Market Lab Report

by Dr. Chris Kacher

The Web3 Evolution Will Not Be Centralized™

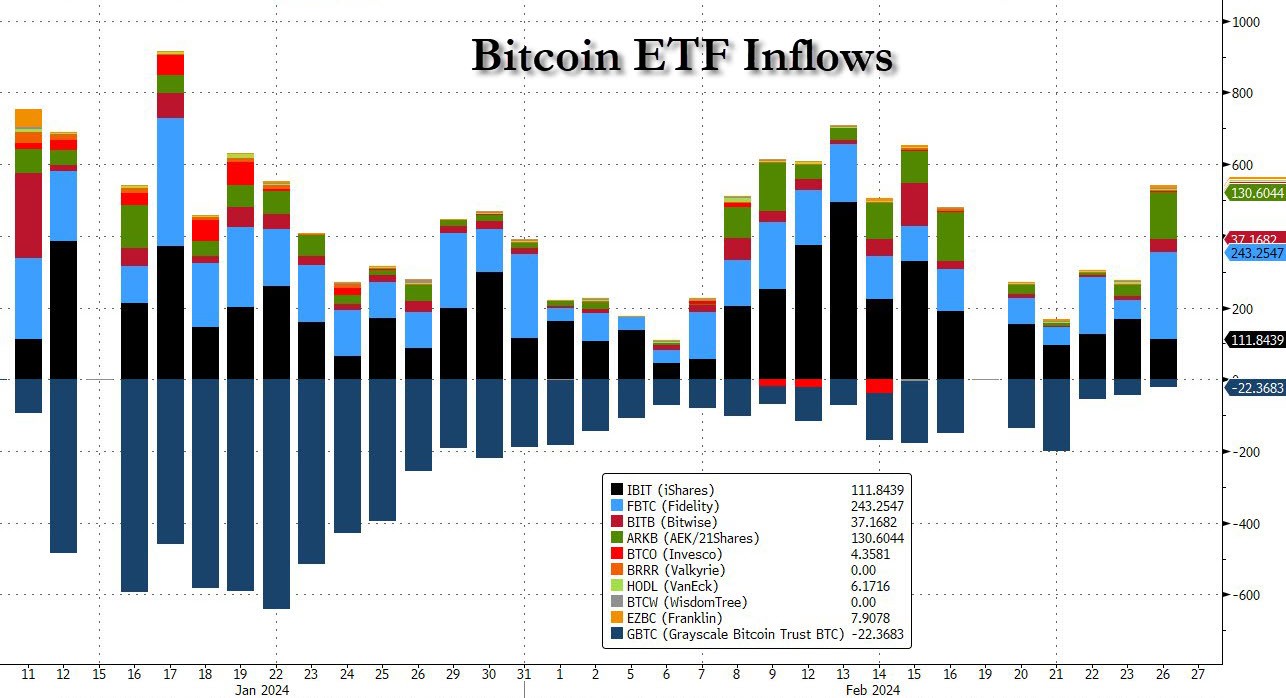

People ask how I've been able to time major entry points in Bitcoin. I use Bitcoin metrics, financial macros, and fundamentals of leading cryptos along with technicals to time my entries. I have written that global liquidity correlates to a high degree with Bitcoin. Today, we also have Bitcoin spot ETF inflows which help drive its price higher while global liquidity is bouncing after waning for several weeks.

As for Bitcoin price, after its spot ETFs were approved, Bitcoin headed lower until Jan 23 when it found its floor. We first suggested members buy BTC on Feb 1 as net inflows continued to increase then anticipated the breakout on Feb 7 correlating with decreasing GBTC Bitcoin spot ETF inflows. Most recently, Bitcoin ETF inflows jumped higher driven by surge in Fidelity's FBTC as GBTC outflows trend towards zero.

Hyper exponential AI + NVDA

As concerns hyper exponential growth of AI, a recent Goldman Sachs report pointed out that, “Innovations in electricity and personal computers unleashed investment booms of as much as 2% of U.S. GDP as the technologies were adopted into the broader economy. Now, investment in artificial intelligence is ramping up quickly and could eventually have an even bigger impact on GDP.”

As we have mentioned in prior reports, such e/acc (effective accelerationism) technologies could postpone recession as greater than expected utility is created. Just three of many examples:1) Insilico Medicine is revolutionizing the traditionally slow and costly process of drug discovery by using AI to rapidly identify and test novel drug targets. AI has helped them accomplish with 50 people what a typical drug company does with 5,000, or a 100x gain.

2) Figure Company is supercharging the future of labor and technology by creating walking humanoid robots. They plan to manufacture and deploy 1 million Figure units by 2030. They currently are in talks to raise as much as $500 million in a round led by Microsoft and OpenAI.

3) Daily.ai allows the user to publish AI-powered email newsletters that generate 40-60% daily open rates without the user having to write a single piece of content, a dream for marketers and customer engagement.

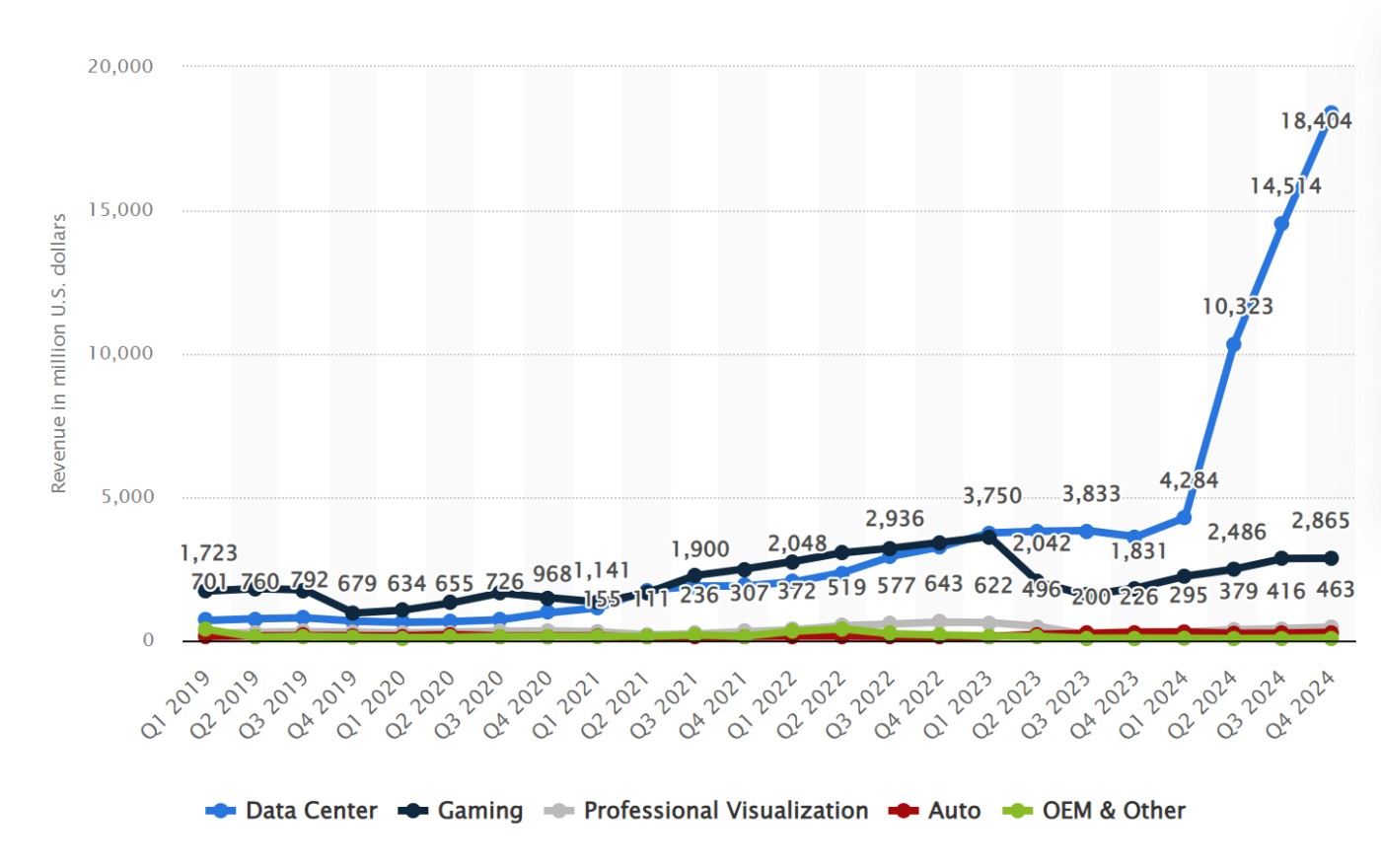

Of course, NVDA is one of the prime beneficiaries from AI chip demand. Data center growth which powers generative AI has been astounding since ChatGPT went live and NVDA's revenues show no signs of slowing.

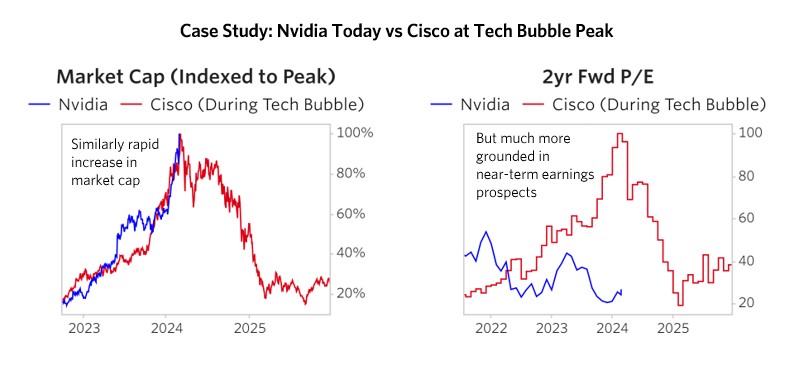

That said, some have asked if NVDA today is the CSCO of the dot-com boom? A chart overlaying the stock price of CSCO from 1995-2001 with NVDA from 2022 to present day shows their charts look similar. But the 2yr forward P/E for NVDA is much more down to earth compared to CSCO back in the late 1990s.

Further, NVDA multiples today are nowhere near the multiples of CSCO back then. NVDA's value is grounded in real margins and real profits. NVDA also has a deeply competitive moat. While CSCO's networking equipment and servers were much easier to commoditize, NVDA's products such as the Hopper 100 contains over 35,000 components and weighs 70 pounds are much harder to recreate. Indeed, China has tried thus the NVDA chip trade embargoes against China have been effective.

Jeff Bezos of AMZN has famously said, "Your margin is my opportunity." Big cloud service providers such as GOOGL's cloud data center will compete away some of NVDA's margin. GOOGL has $100 bil to spend. But there’s always going to be a need to stay up-to-date with the latest chips. NVDA's monopoly on chips can keep it in pole position a lot longer than expected. Natural monopolies can exist for longer than expected.

But a key question is if NVDA is to become a $5-10 trillion company, or a 150-400% gain from its current price, it needs to support an economy that is many times larger. As a rough rule, a company's market cap correlates with the underlying economy it supports. So will the AI economy continue to grow at its current pace? When it comes to tech, the adage, "If you build it they will come" holds true. Back in the late 1990s, internet video streams or even profile pics were severely limited by bandwidth thus often written off as dead. But once the infrastructure layer improved, the application layer developed quickly. So given NVDA's revenue projection out to a few quarters, they expect to continue to grow at breakneck speeds by providing the chips necessary which are in great demand to build out the infrastructure layer, so the application layer where value accrues will quickly evolve. The AI economy should therefore continue to grow quickly at far greater speeds than cutting edge technologies did in the earlier days of the internet.