The Nasdaq Composite has shown clear weakness recently, dropping about 5% from its late January peak near 24,000 down to roughly 22,600. The last few weeks featured more distribution days than accumulation, with heavier volume on down days and lighter volume on up days. This is a classic sign of selling pressure outweighing buying interest, especially in tech heavy names.

The big question is whether growing fears over excessive AI capital spending will overpower the supportive effects of quantitative easing, stealth liquidity injections, and overall global money printing. These forces have reliably driven equities higher across most of the past century.

Right now the AI overspend narrative is winning short term sentiment. Massive capex forecasts from the hyperscalers have already erased well over a trillion dollars in market value from the Mag7 and related stocks in the past month. Investors are increasingly asking whether the revenue and profit ramp from generative AI applications can justify the current pace of spending before margins get crushed or balance sheets strain. This has created a classic show me the money moment, and until clearer evidence of monetization appears, the froth is coming off the most speculative AI linked names.

That said, the liquidity backdrop remains exceptionally strong and historically very difficult to fight for long. Various facilities create capital via stealth QE since QE comes in many forms. The bullish case for higher markets hinges on the Federal Reserve's ongoing liquidity measures, which effectively function as a form of quantitative easing (QE) amid massive U.S. government debt rollovers, around $9.6 trillion in 2026 alone, much of it originally issued at near-zero rates but now refinancing at higher yields, pressuring fiscal balances and prompting central bank intervention to stabilize funding markets. By transitioning from quantitative tightening to reserve management purchases of up to $40 billion monthly in short-term Treasuries, the Fed injects liquidity that suppresses yields, bolsters bank reserves, and encourages risk-taking in equities, crypto, and other assets, much like past QE rounds that fueled multi-year bull runs (e.g., stocks surging 20-30% during QE3 and QE4 phases). This "stealth QE" not only absorbs excess debt supply but also amplifies economic growth through easier credit, potentially offsetting inflationary risks with productivity gains from AI and automation, creating an environment where asset prices inflate as money supply outpaces goods production, driving indices like the NASDAQ and S&P 500 higher once again.

Global central banks are also generally accommodative, repo markets are flush, fiscal deficits stay large, and rate cut expectations for 2026 are still solidly in place. These conditions tend to lift all boats eventually, even when individual sectors look bubbly or overextended.

My base case is that liquidity continues to dominate over the course of 2026. The structural tailwind of abundant money usually finds a way to bid up asset prices unless something dramatic breaks the regime such as a serious recession, sharp inflation re acceleration, or geopolitical shock large enough to force real tightening. AI spending concerns are legitimate and could easily drive a deeper correction in the Nasdaq, but they are unlikely to kill the broader bull market while central bank liquidity remains this supportive.

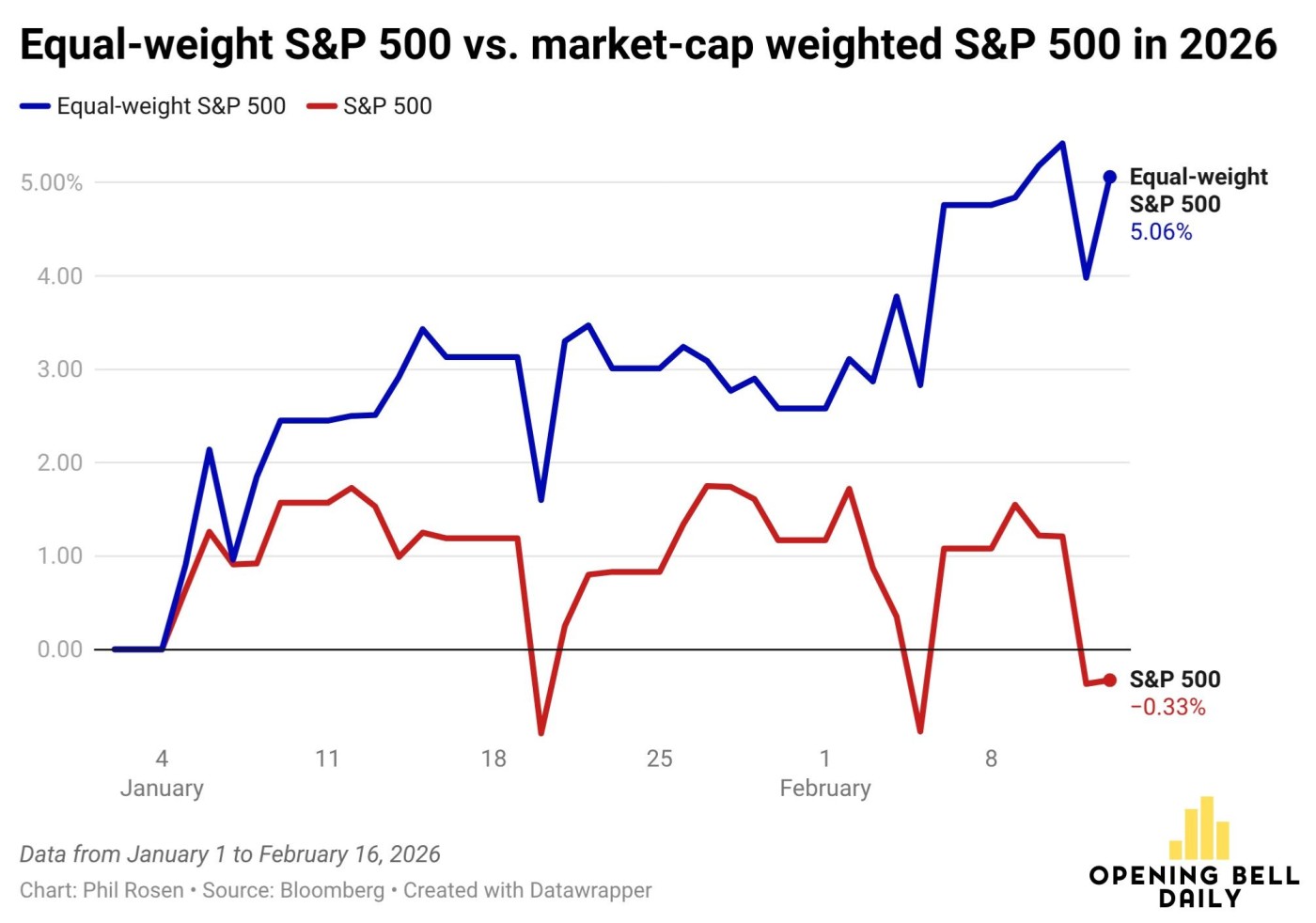

Further, the average S&P 500 stock is doing well while overvalued Big Tech has been weak. Capital has been rotating from tech to other sectors rather than leaving the market altogether. For the first time in years, gains are becoming less narrowly concentrated in a handful of trillion-dollar companies which has typically been a sign of improving market health as breadth and participation widen.

If and when AI dominance returns, we will see it in the price/volume action of leading names. We dont have to guess or speculate.

That said, when things look the ugliest, that has often been the time major averages find their lows. Continue to look for undercut & rally entry points, volume dry-ups, and pocket pivots in leading names.

In the meantime, more downside in overvalued names would not be surprising while selling pressure remains in this risk-off environment as the market digests AI return doubts. Initiating short sell entries in the names most vulnerable that rally into areas of logical resistance would be prudent.