by Dr. Chris Kacher

We have discussed why we have stealth QE due to unfunded liabilities and servicing the onerous debt among other factors. But there are additional incoming costs which are massive. As Ray Dalio has said, "If you then take into consideration the climate issue—one way or another, that’s estimated to be about $8 trillion a year, which is required. We’re not going to spend that. We’re spending about one-sixth of that, which means also one of the reasons we’re not anywhere near approaching holding temperature increases at 1.5 degrees Celsius. That’s 8% of world GDP; that’s a lot of spending. And then there’s the North-South issue. And if you just take what is projected and then you apply the debt service payments to that—the maturity of the debt and the amount of interest payments that has to be on that debt—that is creating a classic squeeze. In other words, I’ve seen this repeatedly happen throughout countries."

Since we will fail to hold temperature increases at 1.5 degrees Celsius, climate is going to create more droughts, floods, and pandemics as they have throughout history which will cost huge sums.

We also have a world of greater conflict. Geopolitical tensions and wars are looking to spread. Such conflicts themselves drive the creation of fiat. The US debt-to-GDP hit record highs during World War II of 113%. Only today has this number been eclipsed to nearly 125% where it currently stands.

Soaring precious metals

The fear trade has emerged once again with soaring gold and silver prices. Geopolitical eruptions, now with Iran in the fray, may be pushing gold higher while silver follows along. Iran may have been buying gold ahead of the attack knowing there would be severe financial sanctions from the US.

We know the universal investment benchmark is the 60/40 portfolio of stocks and bonds. If you replaced bonds entirely with gold, there is nearly no difference in performance on a risk-adjusted basis whether the timeframe is from 1973-2024 or 1928-2024.

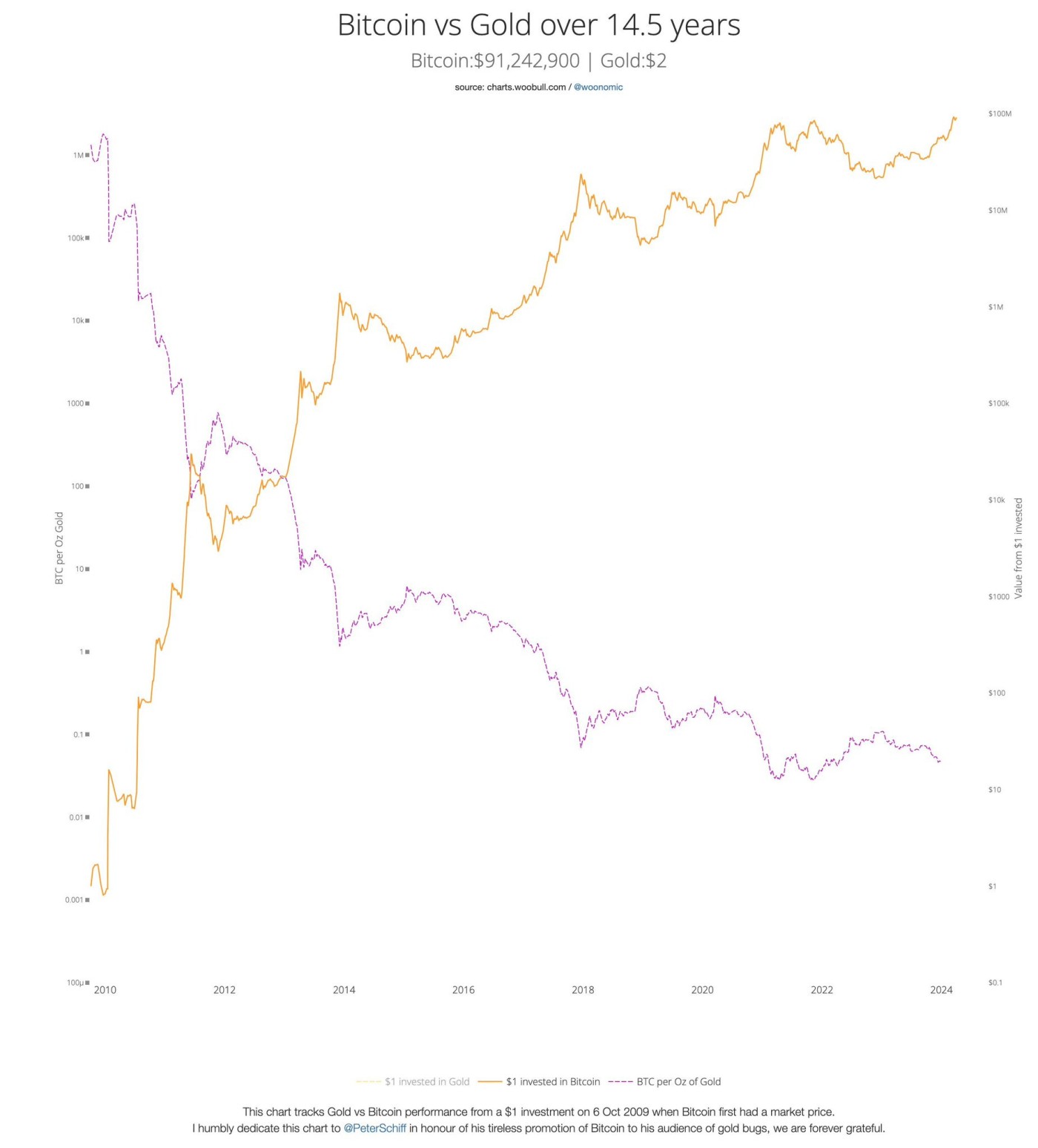

Uniquely, $1 invested in Bitcoin in 2009 is now worth more than $91 million. $1 invested in gold in 2009 is now worth about $2.

Some have suggested Bitcoin is perhaps not yet the fear trade nearly as much as gold. Bitcoin remains highly sensitive to liquidity which has been less than plentiful despite stealth QE. That said, in 2008 and 2020 during the Great Financial Crisis and COVID, all vehicles including gold plunged due to lack of liquidity due to investors panicking to escape into cash. Gold lost more than -30% in 2008 in several days but then was the first to hit new highs the weeks after. In both cases, the Fed issued enormous money prints via QE. In 2020 when Bitcoin was trading, it soared as a consequence. Markets love liquidity.

Currently, the attack over the weekend sent Bitcoin lower as it was the only vehicle trading. Both stocks and Bitcoin remain in correction.

Bitcoin’s sell-off over the weekend also coincided with the last 3 days before American citizens had to make tax payments on Monday. Historically, we have seen bitcoin drop in the 2-3 days before April 15 as holders sell the asset to raise cash to pay their taxes. Thus, multiple factors drove down bitcoin’s price over the weekend.

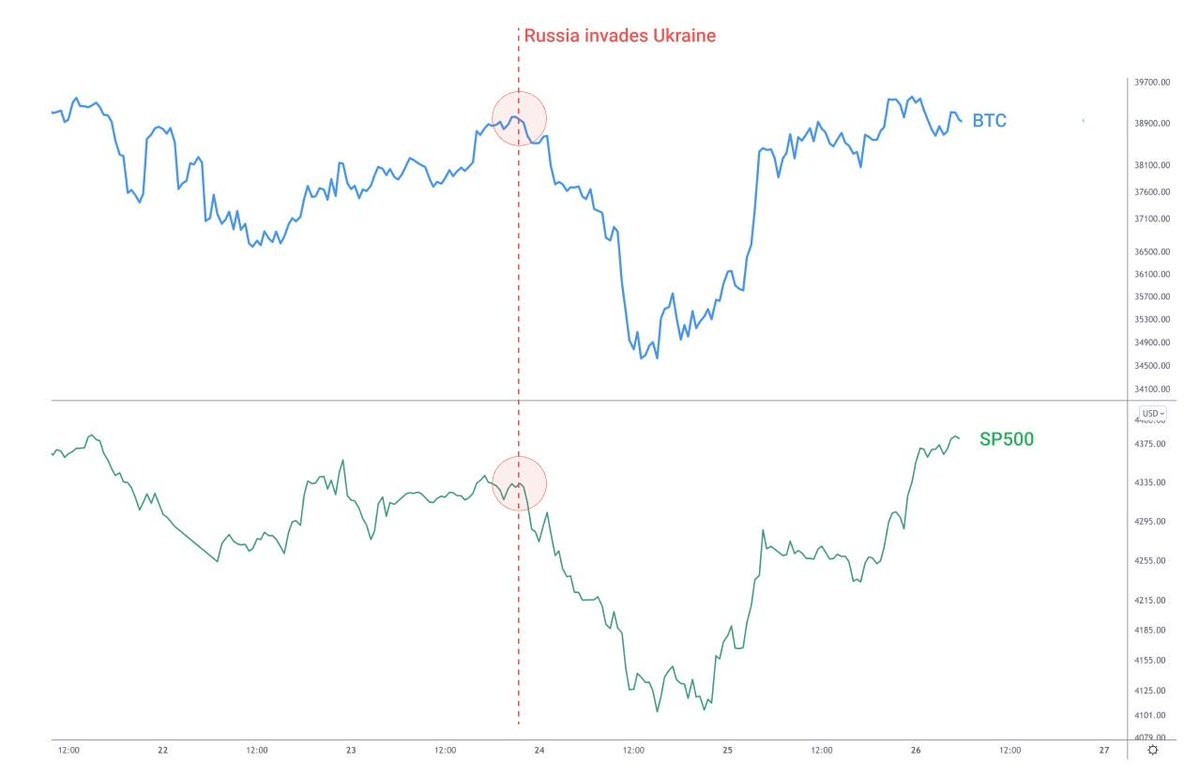

In past wars, stocks rallied. In 1990, the war against Iraq sent stocks soaring. When the war in Ukraine began, Bitcoin dropped just over -10% over the next day but then quickly recovered a day later. This time, uncertainty remains as to when Israel will retaliate against Iran's recent drone attack. Markets dont like uncertainty.

The Fed's data vs. the real data

Data the Fed uses to gauge economic strength continue to show a strong economy with no signs of slowing down. Yet certain metrics are showing otherwise.

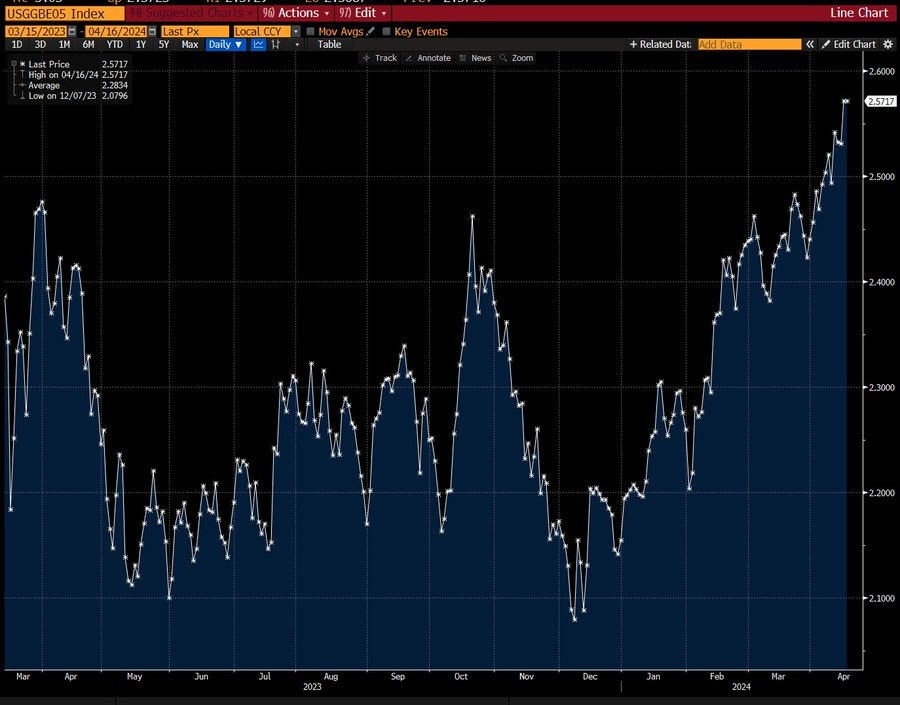

The market's implied rate of inflation over the next five years has risen to 2.6%, the highest level in more than a year. Inflation is bearish for markets though inflation in the 1970s proved bullish for precious metals. The same could happen later this decade.

CPI inflation may hit 3.9% - 4.8% by the 2024 election, according to Bank of America. Over the last 3 months, CPI inflation has averaged 0.4% on a month-over-month basis. If this trend continues it puts year-over-year inflation on pace to hit 4.8% by November, its highest since April 2023, more than twice the Fed’s 2% inflation target. This would likely probably the Fed to pivot to rate hikes. With less liquidity, stocks and cryptocurrencies would likely fall.

|

Employment is also a concern. Since 1990, there have been four recessions. In all four cases, percent change year-over-year of those employed fell below zero. We just crossed below zero. If historical trends hold, this should lead to a recession. That said, any recession may be quickly ended because the Fed can use QE as they did in 2008 and 2020 to stop short the recession. 2009 onward and 2020-21 both saw soaring stock markets. If the Fed did so again, stocks and Bitcoin would likely outperform. The question is whether we would get a black swan of such magnitude to justify such a massive money print. If not, the Fed's hands could be tied in which case we could sink into recession. If such were to hit before the elections, Biden would unlikely get reelected.

|

Bitcoin halving

As we approach the April 19 Bitcoin halving [this piece was sent out before and after the halving], investors have been understandably reluctant about Bitcoin miners. In the month following halvings, miner revenue has dropped by an average of 46%, but in the year following past halvings, miners grew their revenues by more than 100% on average, thanks to rising Bitcoin prices and more efficient hardware. Bitcoin miners therefore tend to have a fairly high correlation to the price of Bitcoin. The leading miners over the long run are MARA and CLSK. Even though both look like disasters at the moment, stay aware potential future entry points. Watch for volume dry-ups, pocket pivots, and undercut & rallies of major moving averages or prior major lows in the chart patterns. But for now all of these vehicles remain in correction.