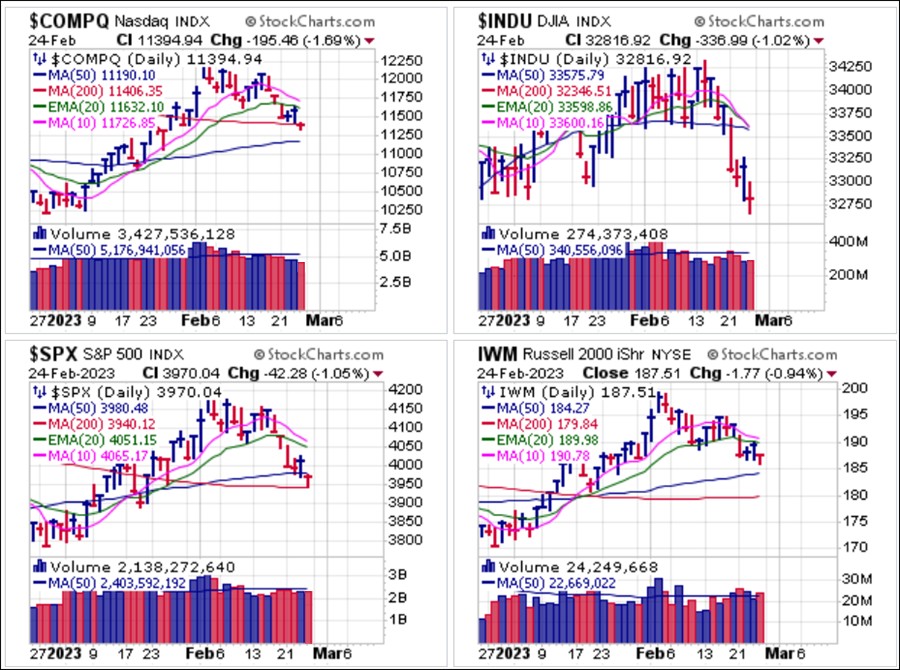

Major market indexes all closed lower at week's end, continuing what has been a two- to three-week sell-off from the early February highs. the NASDAQ Composite closed Friday below its 200-day moving average while the S&P 500 closed below its 50-day moving average but found intraday support at its lower 200-day moving average. Volume was slightly lower on the NASDAQ and just barely higher on the NYSE.

Strong Personal Consumption Expenditures price data on Friday, the Fed's favorite measure of inflation, came in hotter than expected at 0.6% month-over-month vs. expectations of 0.4%. This along with the hot Producer Price Index number earlier in the week indicate that inflation may be reaccelerating after a period of consolidation. Further, consumer spending which accounts for more than two-thirds of U.S. economic activity shot up 1.8% last month, the largest increase in nearly two years due in part to a surge in wage gains. Robust job growth and the lowest unemployment rate in more than 53 years paints a rosy picture, but this is the calm before the recessionary storm if history is any guide. The Fed clearly has more work to do in slowing down aggregate demand. Nevertheless, as discussed in a prior report, recession is likely to come in the second half of this year.

Note that other than a brief respite back in mid-year 2022, the PCE Price Index has remained in a steady uptrend since May 2020. Fed Chair Powell's profuse use of the word disinflationary during his press conference following the last Fed policy announcement two weeks ago does not seem to be supported by the data, and indeed, Wednesday's release of the latest Fed meeting minutes confirmed that nowhere was the word disinflationary to be found.

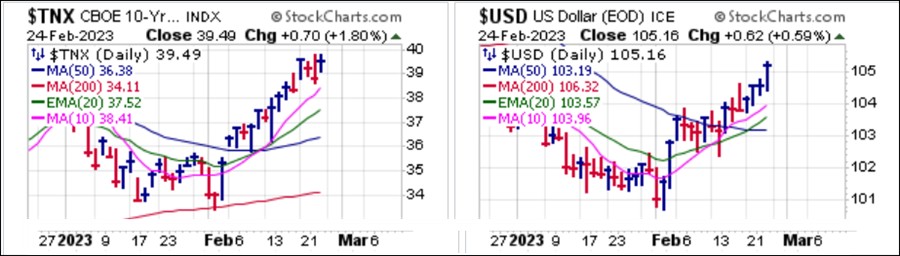

Interest rates and the U.S. Dollar moved higher in response on Friday, as the 10-Year Treasury Yield ($TNX) again approaches the 4.00% level, ending the week at 3.949%. The U.S. Dollar ($USD) closed higher on Friday as it extends its gains off the early February lows. Note that the peak in the market occurred as precisely the same time as the low in the Dollar.

Interest rates and the U.S. Dollar moved higher in response on Friday, as the 10-Year Treasury Yield ($TNX) again approaches the 4.00% level, ending the week at 3.949%. The U.S. Dollar ($USD) closed higher on Friday as it extends its gains off the early February lows. Note that the peak in the market occurred as precisely the same time as the low in the Dollar. As we have noted repeatedly, we do not believe that we are in a new bull market. The trend of inflation is reaccelerating and some are now speculating that the Fed will have to take the Fed Funds Rate above 6%, well beyond the current terminal rate of 5.25-5.50% that the crowd currently expects, and leave it there. In our view, as long as rates and the Dollar continue to rise, stocks will be on the defensive.

As we have noted repeatedly, we do not believe that we are in a new bull market. The trend of inflation is reaccelerating and some are now speculating that the Fed will have to take the Fed Funds Rate above 6%, well beyond the current terminal rate of 5.25-5.50% that the crowd currently expects, and leave it there. In our view, as long as rates and the Dollar continue to rise, stocks will be on the defensive.The Market Direction Model (MDM) remains on a SELL signal.