by Dr. Chris Kacher

Why markets have bounced

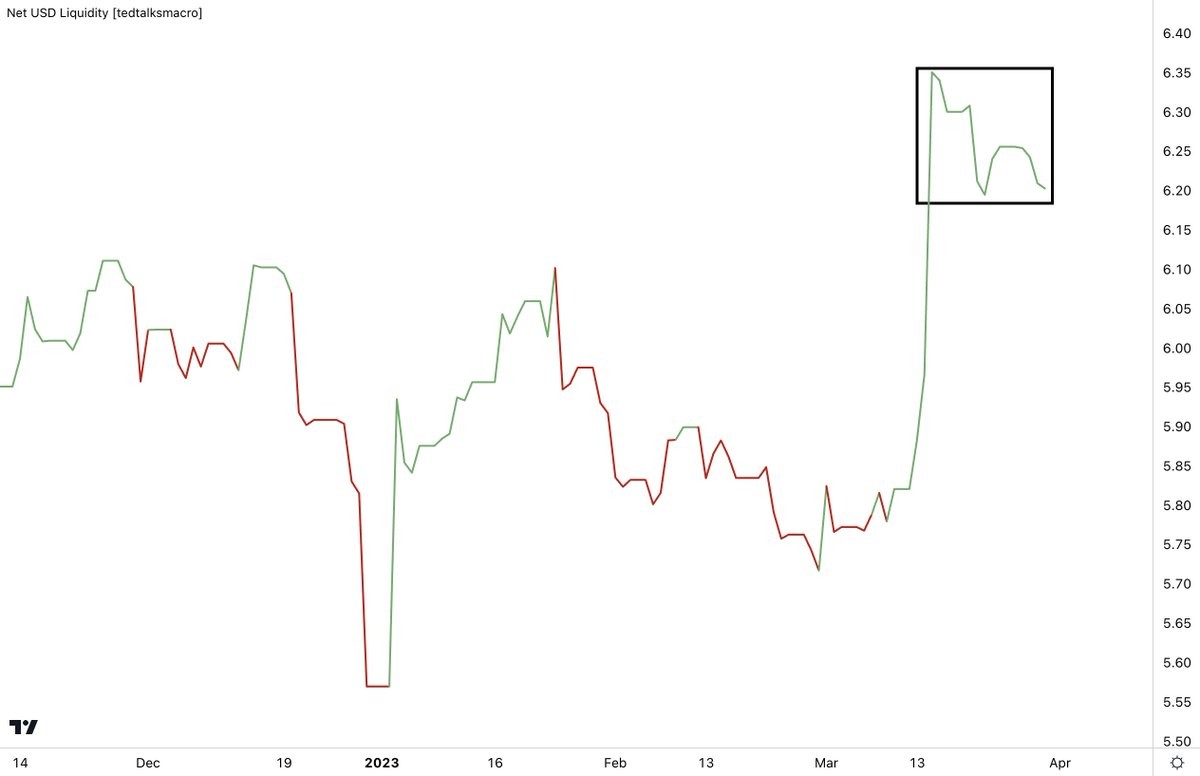

The sharp rise in stock and crypto markets since the banking disaster from Silicon Valley Bank and others is due to rescue liquidity injected by the Fed. The markets liked the strong economy, the added M2 liquidity, and moderating inflation.

But...

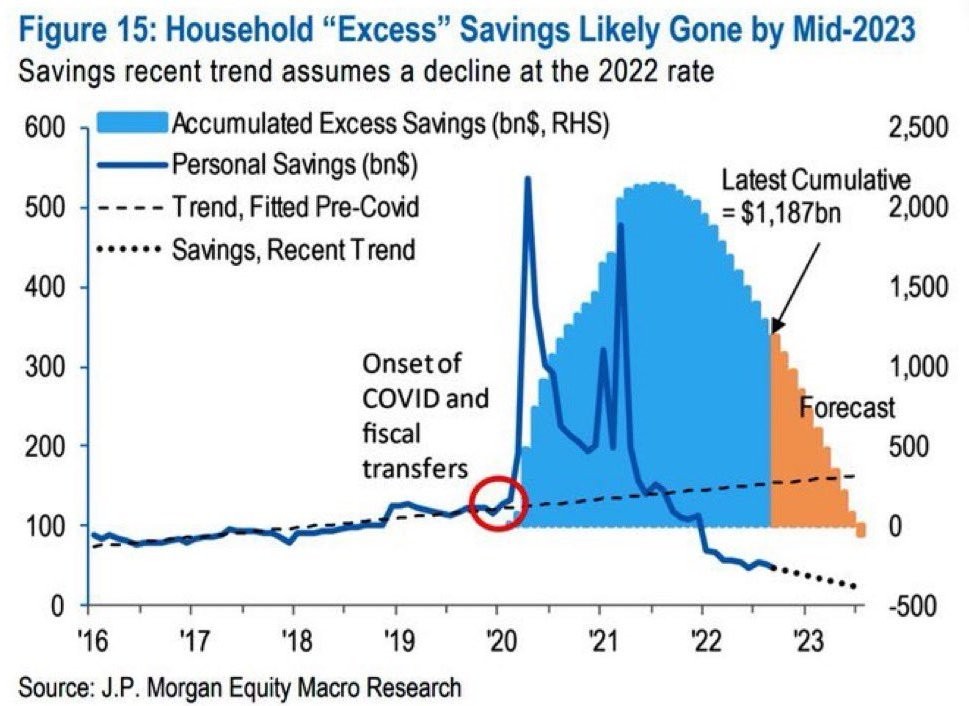

Savings are depleting fast while credit card debt soars.

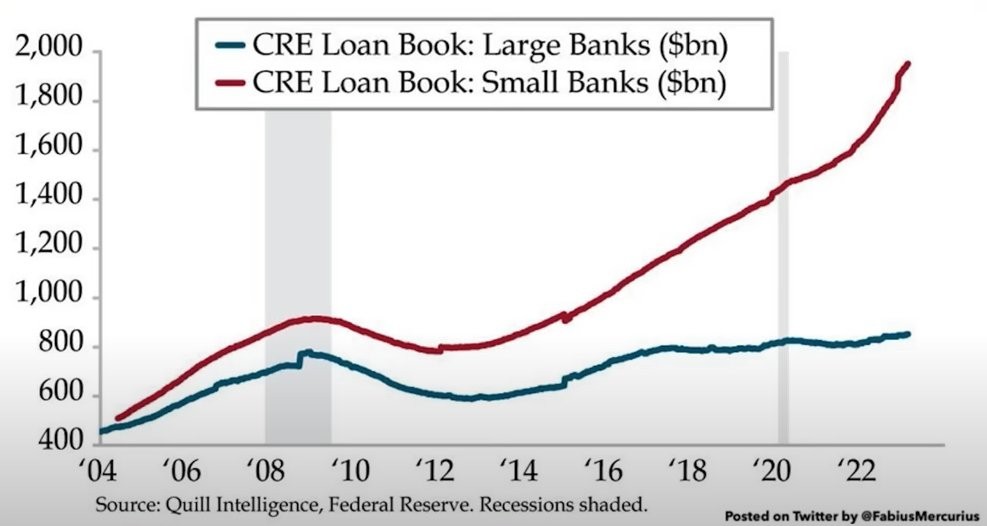

COVID programs which were stimulative have also come to an end. Over the next few months, we are looking at an elevated Fed terminal rate should inflation remain stubbornly high despite having moderated. Meanwhile, another domino in the name of commercial real estate could fall for the same reason that bank bond holdings got hit hard. Banks hold nearly $3 trillion in mortgage backed loans. Never has the Fed raised rates so fast from such low levels. This is causing deep losses in bonds which traditionally are low risk investments.

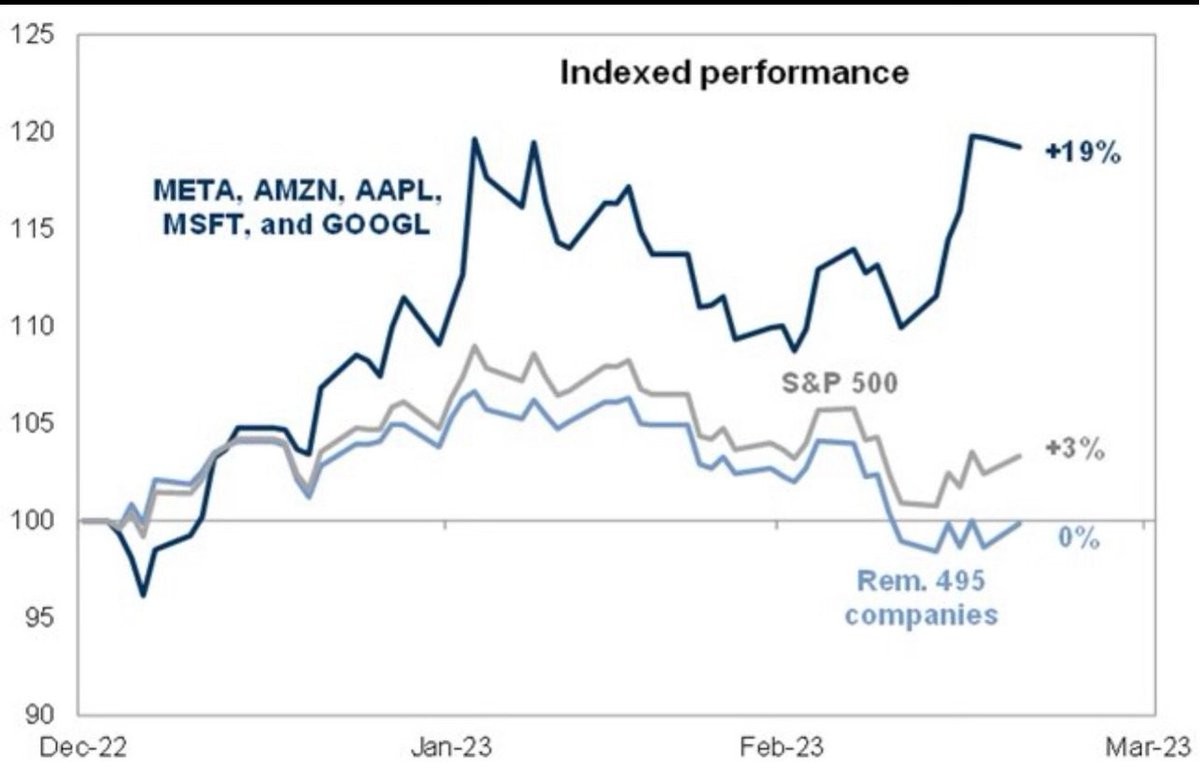

At present, the top technology companies represent about 1/5 of the stock market comprised of META, AMZN, AAPL, MSFT, and GOOGL. But if the terminal rate remains elevated, the lack of liquidity will hit these names and drive down markets.

The Fed's Barkin thinks the inflation battle will take time so will need to stay nimble in weighing fallout from bank stress against incoming inflation data. But tighter bank credit may offset the need for more rate hikes.

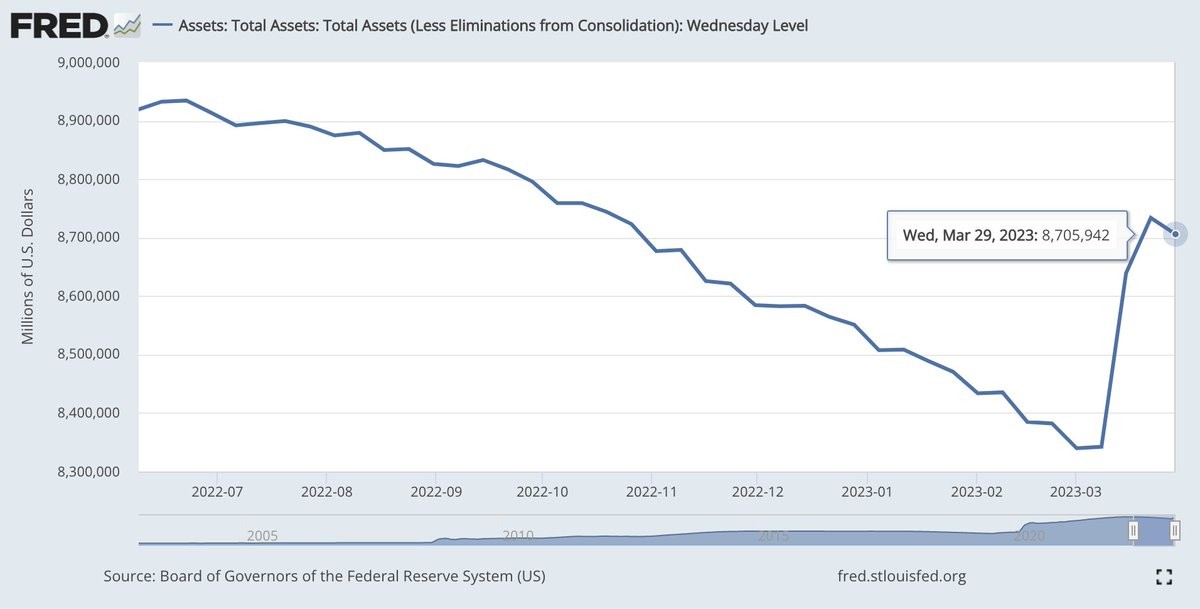

The Fed's balance sheet shrunk by ~$28bln in the last week. Discount window borrowing is down $22bln. This suggests the banking fears have eased but there are no guarantees that there won't be more banking issues.

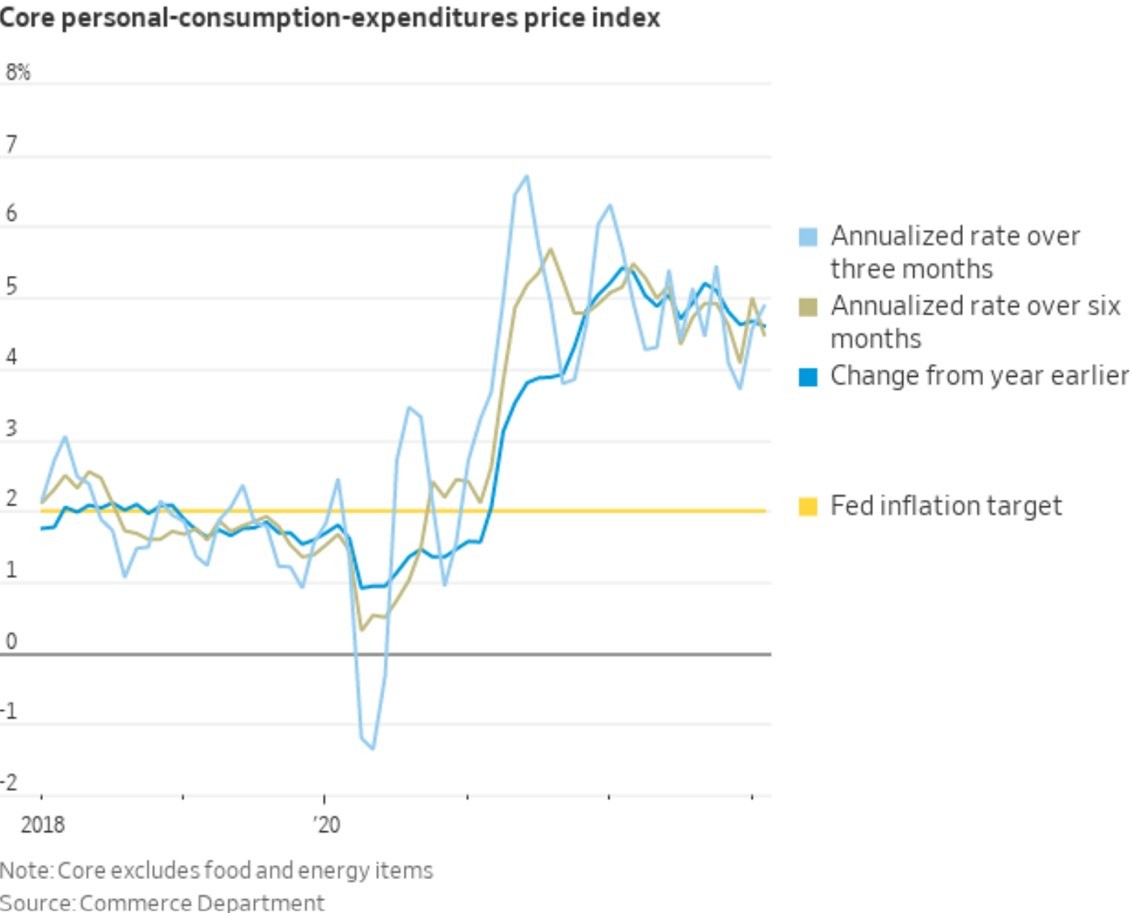

With a PCE coming in below estimates on a monthly basis, the market thinks yields may have topped, though the month before, PCE came in above estimates. Nevertheless, CME Fed Futures is pricing in zero or one more rate hike as both possibilities are probabilistically close, but that of course is subject to change with new data. The jobs report this Fri could once again point to a strong labor market which would make it more difficult for the Fed to pivot though at some point if history is any guide, unemployment will start to sharply rise.

The counterbalanceThe counter to the above is global M2 continues to rise. China recently cut its required reserve ratio by 25bp to 10.75% which further bolsters liquidity.

Any additional domino that tips will force the Fed to boost their balance sheet. This could be due to the $3-4 trillion put to banks as well as other connected black swans such as 1) unfunded liabilities from pensions and IRAs and 2) commercial real estate (CRE). This could restart the bull but at the price of even higher inflation but in such a scenario, the Fed would have little choice.

The choppy, event driven nature of the major averages since February has made this an environment where investors as a whole take on less risk, known as risk off, in the belief markets will fall. Indeed, the number of commodity trading advisers (CTAs) are currently betting about US$26 billion against the S&P 500, the largest short position since October 2021. This has created short squeezes the last 5 out of 5 times CTAs were this bearish. But that notwithstanding, there remain a number of cross currents at hand so it remains more of a shorter term trader's market unless you've been in our alt-currency trades such as precious metals.