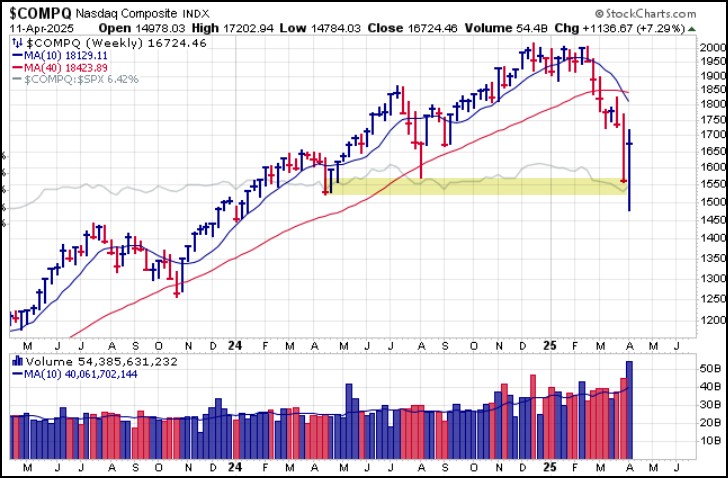

The market worked its way through a volatile week with the NASDAQ Composite and S&P 500 undercutting both their April and August 2024 lows, in large part due to President Trump announcing a 90-day delay on reciprocal tariffs for all countries that did not retaliate against Trump's original tariffs imposed two Wednesdays ago on the so-called Liberation Day. The 90-day delay did not apply to China, however, which remains in a tit-for-tariff bout of one-upmanship as both countries spent the week raising tariffs on each other.

Over the weekend, the President then declared a reversal of 145% tariffs for certain technology goods, including semiconductors and handsets. Apparently, the Administration's boast that 145% tariffs would quickly bring iPhone and other smartphone manufacturing back to the U.S. was all for naught.

Meanwhile, the major market indexes remain well below 200-dma resistance, but we can certainly expect a rally in futures overnight Sunday in response to the latest episode of Trump softening his stance.

While those portions of the media trumpet the President's actions as a trade policy master stroke, the reality is that the Administration likely responded to potential dislocations in the Treasury markets as foreign investors dumped dollar-denominated securities in response to the Tariff Tirade. Wednesday's 90-day tariff delay briefly stemmed the decline in Treasuries but the iShares 7-10 Year Treasury Bond (IEF) ETF continued to make lower lows on Friday as it attempts to hold 200-dma support.

While those portions of the media trumpet the President's actions as a trade policy master stroke, the reality is that the Administration likely responded to potential dislocations in the Treasury markets as foreign investors dumped dollar-denominated securities in response to the Tariff Tirade. Wednesday's 90-day tariff delay briefly stemmed the decline in Treasuries but the iShares 7-10 Year Treasury Bond (IEF) ETF continued to make lower lows on Friday as it attempts to hold 200-dma support.

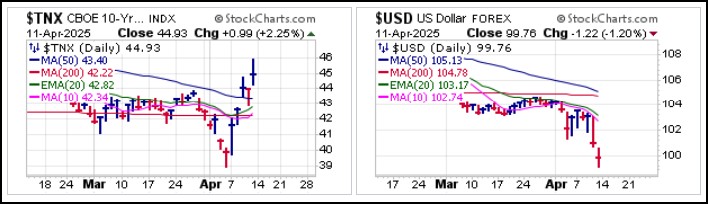

Strange cross-currents abound. Despite the conventional economic wisdom that tariffs as well as rising interest rates should be bullish for the U.S. Dollar ($USD) we see that rising rates via the 10-Year Treasury Yield ($TNX), along with the tariffs, are in fact sending the dollar lower as it tests three-year lows.

This all speaks to the dumping of dollar-denominated securities by foreign countries and a sharp move into gold as an alternative reserve currency. The Continuous Gold Futures Contract ($GOLD) posted a new all-time high of $3,245.22 an ounce on Friday, ending the week at $3,236.55. Meanwhile, major brokerages like Goldman Sachs (GS) have raised their 2025 gold price target to $3,525 with an upside tail-risk of $4500 depending on the situation once the full level and array of tariffs is known. UBS Securities (UBS) and Deutsche Bank (DB) have also chimed in with new 2025 price targets of $3,500 and $3,350, respectively.

As the tariff situation continues to develop, and the news flow shifts depending on how aggressive the Trump Administration remains and whether any countries are able to strike trade deals with the U.S. during the 90-day delay, expect a potentially uninvestable environment where extreme news-generated volatility may be the order of the day. This remains a very dangerous market, and cash remains king for now, temporary news-generated reaction rallies such as we may see overnight on Sunday and into Monday morning notwithstanding.

The Market Direction Model (MDM) remains on a CASH signal.