Major market indexes corrected slightly this past week and turned positive on Thursday ahead of the long three-day Easter Holiday weekend. The NASDAQ Composite tested its 10-day moving average on Thursday and Friday and held as it tests the mid-February high on the upside. Many are trying to call this a new bull market but we do not believe underlying conditions are capable of producing anything other than short-term trends in either direction.

Pundits and talking heads cite the NASDAQ's rally in 2023 in percentage terms as confirmation of a new bull market while others attempt to impose what is mostly an antiquated indicator, the O'Neil style follow-through day. Others will cite the NASDAQ's movement above the prior declining tops trendline formed during 2022. We would argue that after an initial leg down, such movements above declining tops trendlines are inevitable as an index moves mostly sideways and forms a bear flag/pennant. We believe that this is a reasonable possibility, since under the cosmetic surface of the major market indexes, individual stocks are another matter altogether. Financials, industrial metals, travel, retail, and many other groups remain weak. Big-stock techs have rallied but we view this as a narrow defensive rotation into long-term established, reliable big-cap tech juggernauts. True leadership that is normally seen at the start of a bona fide new bull market is simply not there.

The risk-on Russell 2000 also continues to lag the other major indices as it trades in a back-and-forth manner at levels seen nearly a year ago, and hardly the strong uptrend seen after the Fed had to create trillions of dollars due to COVID.

Gold and silver continue to benefit from the lifeboat trade. Despite the assurances of Fed and other government bureaucrats that the recent banking crisis is past us and that the banking system remains sound, financials stocks have remained in bear flags following the March breakdowns in the wake of the SVB Financial Group (SIVB) and Signature Bank (SBNY) collapses. Since early March, gold and silver have marched higher, with gold posting a near-term breakout three weeks ago. This past week it moved decisively past the $2,000 level, even after Citigroup (C) put a recommendation to short gold a full two weeks ago. We view the 10-day moving average as potential, buyable support for the VanEck Merk Gold Trust (OUNZ) with the 20-dema just below as a secondary support level since we believe strong price support exists at the $1950 level, although the $2000 level may serve as strong psychological support in the near-term.

Fresh statistics are out regarding Central Bank purchases of gold in the first quarter of 2023, showing that global Central Banks bought more gold in Q1 2023 than in any other quarter since 2010. This comes on the heels of global Central Banks buying more gold in 2022 than in any other year since before World War II. The move was mainly motivated by increasing concern about a possible global financial crisis, coupled with concerns over rising economic risks in reserve currency economies. Fiat has been a sinking titanic as M2 never materially decreases in every long term debt cycle but instead accelerates as these debt cycles which typically last 75 to 100 years come to an end.

Fresh statistics are out regarding Central Bank purchases of gold in the first quarter of 2023, showing that global Central Banks bought more gold in Q1 2023 than in any other quarter since 2010. This comes on the heels of global Central Banks buying more gold in 2022 than in any other year since before World War II. The move was mainly motivated by increasing concern about a possible global financial crisis, coupled with concerns over rising economic risks in reserve currency economies. Fiat has been a sinking titanic as M2 never materially decreases in every long term debt cycle but instead accelerates as these debt cycles which typically last 75 to 100 years come to an end. Meanwhile, silver attempts to compress the gold:silver ratio which has been at historically elevated levels for some time. This past week silver broke out as it quickly worked through overhead price congestion formed back in December and January. The Aberdeen Physical Silver Trust (SIVR) remains in a buyable position on this breakout but of course we would be alert to any pullback down to the 10-day moving average as a more opportunistic entry if we can get it, based on how volatile silver tends to be relative to gold

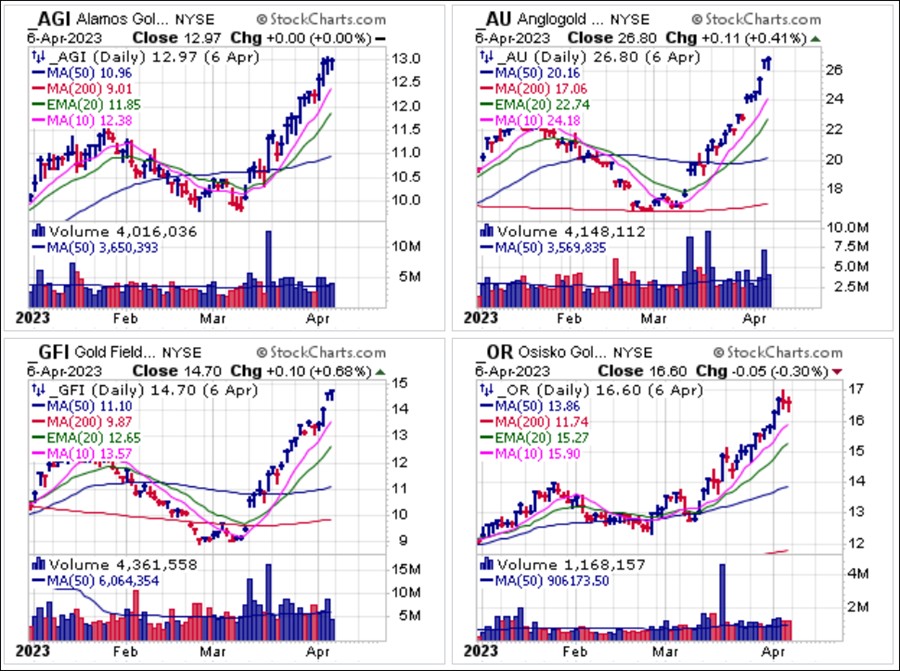

We have also liked a number of precious metals names over the past several weeks, including strong junior miners like Alamos Gold (AGI) and larger-cap senior names like AngloGold-Ashanti (AU) and Gold Fields Ltd. (GFI). We have viewed Osisko Gold Royalties Ltd. (OR) as the leading name in the space based on the fact that it does not mine metal itself, but instead owns royalty streams from other mining companies' gold and silver production, thus making its cost structure immune to current inflation.

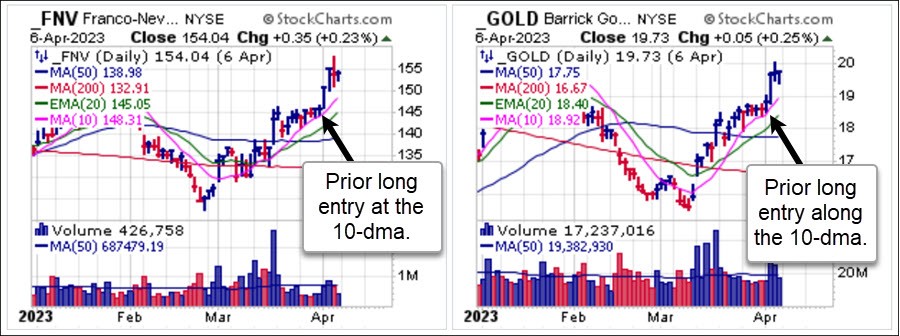

We have also liked a number of precious metals names over the past several weeks, including strong junior miners like Alamos Gold (AGI) and larger-cap senior names like AngloGold-Ashanti (AU) and Gold Fields Ltd. (GFI). We have viewed Osisko Gold Royalties Ltd. (OR) as the leading name in the space based on the fact that it does not mine metal itself, but instead owns royalty streams from other mining companies' gold and silver production, thus making its cost structure immune to current inflation. Last weekend we tagged two names in the group, royalty stream owner Franco-Nevada (FNV) and senior miner Barrick Gold (GOLD) as buyable stocks. Both stocks showed identical patterns as they held tight along their 10-day moving averages with volume declining, which according to our methods offers a lower-risk entry using the 10-dma as a selling guide. Both stocks then went on to post pocket pivots on Monday and Tuesday as they shot higher. If anyone was looking for some fresh names to buy in the group given its current compelling leadership position, we handed them to you on a silver (no pun intended) platter in last weekend's Focus List Review.

Last weekend we tagged two names in the group, royalty stream owner Franco-Nevada (FNV) and senior miner Barrick Gold (GOLD) as buyable stocks. Both stocks showed identical patterns as they held tight along their 10-day moving averages with volume declining, which according to our methods offers a lower-risk entry using the 10-dma as a selling guide. Both stocks then went on to post pocket pivots on Monday and Tuesday as they shot higher. If anyone was looking for some fresh names to buy in the group given its current compelling leadership position, we handed them to you on a silver (no pun intended) platter in last weekend's Focus List Review.

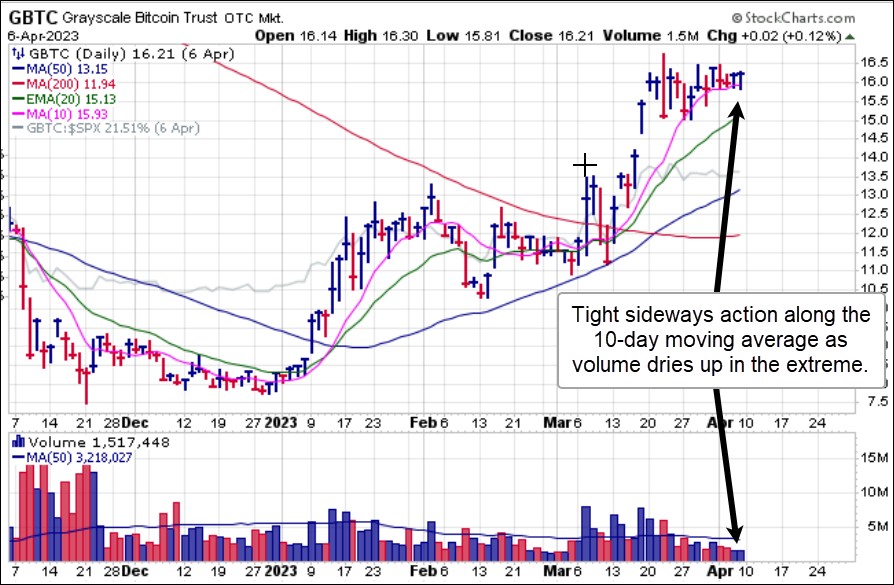

While Bitcoin ($BTCUSD) has lagged the precious metals over the past 2-3 weeks, the technical action remains highly constructive. Using the daily chart of the Grayscale Bitcoin Trust (GBTC) we can see that it is holding extremely tight as volume dried up to -52.9% below average on Thursday. This puts it in a buyable position using the 10-dma as a tight selling guide and the 20-dema as a wider selling guide depending on one's risk preference.

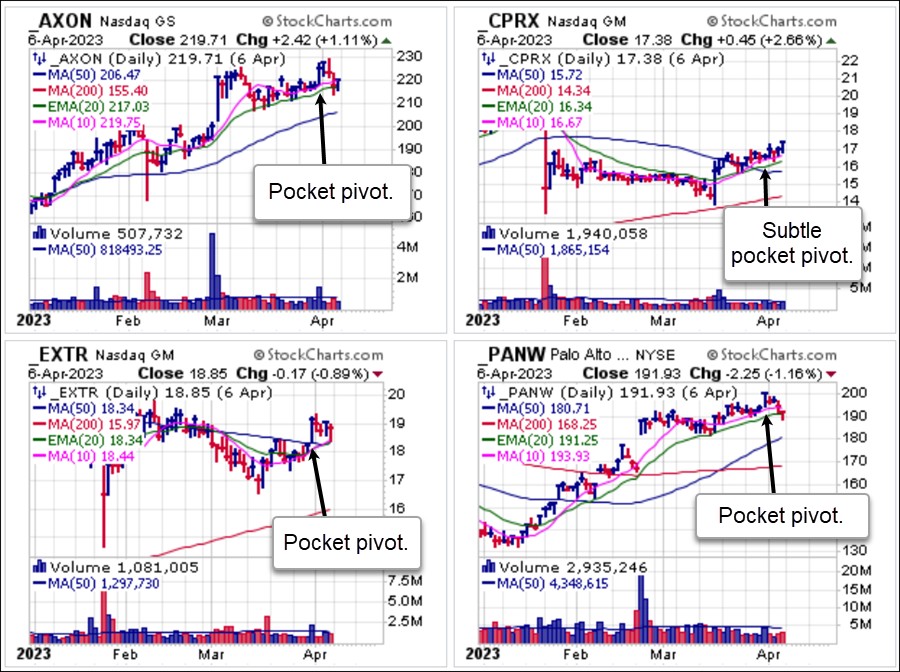

While Bitcoin ($BTCUSD) has lagged the precious metals over the past 2-3 weeks, the technical action remains highly constructive. Using the daily chart of the Grayscale Bitcoin Trust (GBTC) we can see that it is holding extremely tight as volume dried up to -52.9% below average on Thursday. This puts it in a buyable position using the 10-dma as a tight selling guide and the 20-dema as a wider selling guide depending on one's risk preference. Last weekend we discussed some pocket pivots in several stocks, including AXON Enterprise (AXON), Catalyst Pharmaceuticals (CPRX), Extreme Networks (EXTR), and Palo Alto Networks (PANW). These were some of the few interesting charts we saw last week, but note that all these pocket pivots were immediately met with pullbacks to moving average support. This is very typical for this market, and we adjust to this by always looking for potentially buyable pullbacks closer to the moving average following a pocket pivot that occurs at or through a particular moving average. AXON pulled down and shook out at its 20-dema on Wednesday and Thursday, CPRX quickly tested the 20-dema and then move to higher highs by the end of the week, and EXTR pulled into its 50-dma and held buyable support at the line on Friday. PANW is the weakest of the three as it pulled back all week and by Thursday closed just above the 20-dema which is a much lower-risk entry using the 20-day line as a selling guide than chasing last week's pocket pivot. This is how we favor handling pocket pivots once they get even slightly extended in the current market environment.

Last weekend we discussed some pocket pivots in several stocks, including AXON Enterprise (AXON), Catalyst Pharmaceuticals (CPRX), Extreme Networks (EXTR), and Palo Alto Networks (PANW). These were some of the few interesting charts we saw last week, but note that all these pocket pivots were immediately met with pullbacks to moving average support. This is very typical for this market, and we adjust to this by always looking for potentially buyable pullbacks closer to the moving average following a pocket pivot that occurs at or through a particular moving average. AXON pulled down and shook out at its 20-dema on Wednesday and Thursday, CPRX quickly tested the 20-dema and then move to higher highs by the end of the week, and EXTR pulled into its 50-dma and held buyable support at the line on Friday. PANW is the weakest of the three as it pulled back all week and by Thursday closed just above the 20-dema which is a much lower-risk entry using the 20-day line as a selling guide than chasing last week's pocket pivot. This is how we favor handling pocket pivots once they get even slightly extended in the current market environment.

Friday's BLS jobs report looked like a big nothing burger with index futures relatively unchanged. New non-farm monthly payrolls came in at 236,000, just below the 238,000 that were expected. In our view, this remains an unstable market environment that is still subject to event risk. Over the weekend, news that the last two weeks of March saw bank credit contract the most ever indicates that liquidity may remain an issue for this market. Thus, it is not a market for intermediate- to longer-term trend-following investors, although we believe the alternative-currency lifeboat trade may offer more intermediate-term prospects, and of course we have been on it in these reports.

The Market Direction Model (MDM) switched to a BUY signal on Monday, April 3rd and then switched back to a CASH/NEUTRAL signal on Wednesday, April 5th. Markets will likely remain in a choppy environment as stealth QE continues to push M2 higher but institutional investors look to sell into strength as recession looms. Liquidity rose due to the banking disaster but is countered by bank credit contraction. The Fed will only print just enough as it continues to battle inflation. That said, China and Japan continue to contribute to the overall rise in global M2, thus adding to the riptide nature of this market so far this year. If inflation remains stubbornly high, the Fed may have to keep rates at elevated levels which will keep liquidity scarce.