by Dr. Chris Kacher

Bulls vs bears

We have a number of metrics at bullish tipping points.

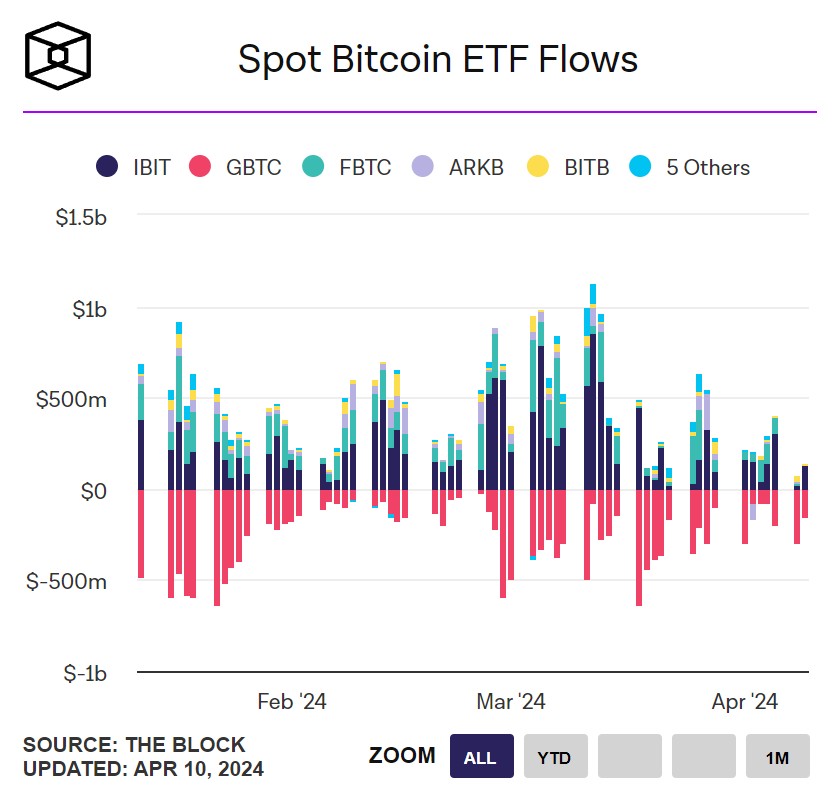

=The Grayscale GBTC selling is waning slowly though increased during the recent selloff in Bitcoin. Meanwhile, the Bitcoin spot ETF inflow continued to increase up until the Bitcoin selloff. Over time, as more institutional funds adjust their mandates to include 1-2% of Bitcoin in their portfolios, the net effect should be increasing net inflows into Bitcoin.

=Despite decreasing global liquidity since the start of the year, stocks and Bitcoin have trended higher albeit in a sloppy manner. This is due in part to the Fed tapering the taper, ie, slowly the pace of tightening. Further, stealth QE is at hand as $1 trillion gets created roughly every 100 days to fund war support efforts, defense spending, debt interest, and unfunded liabilities among other factors. A $1.2 trillion spending package was recently approved. The debt-to-GDP ratio hit its all-time record of 113% by the end of World War 2, current debt accounted for 124.3 % of the country's Nominal GDP in Dec 2023. Other countries have greater debt on their books. In consequence, record levels of debt interest must be serviced which forces all central banks to create more fiat which degrades all currencies around the globe. The US dollar still remains the champ by far. The long term rising value of hard assets, real estate, precious metals, stocks, and Bitcoin is a direct reflection of this degradation in buying power.

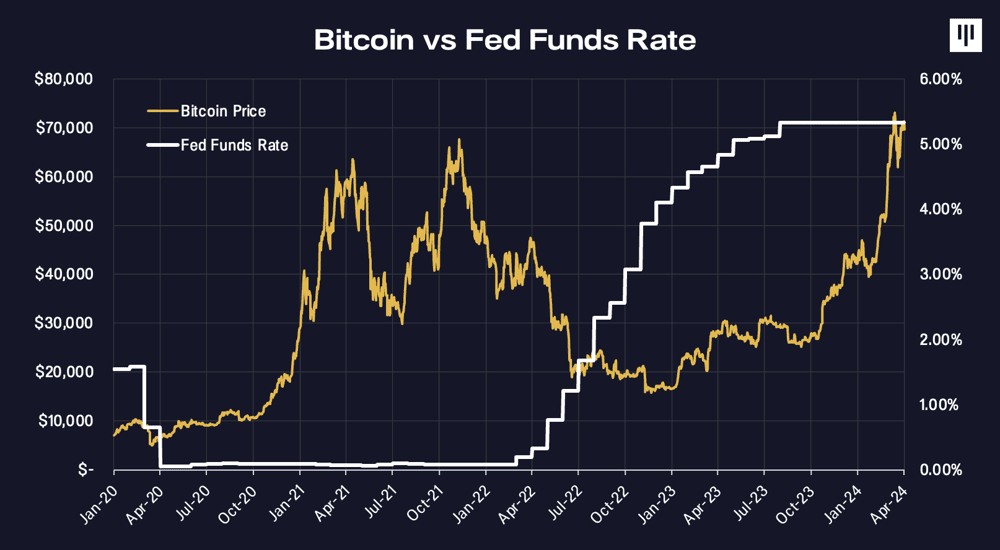

Jamie Dimon, CEO of JPMorgan Chase, recently indicated in a shareholder letter that the resilience of the US economy could "lead to stickier inflation and higher rates than markets expect." This helps partially explain why precious metals have been rallying hard as investors brace for inflationary pressures. If there are any rate hikes instead of cuts, this could induce recession thus the concern is that stocks and Bitcoin would fall. But over the past couple of years, as interest rates have risen, Bitcoin has been able to rally. Rates rose all the way through Aug-2023 yet Bitcoin started rallying well ahead of that in late 2022. But the economy was able to withstand rate hikes. With rates at current levels, any delay in rate cuts or worse, a rate hike, could upset the economic apple cart. That said, we need not try to make predictions. We will see the signs of a slowing economy in price/volume action of leading stocks and major indices so we dont need to rely on doctored data.

=The economy remains deceptively healthy which is what matters to markets. GDP, inflation, and employment data remain favorable for now. The question is when will recession hit? With stealth QE and any subsequent black swan QE, recession may continued to be postponed for longer than expected. These days, I wouldn't be surprised to see the Fed justify more QE if the economy starts to falter. Metrics can be explained in such a way to create a false black swan. Further, the Fed relaxed capital requirements on banks despite politicians calling for banks to hold more capital so that the regional banking crisis of early 2023 would not repeat itself. Obviously, the banks lobbied hard to nullify these higher capital requirements. They had a good argument. If Yellen wants us to buy questionable government bonds, then we can only do it profitably with infinite leverage. The Fed doesn’t print the money, but rather the banking system creates the credit money out of thin air through fractional banking and purchases the bonds which then appear on their balance sheet. Banks now can hold US Treasurys in the trillions of dollars needed to finance the US government deficit on a go-forward basis since they are required to put no money down.

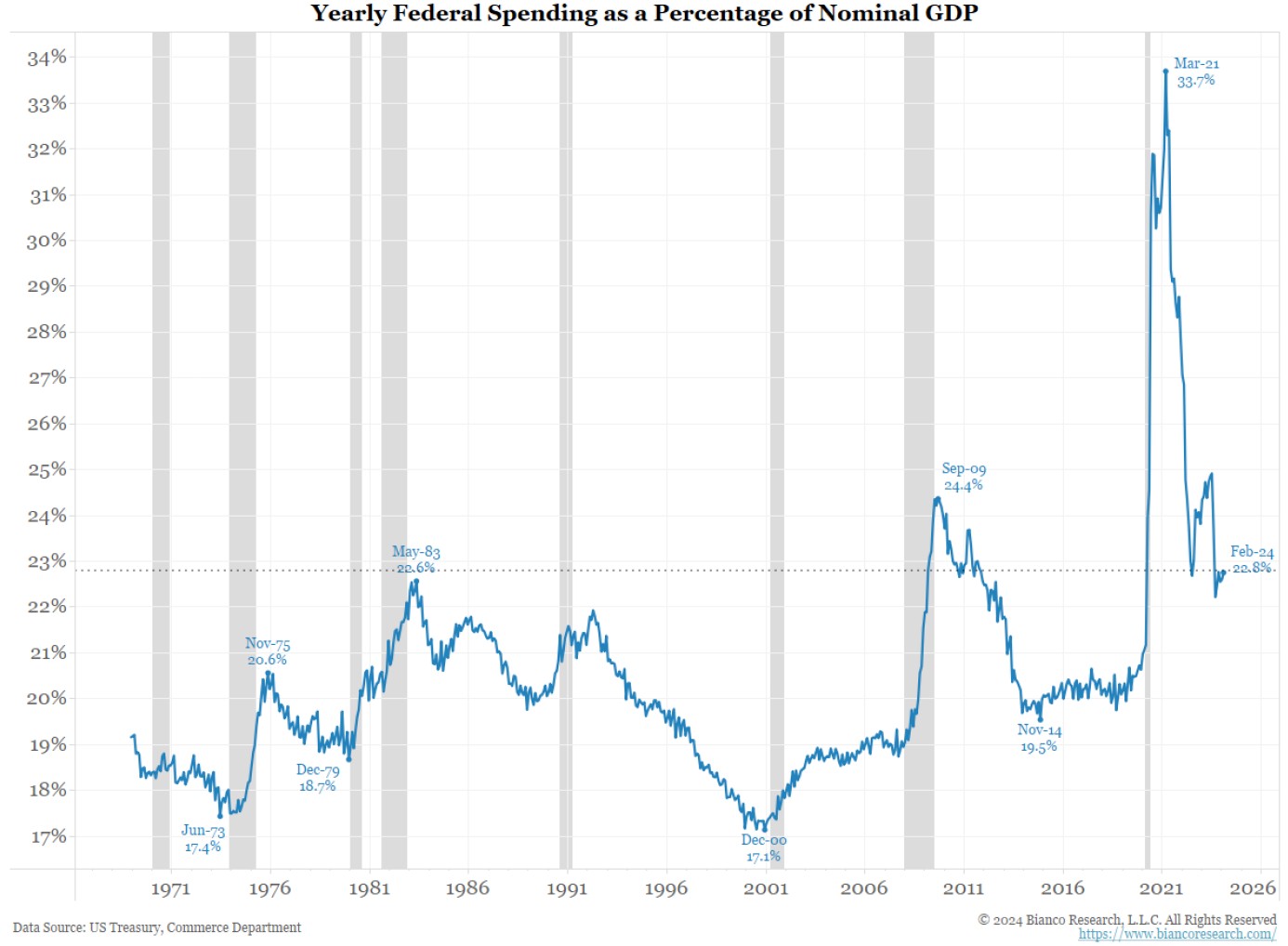

It's clever tricks like this that clearly show the profligate spending of the US Government as evidenced by the record-high deficit. The two recent periods where deficit spending was higher were due to the 2008 Great Financial Crisis and the COVID lockdowns. The US economy is growing, but the government is spending money like it's in an economic depression. This seems to be the new norm. Yearly federal spending as a percentage of nominal GDP stands at 22.8% despite the "strong" economy compared to prior cycles where since 1971, it ranged typically between 17-20%. Taking the dollar off the gold standard in 1971 enabled the Fed to create money out of thin air with ease.

|

=The Swiss rate cut which suggest future rate cuts by central banks. That said, with inflation stubborn and the economy relatively strong, the number of rate cuts has fallen from 7 at the start of the year to 1 or 2 today, so perhaps we will only get one cut by the end of the year as suggested by some Fed members. Of course, it all remains doctored data dependent.

=A number of bullish events await: the Bitcoin halving is due on April 19, S2F (stock-to-flow) trends, and the Fed/Yellen put among other factors.

What about bearish arguments?

But some ask what bearish events have been overlooked? The warning signs would be a faltering economy with no QE to the rescue, more pronounced diminishing global liquidity, a reacceleration in inflation, and major central banks becoming more hawkish. Ultimately, it is the price/volume action of leading stocks and major averages that define the major trend. In cryptocurrencies, it is the price/volume action of Bitcoin which guides all other cryptocurrencies. Both correlate heavily when it comes to macro events such as overall liquidity, recession probabilities, and interest rate direction.

Also, Arthur Hayes however has written the precarious period for risky assets is April 15th to May 1st. This is when tax payments remove liquidity from the system, QT rumbles on at the current elevated pace, and Yellen has yet to start running down the Treasury General Account. This could cause a setback in markets. After May 1st, the pace of QT declines, and Yellen gets busy cashing checks to jack up asset prices. In the long run, expect to see continued asset inflation sponsored by Fed and US Treasury financial shenanigans.