices while ignoring earnings. Despite the S&P 500 rising more than 9% year-to-date, its forward P/E ratio has actually fallen from 22.2x to 20.4x. Earnings estimates have grown roughly twice as fast as the index itself, meaning the market is getting cheaper on fundamentals — not expanding multiples. In fact, the S&P 500 now trades at a similar multiple to May 2024, yet the index is over 40% higher. The “bubble” many fear is becoming cheaper, driven by strong earnings growth rather than speculation.

The AI Bubble Investors Should Worry About Is in Analyst Spreadsheets

Many have been concerned that stocks are way overvalued, but the current AI-driven market rally is **not** repeating the extreme valuation excesses of the dot-com bubble. Instead, the real risk lies in **overly optimistic earnings forecasts** baked into Wall Street models. Current stock prices are relatively reasonable, while analyst projections for future profits (especially in semiconductors and tech) have reached historic highs. This mismatch suggests the potential "bubble" is confined to spreadsheets rather than actual market prices.

Key Data Points

- **Analyst optimism at record levels**:

- Long-term S&P 500 earnings growth forecast raised to an all-time high of **25.5% per year**.

- Semiconductor industry projected to maintain a record **50.3% profit margin** (more than triple the broader market).

- Tech earnings estimates for the next 12 months raised by nearly **40%** this year.

- **Current valuations remain tame**:

- Tech stocks: **22.2x** forward earnings.

- S&P 500: **20.4x** forward earnings.

- Semiconductor stocks: **18.4x** forward earnings (actually cheaper than the broader market).

- **Historical comparison (Dot-com peak in March 2000)**:

- Tech: **55x** forward earnings.

- S&P 500: **25x** forward earnings.

Analysis: Earnings Momentum vs. FOMO

Veteran strategist **Ed Yardeni** highlights that analysts are assuming the semiconductor industry has become a "secular grower" capable of sustaining extraordinary margins indefinitely — a bold claim given its historical boom-bust cycles.

Unlike the dot-com era, which was driven by pure **FOMO (fear of missing out)** and sky-high valuations with little earnings to back them up, today’s market is powered by **fabulous earnings momentum** in forecasts. Actual stock prices have not run ahead of these expectations — in many cases (especially chips), they are trading conservatively relative to the projected growth.

AI adoption is happening faster than the internet did, with integration into businesses occurring almost immediately. This could justify stronger growth, but it also increases the risk if forecasts prove too rosy.

Nevertheless, the continued selloff after Samsung’s disappointing earnings (memory margins and guidance missed) is dragging the whole chip sector (MU, NVDA, AVGO, ASML, etc.) lower.

Risks and Implications

- **If positive forecasts are wrong**: A slowdown in AI spending or failure to deliver on margin/earnings growth could trigger an even sharper correction, even at current "reasonable" valuations, so obeying your sell stops is key so you step aside.

- **If forecasts are right**: The market has room to run, as current multiples are not stretched. The further AI-related stocks fall, the better the bargain.

The data suggests any bubble is more likely in **spreadsheet assumptions** than in today’s stock prices.

Semiconductor stocks are delivering some of the strongest earnings in the industry’s history, yet many names—including Nvidia, Micron, SNDK, Samsung, and SK Hynix—remain flat or well off their highs, creating a clear disconnect between fundamentals and price action. Nvidia, for example, just reported $81.6 billion in quarterly revenue and is now trading at its lowest forward P/E since 2019, roughly in line with the broader market. The same pattern holds across memory names, where explosive growth has been met with sharp pullbacks. This isn’t a sign of deteriorating business trends. Rather, these stocks had already priced in near-perfect outcomes after massive runs, so even blowout results are triggering profit-taking and hesitation from new buyers. With hyperscaler capex still projected to approach $1 trillion in 2027, the current compression in valuations looks more like a healthy reset than a fundamental shift in the AI investment cycle.

Still, investors should monitor analyst revisions closely rather than panic over current valuations. The AI trade looks more grounded in expected fundamentals than the dot-com bubble ever was — but those fundamentals are extremely aggressive and priced for perfection. Prudent investors will focus on companies actually delivering revenue and profit growth today, not just those with the most optimistic long-term models.

Timeframe

Many top performing AI-related names have moved up 3-4x in just several weeks such as MU, SNDK, ALAB, and CRDO. While these names lost nearly one-quarter to one-third from peak such as SNDK shown below, you probably sold if you used the 10-dma or 20-dema, or are still sitting if you use the 50-dma which it has yet to violate. The 7-week rule works on both the 10-dma and 20-dema, depending on your time horizon. Watch for potential shorts or longs in these top performing names as they navigate their major moving averages such as SNDK with its 50-dma. It has rocketed so has a long way to fall if fundamentals change.

On the other hand, despite recent weakness in semiconductor stocks, leading metrics from AI companies remain supportive of further upside. The major hyperscalers are guiding for very strong capital expenditures in 2026, with combined spending from Amazon, Microsoft, Alphabet, and Meta expected to reach $630–750 billion — representing significant year-over-year growth. A large and growing share of this capex is directed toward AI infrastructure, including chips, data centers, and high-bandwidth memory. Analysts have continued to revise these spending forecasts higher, and many describe the AI buildout as a multi-year cycle rather than a short-term spike. As long as these elevated investment levels hold, semiconductor demand should remain robust even if the pace of growth moderates from prior extremes. A P/E that is not terribly high further stokes the flames or at least removes the argument that stocks are way overvalued.

That said, the recent weak guidance from Samsung, Micron (MU), and Western Digital (WDC) has been a concern but given the above, does not necessarily signal that semiconductor stocks have topped. These companies are heavily exposed to the memory cycle, which is the most volatile and cyclical segment of the industry. After delivering massive gains over the past year, expectations had become extremely high, making it easier for even solid results to disappoint on guidance. Memory stocks have historically experienced sharp pullbacks and cautious outlooks during bull markets, only to recover as demand reasserts itself. More importantly, the broader AI infrastructure story remains supported by very strong hyperscaler capital expenditure plans for the remainder of 2026 and 2027, suggesting that any near-term softness in memory may reflect short-term digestion rather than the end of the cycle.