Market Lab Report

by Dr. Chris Kacher

The Metaversal Evolution Will Not Be Centralized™

Wage price spiral?

The less-than-expected increase in wages at 0.3% vs. expectations of 0.4% drove last Friday's rally. The straight-up-from-bottom rally is also due in part to short covering which creates those sharp peaks during dead bat bounces.

CPI came in at expectations. No surprises. Shelter which remains a large part of inflation makes up 40% of the CPI. It can remain stubbornly high though the Fed has said they are aware of this thus are likely to put more weight on other shelter metrics which are less lagging such as the rate for new leases which is coming down. Further, PCE is the Fed's favored indicator.

Based on the current bounce, the market is brushing off the Fed's view of stubbornly high inflation which has many Fed members assuming the terminal rate will be at least 500-525 from 3 more 25 bps rate hikes. That said, CME Fed Futures assumes two more 25 bps rate hikes, not three, for a terminal rate of 475-500 bps. But of course, the number of rate hikes is data dependent. A number of Fed members as well as Goldman Sachs and Blackrock believe inflation will remain stubbornly high which will force the Fed to hike beyond the 500-525 bps terminal rate.

As for the 3.5% unemployment rate, the lack of those seeking work post COVID, the surge in retirees, and the Fed counting those who work 2 or 3 jobs as the creation of 2 or 3 jobs makes the reported figures look better than they are in reality, and explains how the unemployment rate dropped to 3.5% below estimates of 3.7%.

While wages cooled, a wage price spiral can still happen due to the low supply of workers. Demand, however, is also cooling as major companies such as Apple and Amazon lay off workers. Blackrock and Goldman Sachs believe unemployment will not soar due to the lack of supply and demand, but instead tick higher by just 0.5%. This would go against all other prior recessions when unemployment soared since companies eventually have to layoff more employees. It would seem based on the massive bubble that must be unwound that layoffs will be substantial thus the unemployment rate, while tempered by a significant number that are no longer looking for work, will still rise well beyond that of just 0.5%.

The Fed funds rate has never broken the downtrending line until now. Notice how a fast drop in the FFR was followed by recession. So just because the Fed pivots by halting then lowering rates does not mean markets are in the clear. Certainly prior major bubbles such as 1930-1932 and 2000-2002 are appropriate guides. So the current dead bat bounce is just that. Expect markets to reach new lows before they find their true floors.

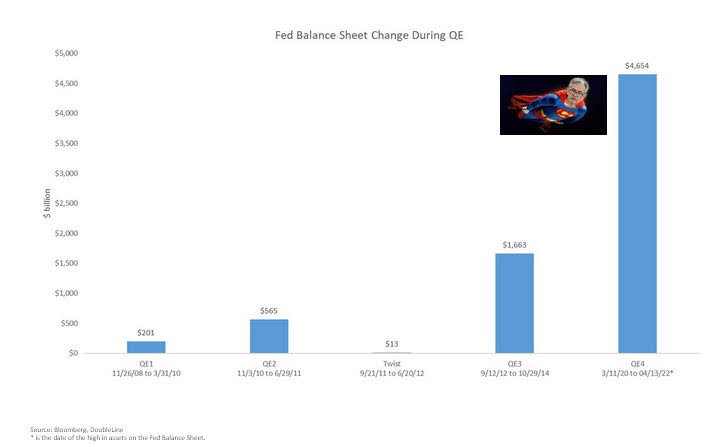

In consequence, the question is when, not if, something breaks that forces the Fed to pivot as companies layoff employees at a faster pace. The magnitude of the pivot will depend on the seriousness of the black swan. QE 1 to 3 was due to the financial collapse of 2008. QE4 was due to COVID. What might QE5 look like?