Israeli attacks on Iran Thursday night threw a spanner into the works of the general market action on Friday. According to Israeli officials, these military operations against Iranian targets will continue for two weeks. If that is true, then the market has just been flipped into a Twilight Zone where it becomes very difficult to take a stand on stocks, one way or the other.

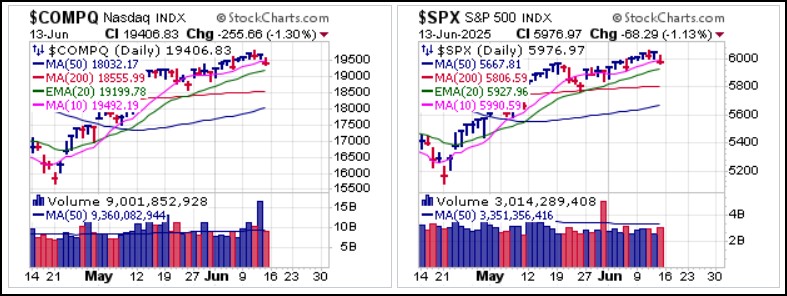

The good news is that at least on Friday, the market's reaction was relatively muted, but could improve or deteriorate based on the news flow coming out of the Middle East. Otherwise, light CPI and PPI data this past week offered a constructive counterpoint to the week's action, but by Friday both the NASDAQ Composite and S&P 500 Indexes were rolling through 10-dma support, perhaps en route to a test of the 20-dema.

Gold ended the week with its highest weekly close in history as the Continuous Futures Contract ended Friday's session at $3432.03 an ounce while COMEX Gold Futures printed a weekly close of $3452.60 an ounce.

Gold ended the week with its highest weekly close in history as the Continuous Futures Contract ended Friday's session at $3432.03 an ounce while COMEX Gold Futures printed a weekly close of $3452.60 an ounce. This played out as a pocket pivot/trendline breakout in the SPDR Gold Trust (GLD). In the process the GLD posted an all-time high closing price as it came within twelve cents of its absolute all-time high at 316.41.

This played out as a pocket pivot/trendline breakout in the SPDR Gold Trust (GLD). In the process the GLD posted an all-time high closing price as it came within twelve cents of its absolute all-time high at 316.41.

Silver spent the week holding tight after big gains the prior week. The Silver Continuous Futures Contract ended the week at $36.30 an ounce after coming to within about 1% of the $37 an ounce level.

Bitcoin ($BTCUSD) came in to test 50-dma support as it tries to make up its mind over whether it is a risk-on asset much like its tech-stock counterparts or a safe-haven, alternative currency asset like its precious metals cousins.

With the Fed on tap for Wednesday and the news flow out of Israel and Iran remaining extremely fluid as the conflict steadily escalates. The situation in the Middle East, however, presents a very serious and substantial Wild Card for the market. If long anything, review trailing stops and be prepared to act as necessary. Otherwise, fasten your seatbelts as we move into the new trading week which is likely to be a volatile one.

The Market Direction Model (MDM) remains on a BUY signal.