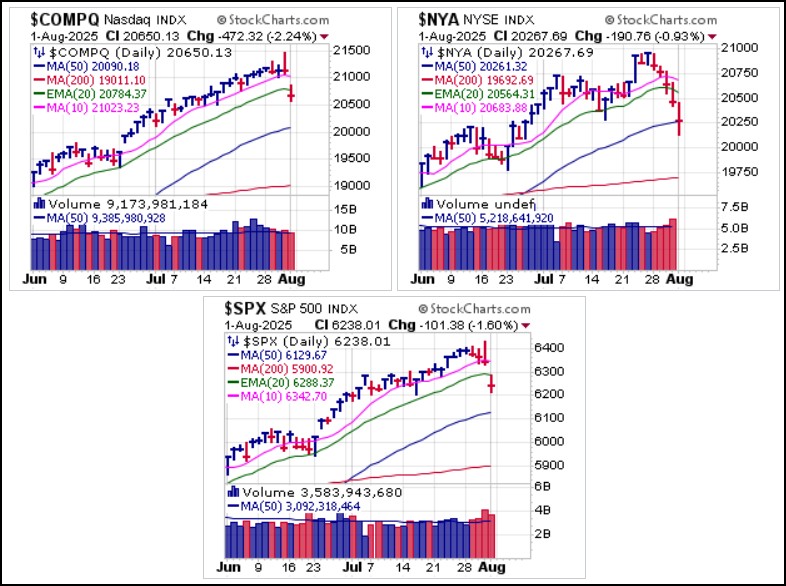

Stocks had a rough week as a feeble jobs report from the Bureau of Labor Statistics, combined with some very severe downward revisions of prior jobs numbers, sent stocks slashing lower to end the week on a very sour note Friday. Total nonfarm payroll employment in the U.S. increased by 73,000 jobs in July vs. expectations of 102,000, with the unemployment rate remaining steady at 4.2%. Significant revisions were made to prior months' data, specifically for May and June 2025, which were notably lower than initially reported. May nonfarm payrolls, initially reported as a gain of 144,000 jobs, were revised down by 125,000 while June nonfarm payrolls, initially reported as a gain of 147,000 jobs, was revised lower by 133,000.

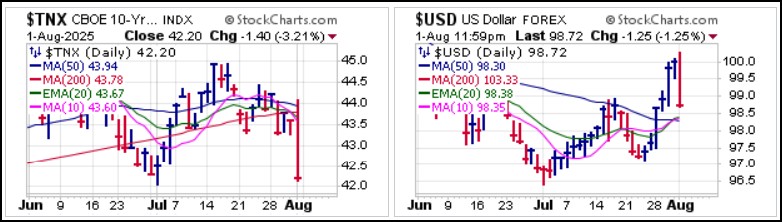

Interest rates across the yield curve and the U.S. Dollar ($USD) plummeted in response to the weak current and revised jobs numbers.

Interest rates across the yield curve and the U.S. Dollar ($USD) plummeted in response to the weak current and revised jobs numbers.

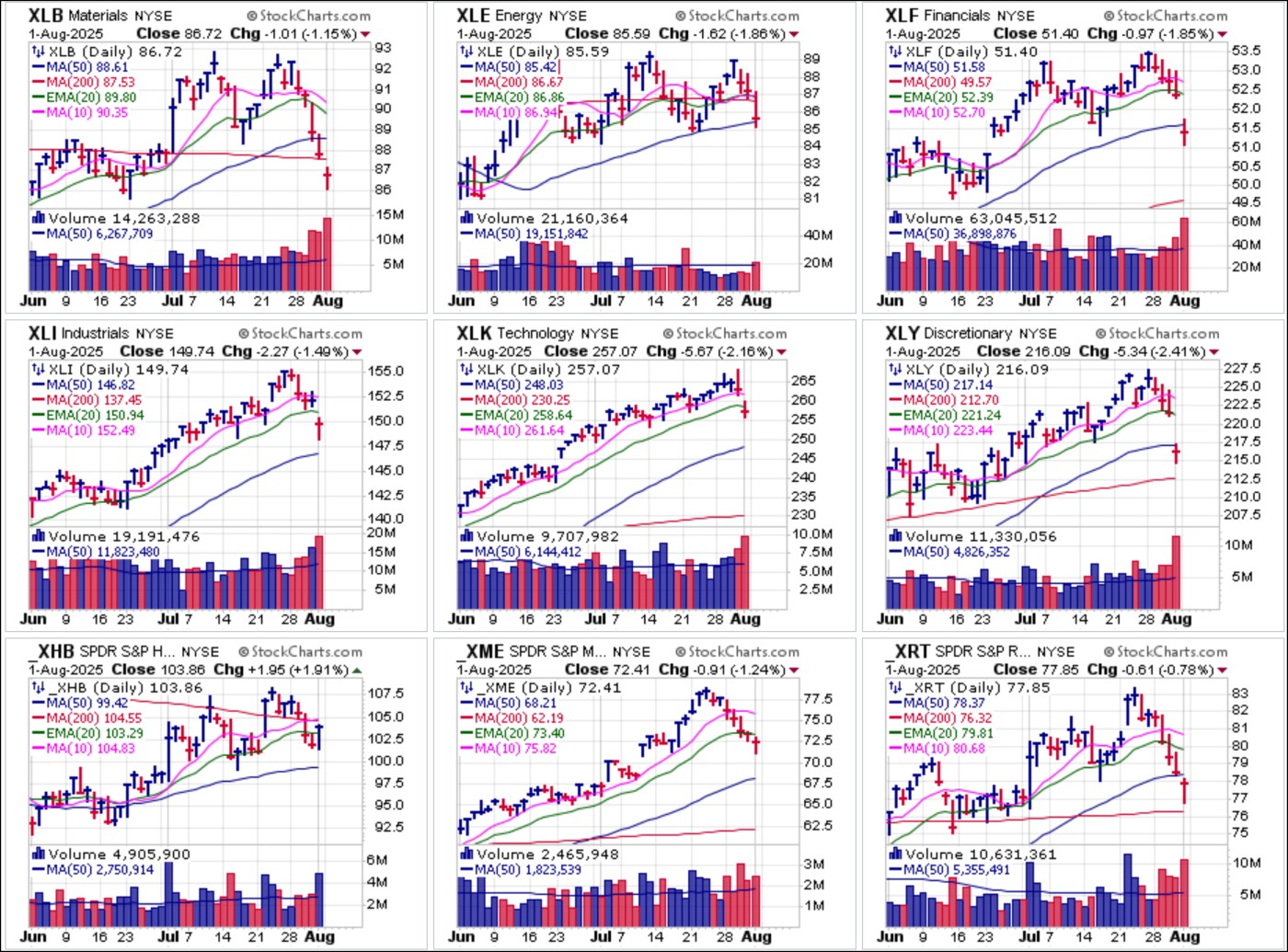

Selling was broad and persistent heading right into Friday, with only the S&P Select Sector Homebuilders (XHB) ETF closing up on the day as homebuilding stocks bounced on the hopes of lower mortgage rates that would in turn induce demand for new homes. If the economy is indeed weakening, however, then homebuilders will likely suffer such that Friday's rally may simply bring the XHB into short-selling range near the 200-dma.

The severity of the technical damage indicates that it is likely the market and individual stocks will require some time to heal, whether as sideways action, a continuation of a standard market correction, or an outright bear market. For now, that is unknown, and investors who are long stocks should review their risk-management plan and the appropriate trailing stop price levels.

Interestingly, gold and silver rallied in response to the BLS report that in turn sparked a sharp downside break in interest rates and the $USD, but crypto-currencies Bitcoin ($BTCUSD) and Ethereum ($ETHUSD) both sold off, breaking moving average support at the 10-dma and 20-dema along the way. $BTCUSD is now approaching 50-dma support. Gold via the SPDR Gold Trust (GLD) tested the prior late June low on Thursday and then gapped back above three moving averages to post a moving average undercut & rally (MAU&R) long entry with the idea that it should hold the 50-dma to remain viable. The iShares Silver Trust (SLV) also gapped higher after finding VDU support at the 50-dma, technical long entry that perhaps presaged the weak Friday jobs numbers.

Interestingly, gold and silver rallied in response to the BLS report that in turn sparked a sharp downside break in interest rates and the $USD, but crypto-currencies Bitcoin ($BTCUSD) and Ethereum ($ETHUSD) both sold off, breaking moving average support at the 10-dma and 20-dema along the way. $BTCUSD is now approaching 50-dma support. Gold via the SPDR Gold Trust (GLD) tested the prior late June low on Thursday and then gapped back above three moving averages to post a moving average undercut & rally (MAU&R) long entry with the idea that it should hold the 50-dma to remain viable. The iShares Silver Trust (SLV) also gapped higher after finding VDU support at the 50-dma, technical long entry that perhaps presaged the weak Friday jobs numbers.

This is where risk management skills and plans become relevant, while also considering taking profits where they exist and raising cash levels for the purpose of capitalizing on any potential opportunities that a sustained market sell-off may create.

The Market Direction Model (MDM) remains, for now, on a BUY signal that was issued on May 20, 2025.