by Dr. Chris Kacher

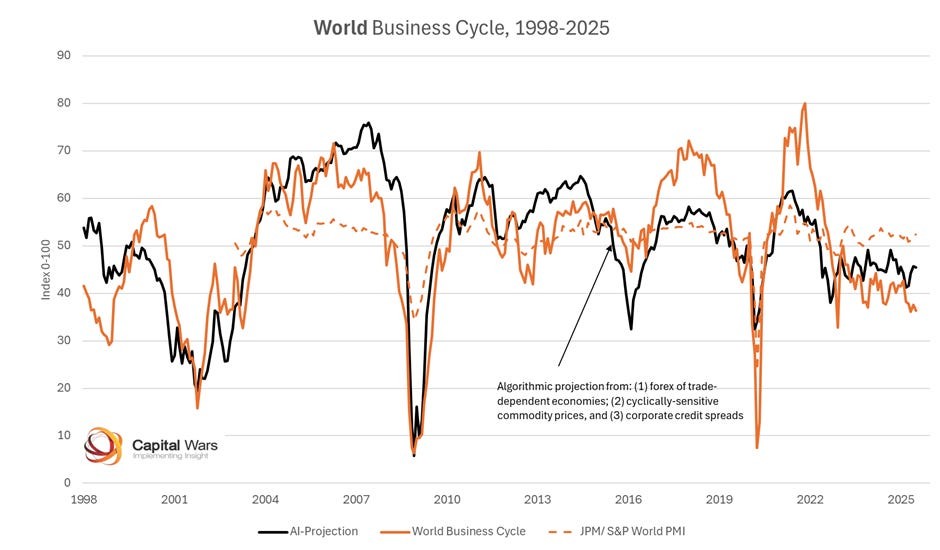

Trendless global economic activity

The chart shows three measures of global economic activity: AI values based on global commodity prices/credits/trade-sensitive exchange rates, the global business cycle, and the JPMorgan/ S&P PMI Index. The AI values are more accurate because it records actual results compared to the last two which are opinion-based. Yet all three paint a similar picture of a sluggish, not recessionary global economy, while the AI values and the global business cycle tend to correlate.

Interestingly, there is no obvious business cycle to speak of since COVID emergency stimulus ended. Of course, other forms of stimulus that outweigh COVID stimulus have been in place but this has been insufficient to spur the global economy which remains trendless. This has triggered analysts to warn of impending busts.

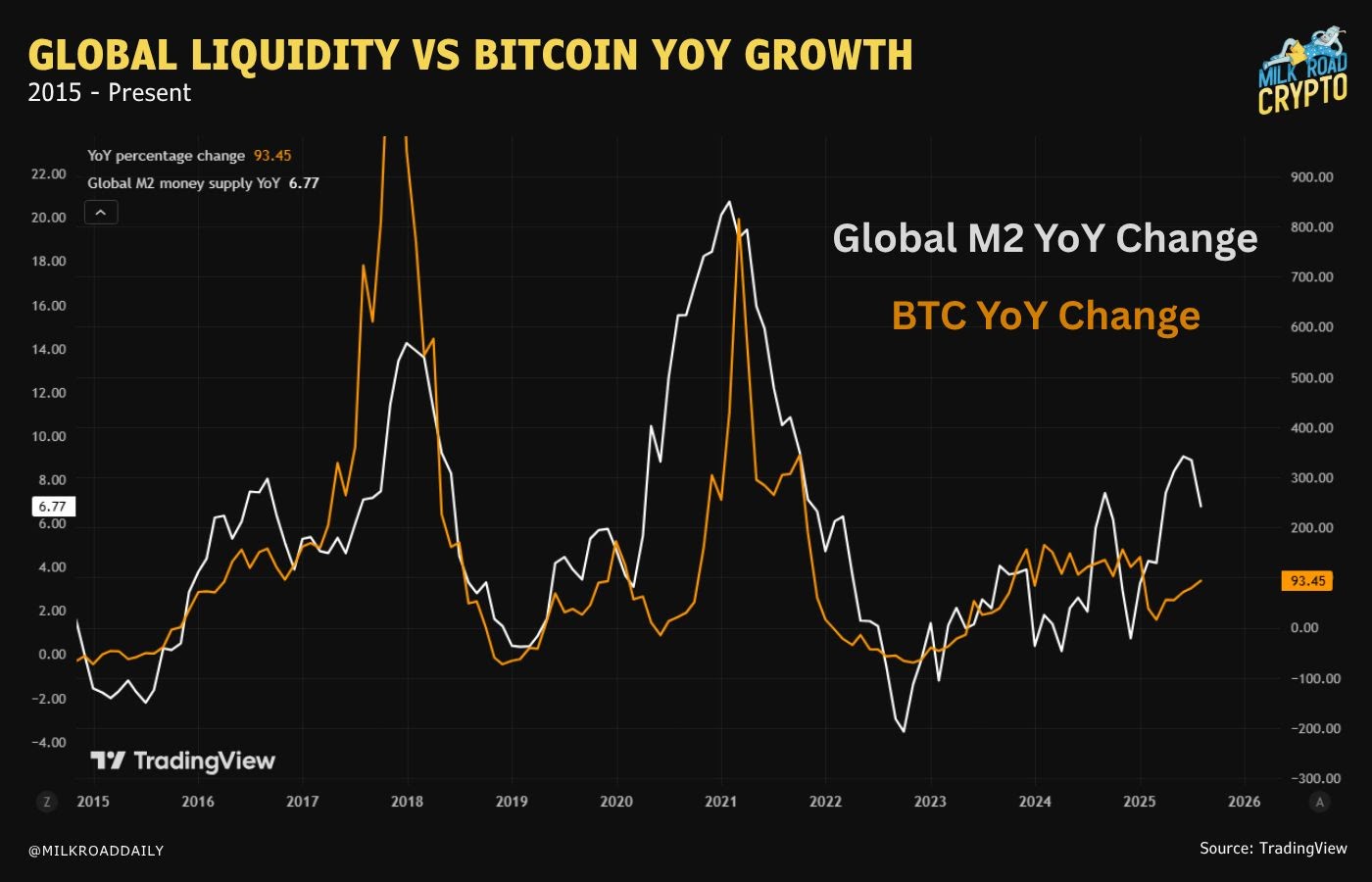

Further easing of interest rates should help continue the bullish price action in stocks, Bitcoin/Ethereum/crypto, real estate, and precious metals. Notice how global M2 continues to move higher since early 2023 albeit in 3 steps forward, 2 steps backward fashion. This has resulted in Bitcoin trending higher then basing, over and over, since then.

Meanwhile, Raoul Pal's favorite indicator, the ISM, has been relatively trendless since early 2023. ISM predicts the pace of global liquidity. So if we compare prior bullish periods such as 2017 and 2020-21 where ISM and global liquidity were soaring to the current period (2023-present), we see ISM and global liquidity are just getting started. Global M2 has hit new highs but we may not see it, along with ISM, start to surge until the Fed starts to lower rates once again as well as Trump's $5 trillion package spurring the digital printing press. FedWatch futures predict three more rate cuts this year with around a 90% chance of a rate cut in September.

Some manufacturers say the lower ISM reading is due to customers holding off or cutting back on buying, likely because of uncertainty around tariffs, but now that the tariffs have been sorted out, it could help pick business back up again. This is bullish for the ISM along with rates and the dollar, both which should ease into the rest of the year.

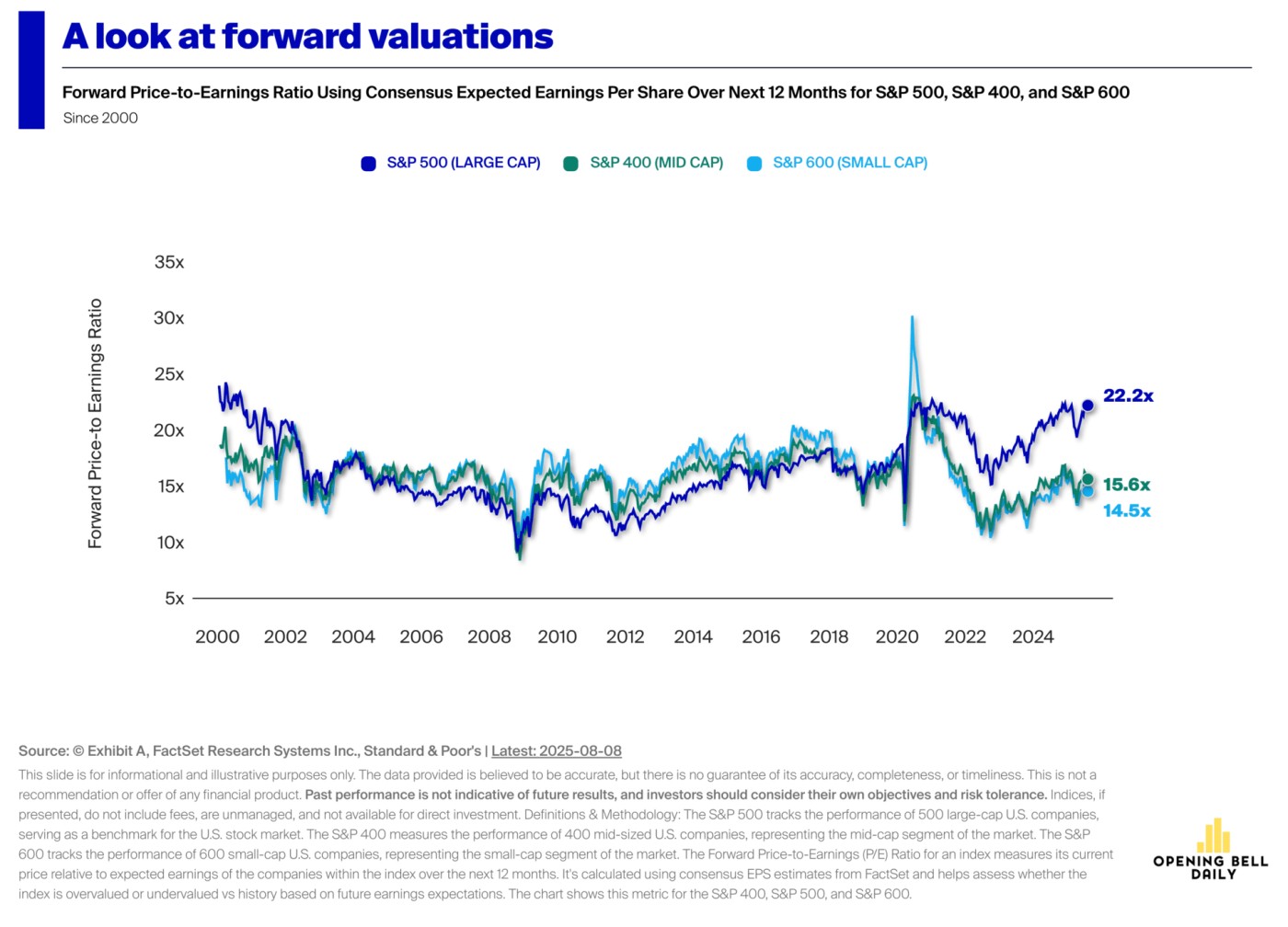

Priced to perfection?

Some analysts are concerned that markets are priced to perfection. AI enthusiasm which is partly driven by hype has pushed valuations to unprecedented levels. More than 20% of stocks in the MSCI World index now trade above 10 times sales, making it larger than during the peak of the dot-com bubble. A Man Group strategist wrote, "It’s one thing to justify these valuations when US 10-year Treasury yields are below 2%. But with yields now around 4.5%, the justification becomes much harder to swallow.”

When enterprise value-to-sales ratios top 20x, the median Russell 1000 stock has lost roughly 73% over the next five years while the median MSCI World stock has lost roughly half of its value.

Forward P/E ratios over the next 12 months are near record levels and the S&P 500 is now trading at 3.15x sales, its highest valuation in history.

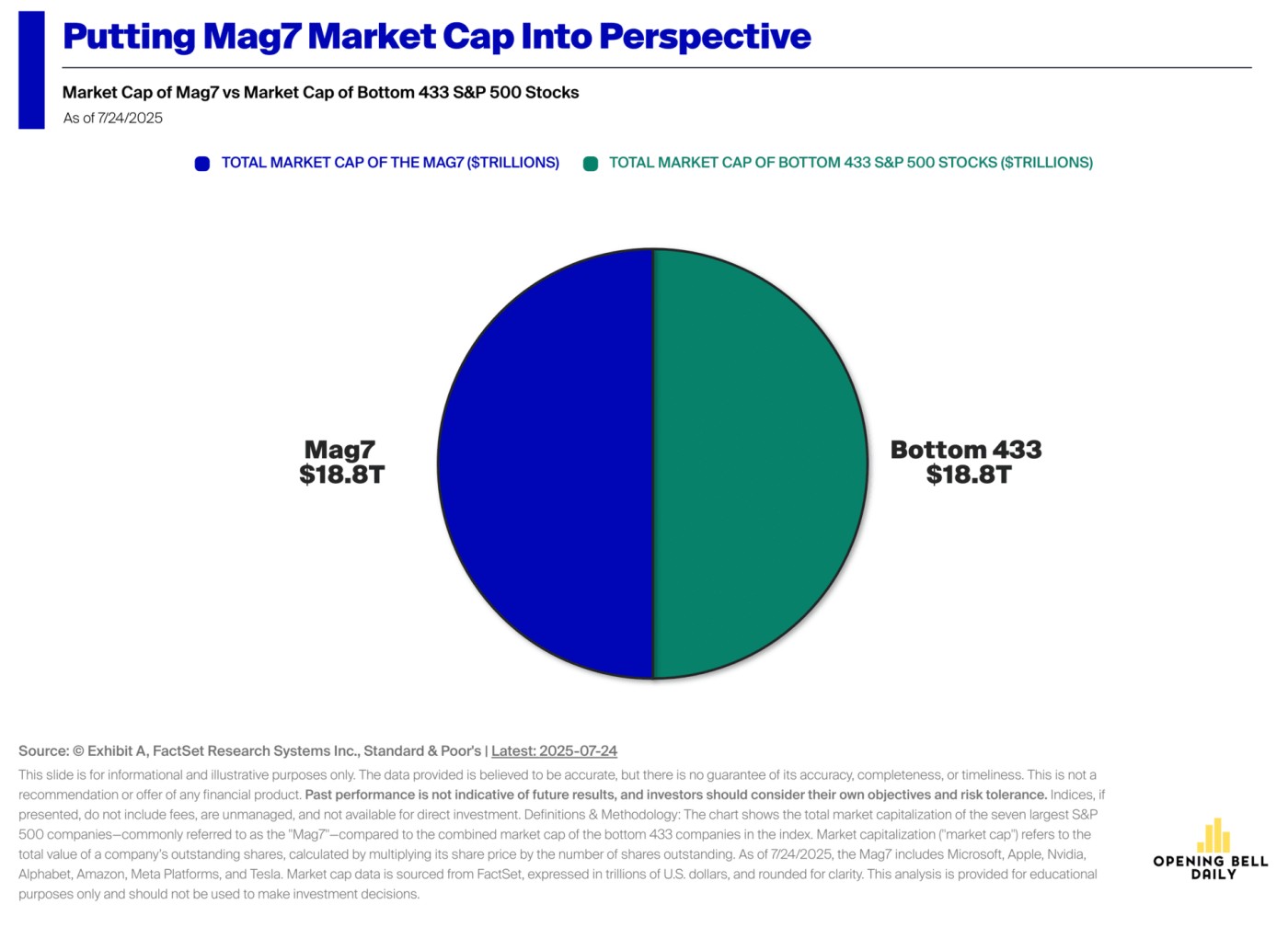

I would argue that rates are coming down, and The Magnificent Seven have deep moats while reporting record profits due to AI, a technology that is adding material value now which some argue justify lofty valuations. Anthropic's recent valuation surge from $65 billion to $100 billion in months, with Claude Code generating $200+ million annually at 60% margins, proves AI is already creating massive economic value. These companies are solving real problems and generating real revenue at unprecedented scales. These names are not pets.com. Plus the market has become bifurcated where only the strongest survive and thrive, so while the majority can lag or fall in value, the best win the day.

Further, the US dollar has been debased at the much faster pace of 4% than the 2% the public has been led to expect over the last 50 years. Kobeissi letter writes, "“Fiat currencies are in an eternal bear market. The US, Canada, China, and France have averaged around 4% inflation over this period." This debasement accelerated after 2020 due to COVID then massive spending packages such as the recent $5 trillion one put forth by the Trump administration. In consequence, the dollar has been debased by 30% since 2020, so stocks are trading at a higher premium to account for this.

Bitcoin which reflects the devaluation of fiat even more so than stocks shows through its metrics that we are not anywhere near a market top. While one can expect sharp news driven corrections along the way such as the one brought on by the hot PPI numbers, or overvaluation concerns such as the deep correction on September 3, 2020 in both stocks and cryptocurrencies, Bitcoin has yet to climax top if history is any guide. Ethereum and other alt coins seem to just be getting started as ETH nears old highs of $4868 achieved during its last climax top in November 2021, the month we warned investors that the Fed has changed its tuned and would start tightening which would lead to diminishing global liquidity.

Nevertheless, historically, when interest rates are high and valuations are extremely stretched, the margin of error is small. So AI will have to continue to add value and productivity meeting or beating expectations. Major advances in hardware efficiency and energy sourcing are enabling AI to continue scaling, but future growth will hinge on sustained innovation and massive infrastructure build-out. New breakthroughs are making previously “impossible” scales feasible, though each step introduces new bottlenecks and demands careful coordination between tech, industry, and power sectors. But even more importantly, global liquidity will have to continue to trend higher. So far, this seems to be the case. Stay tuned.