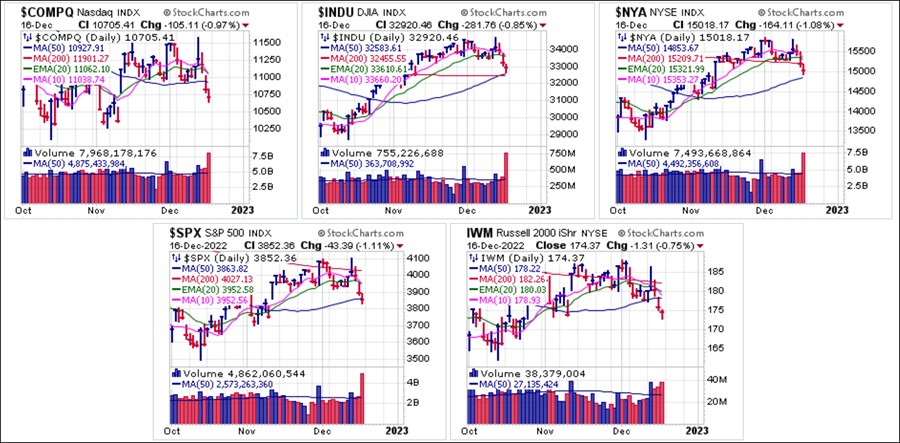

Major market indexes broke to the downside following the Fed policy announcement on Wednesday after the Fed raised its inflation estimates and its terminal rate for the current rate-raising cycle at 5.1-5.4%. That sent the market lower heading into Friday's quadruple-witching options expiration as the S&P 500, the NASDAQ Composite, and the Russell 2000 Indexes all closed below their 50-day moving averages. The leading index, the Dow Jones Industrials, found support at its 50-day moving average, but as we have already said before, we have never seen a bull market begin when it is led by a narrow risk-off 30-stock index like the Dow.

The idea that the Fed will engineer a so-called soft landing strikes us as comical given the Fed's historical track record in this regard. The Fed had no clue last year that they would be raising rates so aggressively this year as they respond in hindsight to inflation that last year they assured us was only transitory. Today, Fed Chairman Jerome Powell speaks confidently about how high and for how long they will raise interest rates as if they know and have everything buttoned-down and under control. In our view, nothing could be further from the truth.

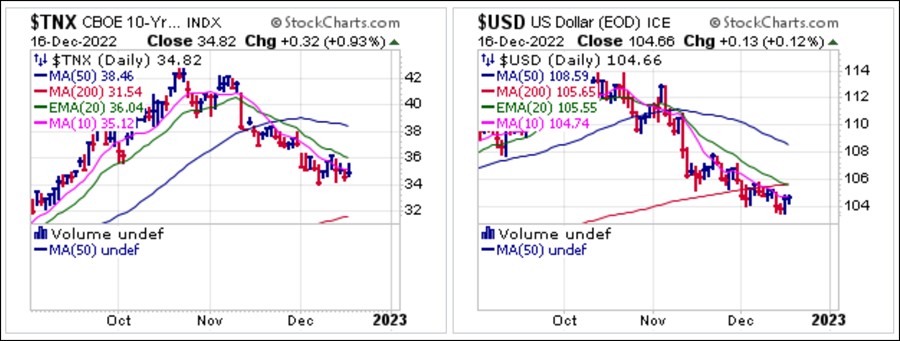

The idea that the Fed will engineer a so-called soft landing strikes us as comical given the Fed's historical track record in this regard. The Fed had no clue last year that they would be raising rates so aggressively this year as they respond in hindsight to inflation that last year they assured us was only transitory. Today, Fed Chairman Jerome Powell speaks confidently about how high and for how long they will raise interest rates as if they know and have everything buttoned-down and under control. In our view, nothing could be further from the truth.As interest rates and the dollar decline, they offer clues as to the market's assessment of just how soft of a landing the Fed will engineer. In reality, they are driving full-speed at a brick wall and will likely not know they have hit a wall that they cannot see until it is too late.

Precious metals are also presaging an out-of-control Fed that will likely shift into reverse long after the market has figured out that they will, just as was the case with respect to inflation. The Sprott Physical Gold Trust (PHYS) and the Sprott Physical Silver Trust (PSLV) remain in strong uptrends off their October an November lows, and despite Fed talk of raising rates higher for long have not given up much of their recent gains. For now, these both remain in positions where we primarily view pullbacks to their respective 20-day exponential moving averages as the best, lower-risk entry possibility now that these have become extended to the upside.

Many members have wanted us to give in to those who erroneously declare that the market is in a confirmed uptrend as it starts a new bull market, but we see no reason to follow what we consider to be incompetent analysis by those intent on selling newspapers. While we believe that the Fed will almost certainly be forced to shift direction sometime in 2023, perhaps earlier, perhaps later, for now the market remains a treacherous landscape.

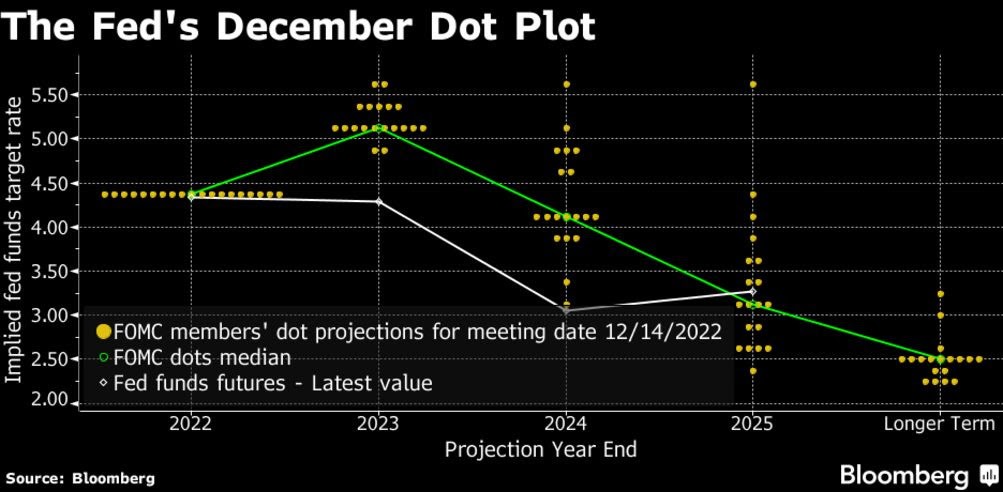

The dot plot shows us the FOMC member’s predictions have shifted as 17/19 members now see rates at or above 5.1% at December 31st, 2023, an increase from last month. This is in keeping with Goldman Sach's prediction that due to the macro environment and persistently high inflation, the Fed will have no choice but to hike by 25 bps increments beyond the 475-500 terminal rate.

The macro environment is the worst we've seen over this long-term debt cycle which started at the end of WW II. Unlike the equity market, the fixed-income market is indicating that bond investors don’t believe the Fed will raise rates past 5%. The bond market thinks something is likely to break by the time the FFR gets to 475-500, or two more 25 bps rate hikes as predicted by CME Fed Futures.

So despite history showing the FFR needs to exceed inflation to have a material effect, it is more likely that a domino effect is unleashed or even a black swan which will force the Fed to halt then lower rates, even in the face of high inflation. Fiat is a sinking titanic so as conditions worsen, so does inflation and debt. This is not the 1970s when debt was small and interest rates were much higher allowing the Fed to first hike rates to record levels to break the back of inflation, then aggressively lower rates to kick off the big bull market of the 1980s.

The Market Direction Model (MDM) remains on a SELL signal.