by Dr. Chris Kacher

The flywheel of CPI/PPI Inflation + QE pump

After hot CPI and PPI numbers, CME FedWatch now predicts the first rate cut in June with a terminal rate of 450-475 bps in December for a total of just three rate cuts. Rates are likely to stay higher for longer. This is the mark of a strong economy at least for now. But keep in mind $21 bil / month is still being injected into the economy via stealth QE. In other words, total QE exceeds QT by more than $21 bil / month.

If global QE can resume its uptrend, markets should ultimately find their way higher though with some expected zig-zag action along the way.

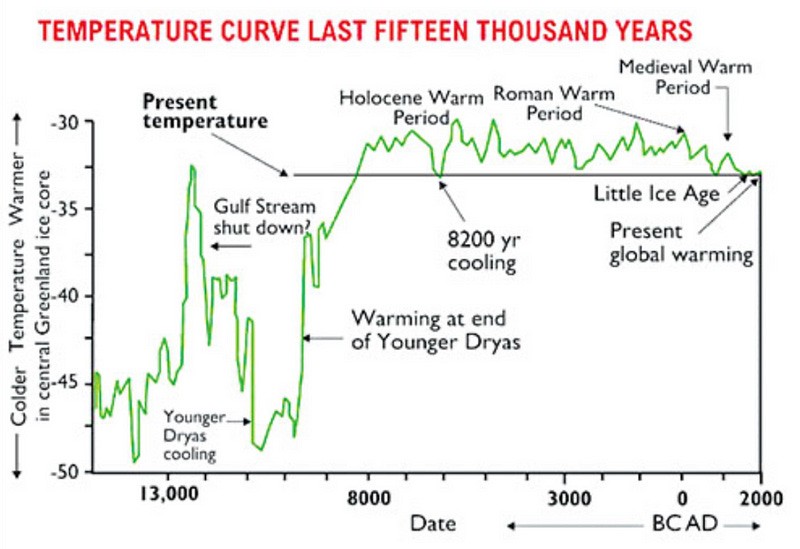

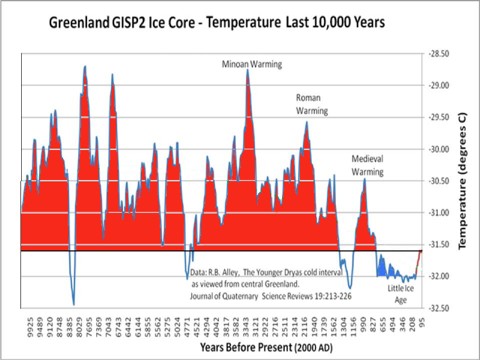

Stealth QE will continue not just for funding expanding wars, unfunded liabilities such as pensions who have losses from real estate bond exposure, and healthcare, but the uneconomic regulations that deal with the consequences climate change. When laws are enacted that hamper corporate profitability, GDP is diminished. This will push governments to create more fiat to aid their sagging economies. There is no free lunch. There was even talk of making farming carbon net zero. This would result in waves of starvation if such laws were enacted. But even such laws including the ones that are already in place would do little to impact rising temperatures.

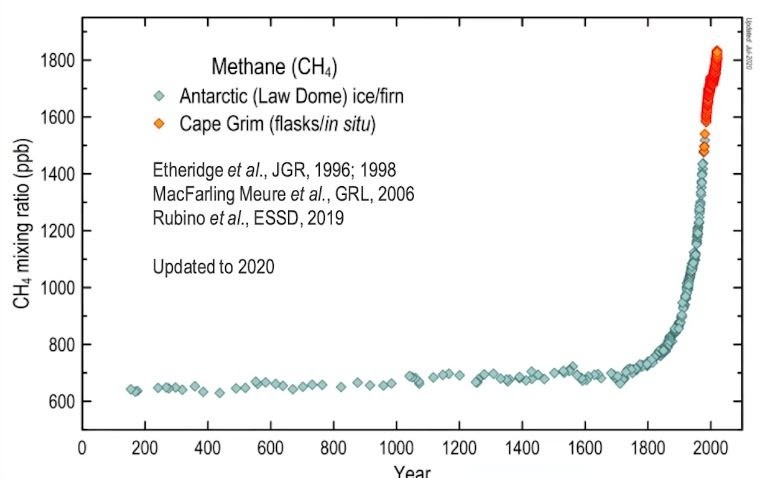

Methane is also a major issue while all focus is placed on carbon dioxide emissions, a big mistake.

Bitcoin halving

Speaking of which, together with capital inflows into spot Bitcoin ETFs, the upcoming Bitcoin halving on April 19 will reduce the number of BTC mined per day from 900 to 450 BTC. If the current rate of inflows to spot ETFs continues at a steady pace, let alone increase, the amount of BTC bought daily could exceed the newly mined supply by 10x. This could make for one supercharged supply shock which could move Bitcoin to new all-time highs later this year. But note that inflows into Bitcoin ETFs may diminish over time.

Is this 1999 again?

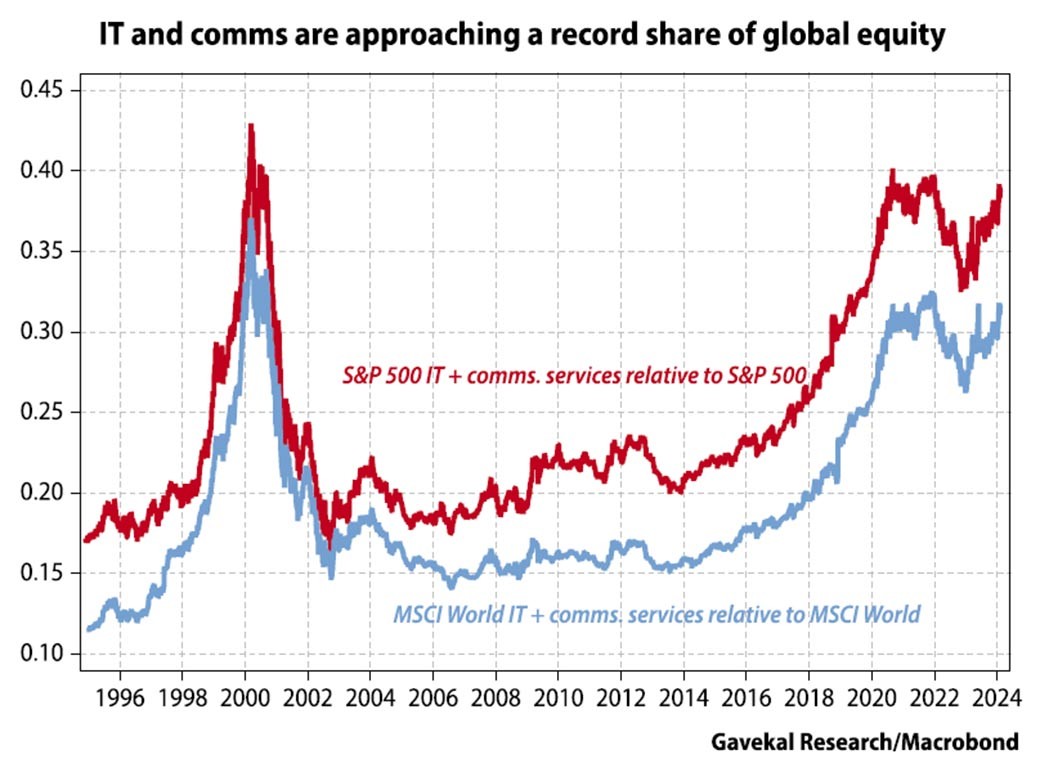

Many are trying to compare today to 1999 in terms of the AI stock market bubble vs dot-coms. It is true that by early 2000, technology accounted for more than 40% of the S&P 500 during the dot-com boom. We are approaching similar levels today.

And, just as in 1999, almost all of the market’s performance in 2023 came from a handful of stocks, which all happened to be in the same sectors.

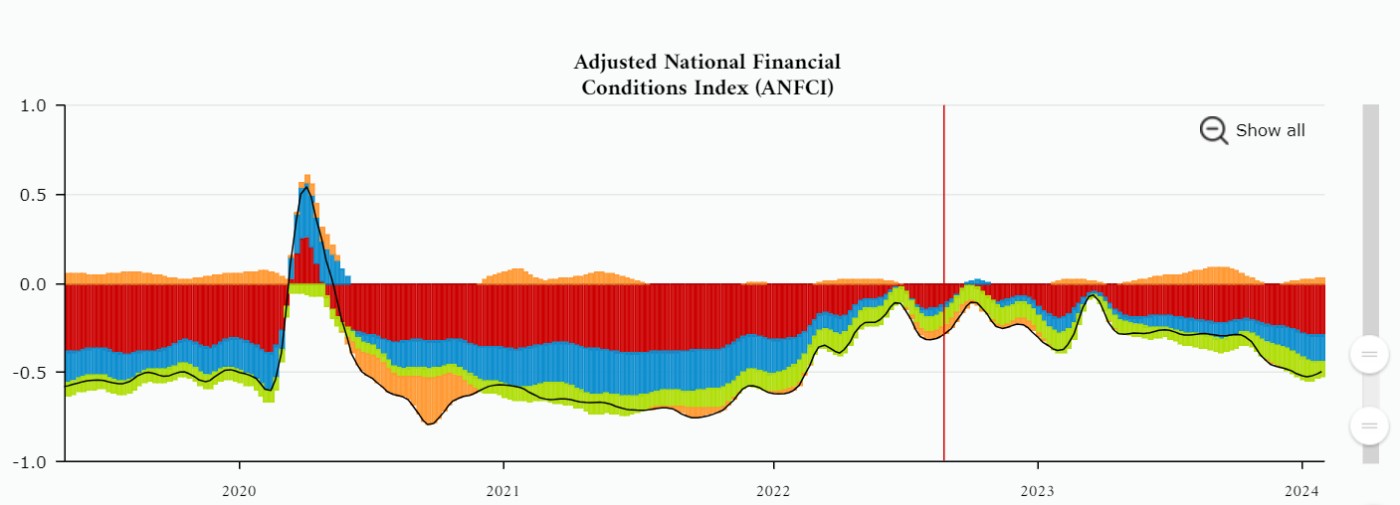

But in 1999, the government was balancing the budget on a cash basis. It was not using quantitative easing. Today, it is running multi-trillion dollar deficits. Between debt rollover and budget deficits, it may need to issue several trillions of new bonds in 2024. This is fiscal QE that acts as a countervailing force to the Fed's tightening. Financial conditions have been a lot more loose since mid-2023.The Adjusted National Financial Conditions Index (ANFCI) shows contributions from the three categories of financial indicators being risk, credit, and leverage. The contributions sum to the overall index. It shows the massive COVID QE pump from March 2020, tightening in 2022, then loosening since March 2023 when the Fed had to do an emergency print to save failing banks.

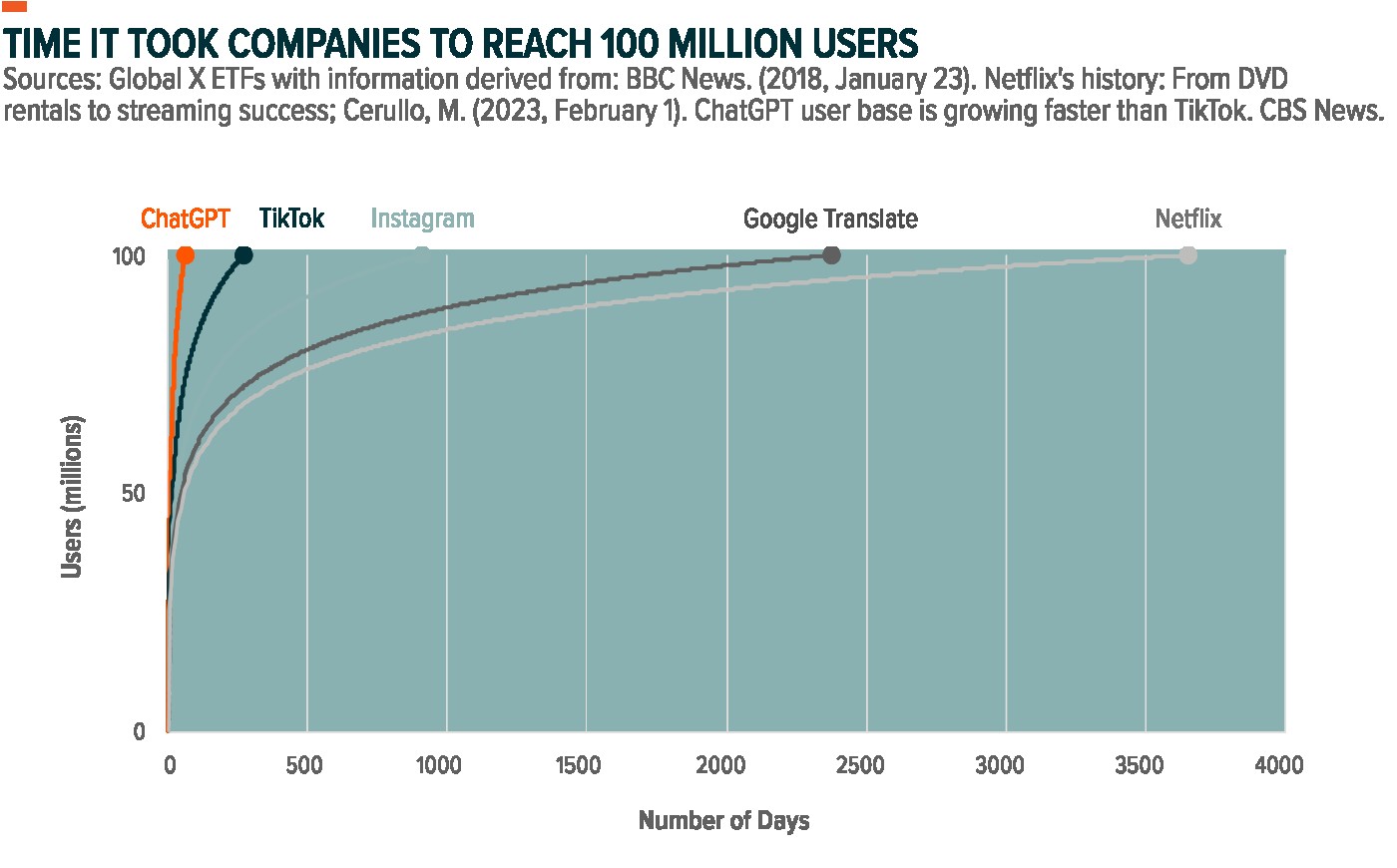

Further, 1999's dot-coms were mostly dot-bombs with non-functional business models. Only a small handful of companies emerged from the wreckage such as Amazon, Yahoo, and Ebay. By contrast, today's AI technology is enabling hundreds of millions of people along with companies of all sizes to greatly boost their productivity. AI's long trek that began many decades ago is finally at a point where the masses can benefit via generative AI platforms such as ChatGPT whose pace of development since it was released in Dec-2022 has been at lightning speeds. No technology compares to such stunning rates of growth.

NVDA/AI

NVDA blew past expectations when it reported earnings after Wednesday's close. Data is the new gold. While AI compute demands seem endless now, the CEO of NVDA Jensen Huang clearly anticipates a shift to efficiency over compute. He anticipates faster chips will increase efficiency, reducing overall AI spending needs significantly lower than Sam Altman’s $7T chip initiative.

But keep in mind that widening US chip curbs against China, its third largest market, would sap growth and hamper the AI-driven boom in its business. On Nov 21 when it reported earnings, it fell in the ensuing days due to this concern, but then resumed its uptrend.

While NVDA beat estimates across the board, sales to China slowed significantly on fears they could use the chips for military applications. Nevertheless, for the quarter, Nvidia reported $5.16 EPS on revenue of $22.1 billion vs. estimates of EPS of $4.60 on revenue of $20.4 billion. That's a massive jump from the same period last quarter when Nvidia reported EPS of $0.88 on $6.1 billion a year ago. The company also guided higher than analysts' expectations for the first quarter, saying it anticipates revenue of $24 billion vs. analyst estimates of $21.9 billion despite the sales slowdown to China.

“Accelerated computing and generative AI have hit the tipping point. Demand is surging worldwide across companies, industries and nations,” Huang said in a statement. “Our Data Center platform is powered by increasingly diverse drivers — demand for data processing, training, and inference from large cloud-service providers and GPU-specialized ones, as well as from enterprise software and consumer internet companies. Vertical industries — led by auto, financial services and healthcare — are now at a multibillion-dollar level."