Market Lab Report / Dr. K's Crypto-Corner

by Dr. Chris Kacher

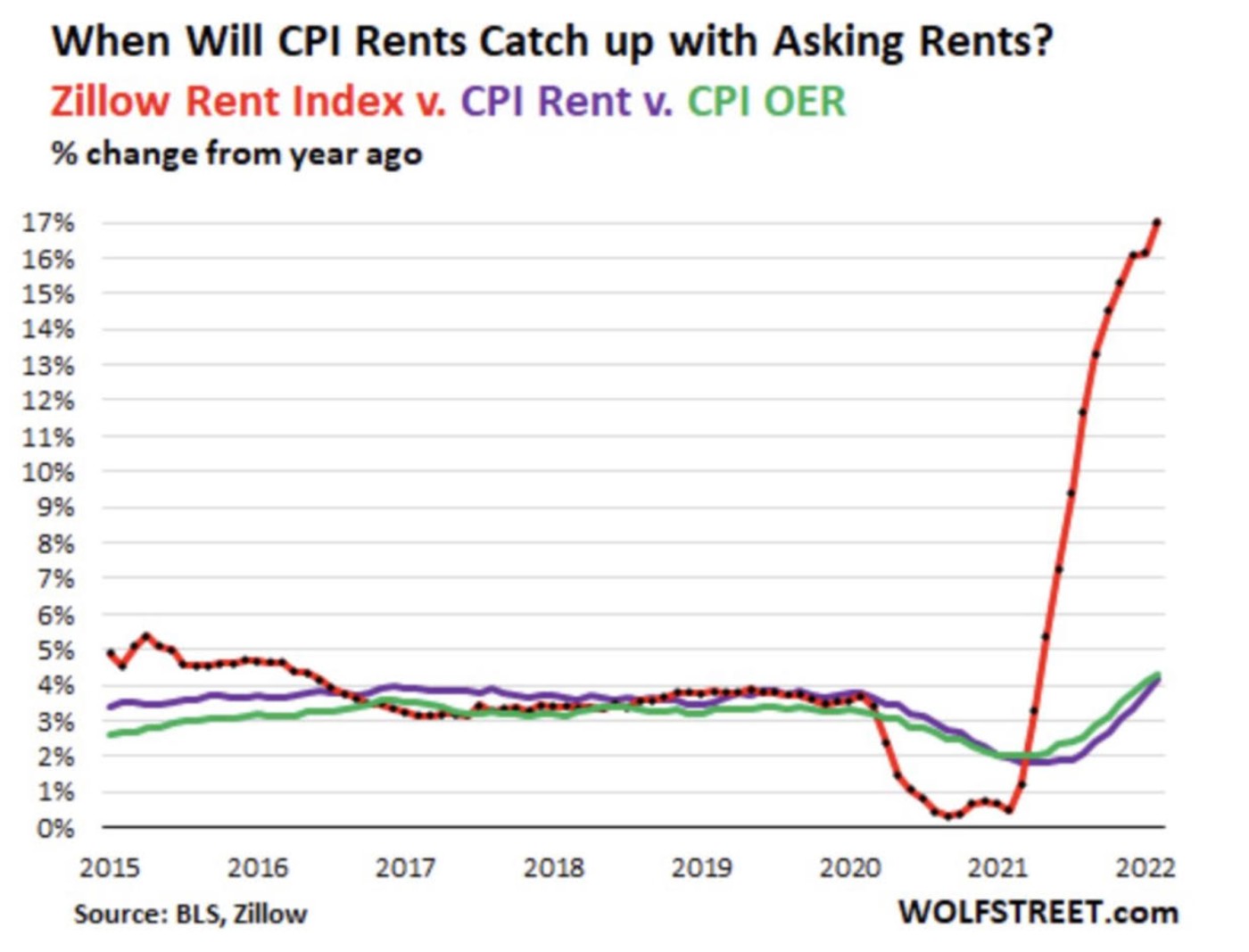

The Metaversal Evolution Will Not Be Centralized™

How will we know when the Fed will reverse course, or at least pause its hiking cycle? A -20% decline in the NASDAQ Composite hasn’t made them flinch, while the S&P 500 has only corrected about -14.6% peak-to-trough. Bond markets will eventually tell us that the hiking cycle is over when the yield curve begins to steepen aggressively; we are most likely a couple rate hikes or more ahead of this. Meanwhile, the curve continues to flatten with the spreads between the 2- and 10-yr Treasurys having narrowed to below 20 bps since Powell's rate hike decision on Wednesday Mar 16, which is the fixed-income market’s way of telling us the Fed is still committed to tightening monetary policy.

At any rate, until Powell signals a delay of future rate hikes as he did in Jan-2016 or a potential reversal to his hawkish position as he did in Dec-2018, expect the choppy downtrends to continue.

But regardless of Powell's actions, inflation has gotten away and has a long tail where it persists for typically at least 2 years. Thus the world is looking at double digit inflation out to at least 2024. While the question in the chart is one important elephant in the room, the same question could be asked about oil, gas, healthcare, education, housing, and used cars.

Historical trends in inflation/stagflation/depression

Powell believes wages are strong and will outpace inflation. Some want to know what he's smoking. Does the word "transitory" that he clung onto with dear life until he no longer could ring any bells? Prior long term debt cycles discussed in full by Ray Dalio of Bridgewater show that once debt gets to above 77% of GDP, the economy crosses the event horizon thus there is no return back to normal conditions.

Inflation starts to accelerate to where the central bank is forced to print more money. This, in turn, propels prices higher while wage inflation lags. This causes diminishing demand of goods and services forcing companies to reduce their prices so demand will increase. To spur demand, the central bank prints more money, so prices continue to climb. The level of M2 continues to increase overall during such periods. History shows M2 never materially decreases at these late stages of the cycle.

You then have a situation of high inflation and low growth, or stagflation. If the situation worsens to where demand lags further forcing companies to again lower their prices because demand continues to materially lag, you can have a serious depression where despite money being printed, demand continues to lag.

We are at the tipping point of runaway inflation and a depression. The U.S. Federal Reserve will do all it can do avoid a depression which would result in massive corrections beyond -50% in the stock market. If history is any guide, the Fed has no choice but to continue to print, pushing inflation higher which will push fiat's buying power lower, thus stoking the flames of populism which has led to vast social unrest, civil war, and/or revolution. So it is only a matter of time before correcting stock markets force Powell to reverse his hawkish stance.