Market Lab Report / Dr. K's Crypto-Corner

by Dr. Chris Kacher

The Evolution Will Not Be Centralized™

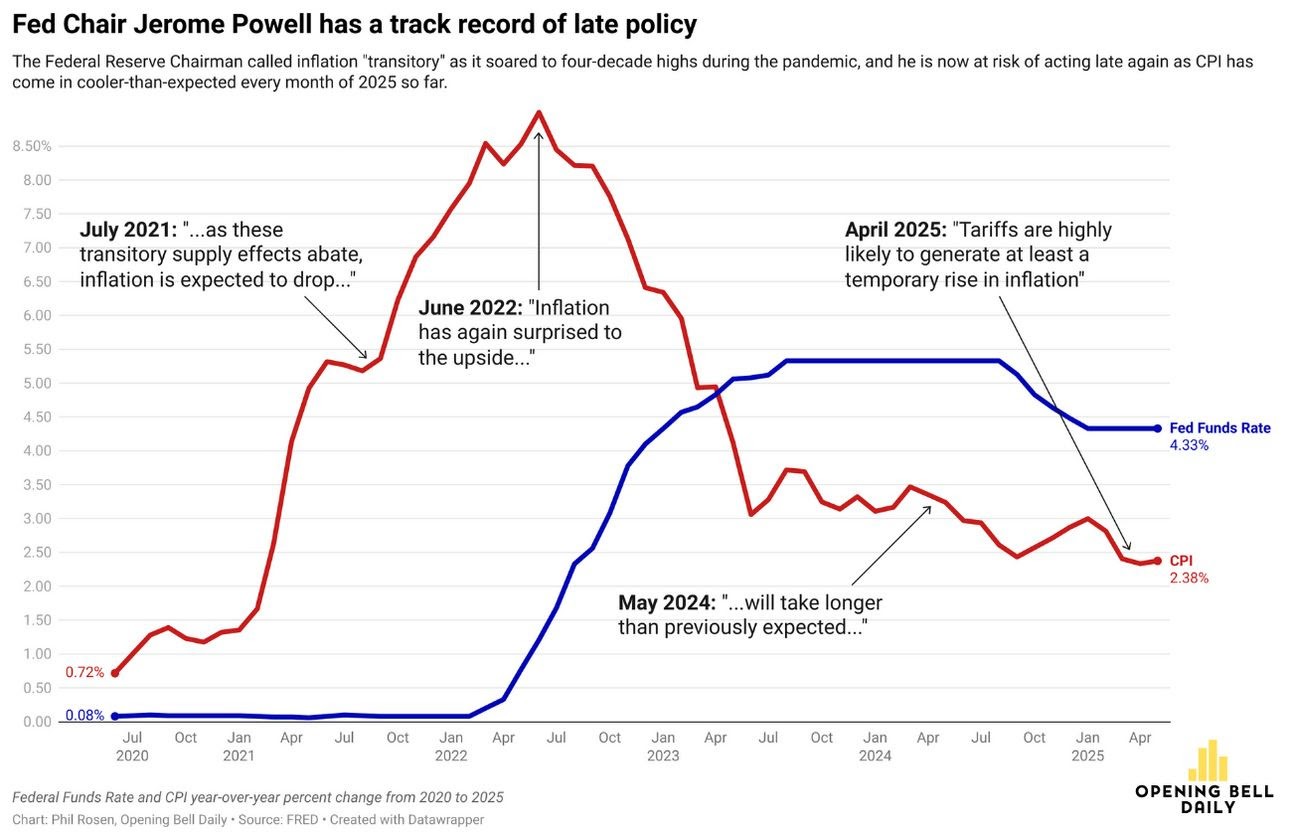

Trump vs. Powell on rate cuts

In a bold and unusually direct speech to close out last week, Fed Governor Christopher Waller laid out the case for an immediate rate cut. He said inflation is near the Fed’s 2% target, the labor market is weaker than it looks, and said that talk of tariffs fueling inflation is mostly noise. “Tariff increases are a one-time boost to prices that do not sustainably increase inflation,” Waller said.

He pointed out that wage growth has cooled, productivity is improving, and inflation expectations remain anchored, but that beneath the headline numbers, he is growing concerned. “With inflation near target and the upside risks to inflation limited, we should not wait until the labor market deteriorates before we cut the policy rate,” the Fed Governor said.

He says recent government job revisions suggests that private-sector job growth has stalled and job openings are evaporating faster than people assume. Furthermore, new university graduates face the worst job market in years.

Waller continues by stating, “If the slowing of economic and employment growth were to accelerate and warrant moving toward a more neutral setting more quickly, then waiting until September or even later in the year would risk us falling behind the curve of appropriate policy.”

Powell has a lengthy track record of being behind the curve, responding late to economic data, dating back to the pandemic’s four-decade high inflation spike.

Underscoring this point, Treasury Secretary Scott Bessent called for a sweeping review of the entire Federal Reserve system while US Representative Anna Paulina Luna formally referred Fed Chair Jerome Powell to the Justice Department over alleged misleading testimony to Congress. Bessent asked, “[H]as the organization succeeded in its mission? If this were the FAA and we were having this many mistakes, we would go back and look at why this has happened.”

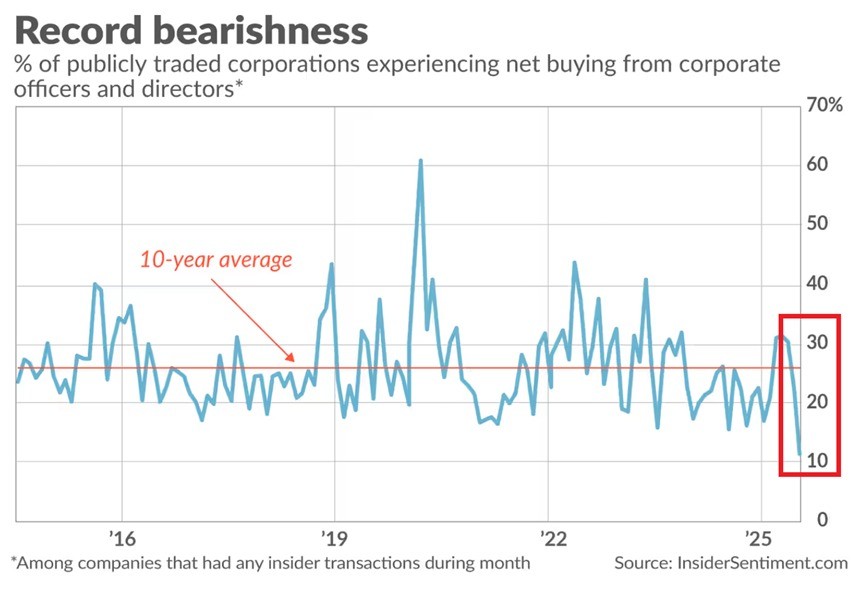

Insider selling at record levels

Corporate insiders are selling shares at the fastest rate in at least a decade, with roughly 89% of companies reporting more insider selling than buying in recent weeks. Insiders were either neutral or negative in 10 of the 11 S&P 500 sectors, with utilities being the only sector to show positive sentiment. This wave of selling is being interpreted by some market watchers as a strong signal that those with the best information believe valuations have run too far, too fast. However, some insider sales are triggered by pre-arranged plans or personal needs, not always a direct signal of pessimism about share prices.

Despite this negative insider sentiment, M2 global liquidity remains at all-time highs. The US M2 money supply reached a record $21.9 trillion in May 2025, reflecting ongoing easy financial conditions and central bank policies that have supported risk-taking and asset inflation.

Markets frequently decouple from fundamentals and sentiment during periods of excess liquidity, as asset prices are pushed up by the sheer volume of money, not just by company earnings or economic news.

Insiders’ extreme bearishness highlights significant caution about stretched market valuations and future growth. However, soaring global liquidity continues to fuel asset prices higher, defying insiders’ signals for now. While insiders might appear "wrong" in the short run, history suggests that liquidity-driven markets are fragile: should conditions tighten, insider caution could soon look prescient. For now, the market’s trajectory is defined more by the tide of global liquidity than by the warnings of corporate insiders.