by Dr. Chris Kacher

The great global liquidity cycle

Since the great financial collapse of 2008, financial crises have been met with quantitative easing (QE), which are fundamentally debt-refinancing crises. A 5-6 year cycle in global liquidity is due to debt maturity rollovers, where refinancing pressures are pronounced. Such pressures dictate market direction, not traditional metrics like debt/GDP. Monetary inflation defined by liquidity growth which devalue fiat matters most as assets such as stocks, gold, and bitcoin tend to rise over time due to this inflation. While bitcoin remains volatile, much of the volatility continues to bleed out of the asset as it matures. Over the cycles since it was created in Jan-2009, it is the best representation of how global liquidity spurs inflation which erodes buying power.

Public debt is expanding faster than private debt, fueled by unfunded liabilities such as pensions and IRAs as well as rising interest burdens due to record levels of debt across central banks. This ensures persistent liquidity growth. Since debt both backs and demands liquidity, and liquidity drives asset prices, gold which is up over 12x since the year 2000 and bitcoin which is up far greater serve as pure monetary inflation hedges.

Regardless of who sits in high office, fiat devaluation is inevitable. It is a question of how fast this devaluation takes place. Nixon taking the dollar off the gold standard gained the Federal Reserve and other central banks much greater control in managing the money supply, setting interest rates, and responding to economic crises. QE would not have been possible under the gold standard, because the Fed could not have created money beyond the gold it held. QE has been used to address all financial crises after the Great Financial Collapse of 2008.

Financial markets today are are primarily rolling over existing debts, less funding new productive investments. Thus liquidity, not interest rates, becomes the key driver. Refinancing walls such as the upcoming mid-2025 debt maturity create cyclical liquidity pressures. This explains why the global liquidity cycle lasts about 65 months.

With global debt at record levels, interest on the debt adds a material sum of money that needs to be digitally created, thus global liquidity may accelerate from here. Hopefully, Dalio's fears will not be realized, so the world will not get Zimbabwe'd.

(Note how one can draw a straight line on this log plot showing how prices exponentially rise over time as the dollar gets devalued.)

(Note how one can draw a straight line on this log plot showing how prices exponentially rise over time as the dollar gets devalued.)Tariffs pros and cons: Dalio's day of reckoning vs. Chamath Palihapitiya

Ray Dalio of Bridgewater just published a piece on his concerns that the tariffs will be the straw that breaks the camel's back. While his fund has been a top performer, his predictions have sometimes fallen short, especially over the last decade. His concerns of collapse have yet to materialize.

Dalio did a deep dive into past long term debt cycles going back many centuries. The average long term debt cycle lasts 75 years give or take 25. While the work is useful in attempting to avoid a recurrence of how sovereign currencies eventually fail, it has often focused too much on the past without regard to existing exponential technologies that make this time materially different. That said, Dalio now acknowledges that such technologies can be game changers, and has provided suggestions on how to sidestep the collapse of the dollar by lowering rates, raising taxes tamely, and increasing government efficiencies. Two of these three are being met.

In lieu of tax hikes, Trump's tariffs aim to level the playing field, making trade agreements fair. One benefit is lower taxes on US citizens. Dalio's concern is that such tariffs will disrupt global trade and supply chains, pushing the US into turmoil, wreaking eventual havoc on the dollar's sovereignty. But this ignores the possibility the US will retain its pole position in technology, especially in AI. US leadership in AI and advanced technology is a major asset that can help preserve economic strength and support the dollar’s global role. However, it is not a silver bullet. The dollar’s sovereignty also relies on prudent fiscal policy, global trust, and an open, stable financial system.

China and others are closing the gap, producing more science and engineering graduates and patents, and building their own tech ecosystems. Rising global tensions, new trading blocs, and the development of alternative payment systems such as central bank digital currencies and China-led initiatives are already reducing the dollar’s share in global reserves and trade.

As the world becomes more multipolar and alternative payment systems grow, US technological dominance must be matched by sound economic and diplomatic stewardship to maintain the dollar’s unique position. The burning question is whether Trump's leadership can achieve this.

In favor of the tariffs, the notable Chamath Palihapitiya wrote that he believes for democracy to last, regular people, not just government workers or powerful groups, should have more control over the government and the economy. He thinks the system should work for everyone, not just a few at the top. He said the fastest way to make other countries change is to affect how much money they make from selling things to the US. By putting tariffs (extra taxes) on imports, the US can quickly pressure other countries. He admits that these changes might make things unstable for a while, but he thinks it could lead to a big change in how the world works. In the end, he hopes this will create a stronger democracy in America and an economy that helps most people, not just a few.

My view is that while it can strengthen the economy in the US, it may come at a much higher price in the long run. Ray Dalio believes the tariffs impact the intricate web of global interrelationships which will disrupt economies, markets, geopolitical orders, climate change, and tech innovation. This could threaten the dollar's sovereignty especially this late in the long term debt cycle, if history is any guide.

That said, this time is different due to exponential technologies which potentially prevent the past from repeating. A growing number on the cutting edge believe higher forms of AI such as artificial general intelligence (AGI) will come much sooner than originally predicted due to the rate at which AI is evolving. Already, AI bots and AI agents can train future bots and agents which increases the pace of evolution. Think of AI as an advanced form of human intelligence that can be used to help humanity better navigate challenges. As AI evolves, this will become more clear. And as with all technologies, AI is a double-edged sword, but history has *always* shown that all technologies always result in more jobs. This in turn enables a greater focus on rapid innovation which solves big problems which boosts economic growth.

In time, bolstering centralized forms of governance over others as Trump is attempting to do for the US will become outdated in the coming years as decentralized forms of governance spurred by the exponential growth of the network state takes hold as detailed in prior reports and in Balaji Srinivasan's book, "The Network State".

Should the market correction worsen due to recession, central banks would have no choice but to print big. Renewed direct QE would increase the rate of inflation at a time the world can ill afford it, but would likely create an uptrend in stocks and bitcoin. Further, Trump's softening stance toward China and other countries along with sentiment levels falling from their bearish extremes as well as accelerating global liquidity can create renewed uptrends.

But even without direct QE intervention, stealth QE remains in effect and lower rates are likely. Investors such as Raoul Pal believe liquidity is key so dismisses tariff-driven recession risks. Focusing on central bank actions, dollar trends, and cyclical indicators shows the global economy is poised for growth despite short-term turbulence. Of course, such turbulence has and can continue to tug markets lower in a hurry so always keep stops tight. Furthermore, given that the tariffs will create turbulence at least in the short term, such could spur recession. Indeed, there are more than a few unknown variables thus the sharp differences of opinion between Ralio, Palihapitiya, and Pal.

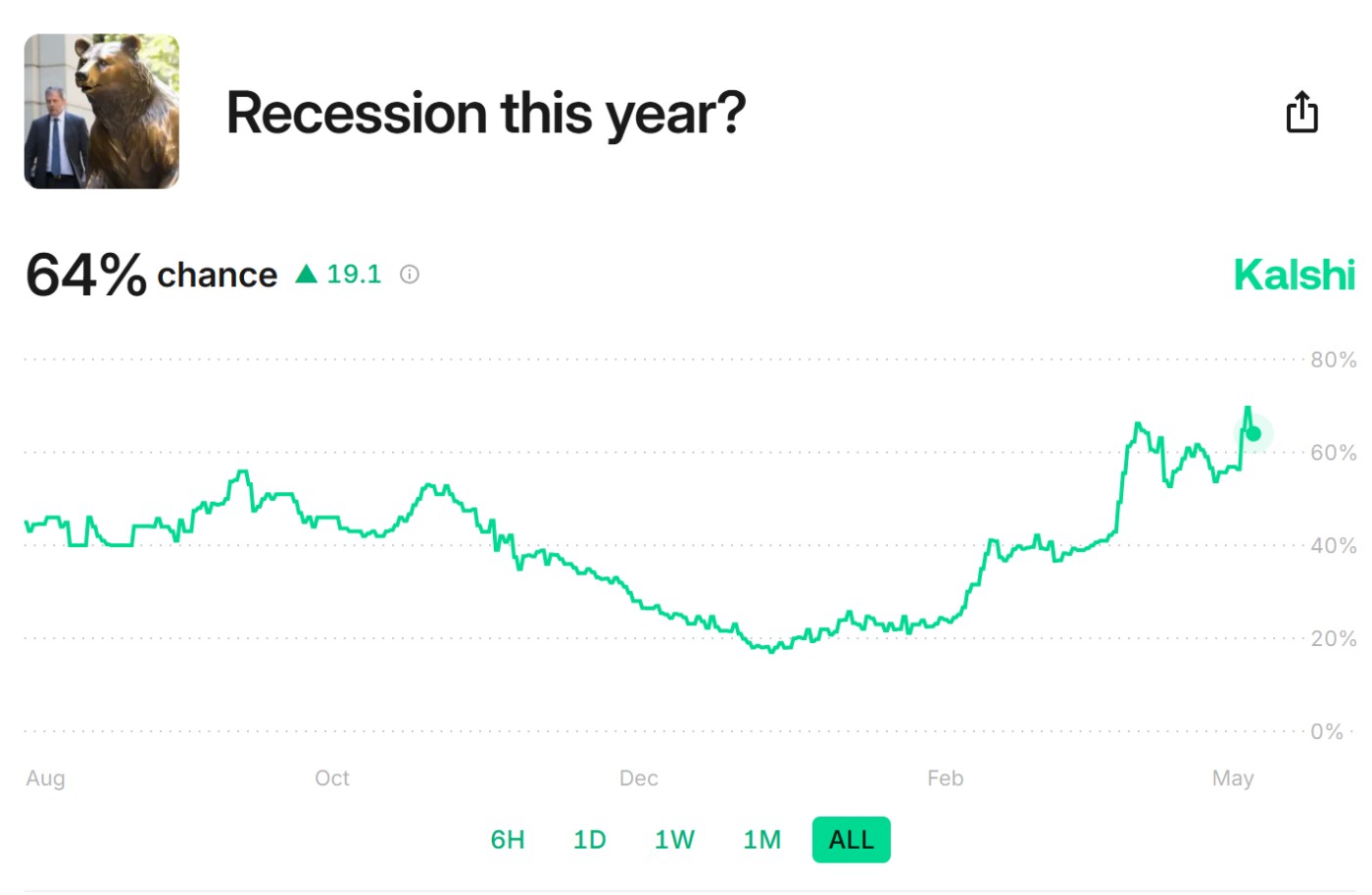

Prediction markets are in alignment with investment banks which all now predict a negative GDP for the first quarter. Indeed, US GDP contracted -0.3% in Q1 2025 despite estimates of 0.3% growth. Worse, the GDP Price Index surged to 3.7%, its highest since August 2023. The Fed must pick between containing either inflation or unemployment. If they dont lower rates, US GDP will weaken and likely increase unemployment. If they cut rates, expect inflation to rebound. The Kalshi prediction market sees 64% odds of a US recession in 2025. CME FedWatch now expects 4 rates cuts for this year. One silver lining was the core PCE which came in at 0.0%, below estimates of 0.1% though PCE (year-over-year) came in at 2.3%, above 2.2% estimates. META and MSFT also reported strong earnings well above estimates. The market remains in flux in terms of whether liquidity will be sufficient to combat economic weakness.