Weak economic data on Friday helped drive a sharp rally. The ISM Non-Manufacturing Index came in at 49.6 from a prior 54, implying a contraction in non-manufacturing activity. In addition, November factory orders fell 1.8% vs. expectation of a 0.4% decline. The headline number was of course the Bureau of Labor Statistics monthly jobs report which showed an increase of 223,000 vs. expectations of 210,000. What caught the market's eye most of all was the less-than-expected increase in wages at 0.3% vs. expectations of 0.4%. CME Fed Futures originally was split 50/50 between a 25 and 50 bps hike in February when the Fed next meets. After the wages number, a 25 bps hike is now favored at odds of roughly 75%.

That said, the lack of those seeking work post COVID, the growing number of retirees, and the Fed counting those who work 2 or 3 jobs as the creation of 2 or 3 jobs makes the reported figures look better than they are in reality, and explains how the unemployment rate dropped to 3.5%. With a lack of supply, an inflationary wage spiral is still possible. Demand, however, is also cooling as major companies such as Apple and Amazon lay off workers. Big tech companies are down typically -50% or more since late 2021. Blackrock and Goldman Sachs believe unemployment will not soar due to the lack of supply and demand, but instead tick higher by just 0.5%. This would go against all other prior recessions when unemployment soared.

It seems more likely that as rates continue to rise, something will break forcing the Fed to pivot as companies layoff employees at a faster pace. Companies currently are not even accounting for recession given their lofty earnings projections.

Lower wage inflation sent the indexes sharply higher on Friday, despite the higher number of jobs created than expected along with an unemployment rate that came in under estimates, with the NASDAQ 100 and NASDAQ Composite leading the way to post gains of 2.78% and 2.56%, respectively. Volume was higher on the NASDAQ but lower on the NYSE as the NASDAQ Composite and the S&P 500 run into moving average resistance at their 20-dema, and 50-dma, respectively, while the narrow 30-stock Dow and the much broader NYSE Composite Index push up through their 50-day moving averages.

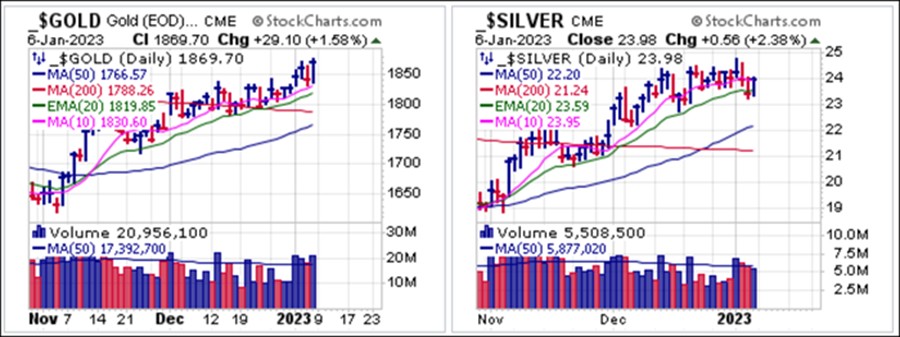

If we have any kind of Focus List it would be represented by the precious metals space. We have been constructive on gold and silver over the past 2-3 months as they have rallied sharply off their September/October lows. Both metals began the New Year with higher highs but it has been gold that has taken a minor relative strength lead over the past week. While silver reversed at higher highs on Tuesday, the first trading day of the year, gold has proceeded to post higher highs with futures closing the week at $1869.70/oz. while silver rebounded off its 20-dma on Friday to close the first week of the trading year at 23.98.

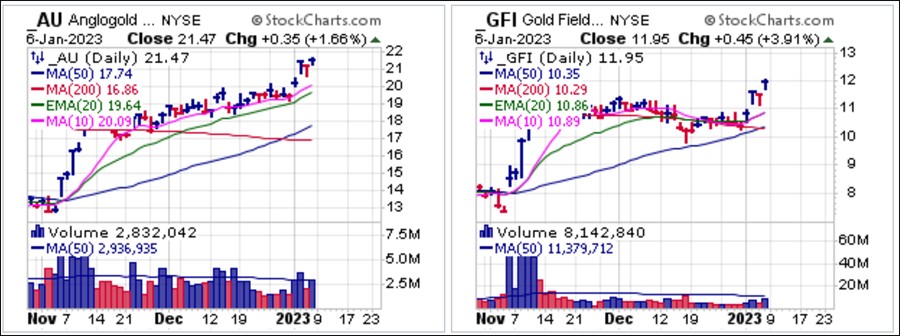

If we have any kind of Focus List it would be represented by the precious metals space. We have been constructive on gold and silver over the past 2-3 months as they have rallied sharply off their September/October lows. Both metals began the New Year with higher highs but it has been gold that has taken a minor relative strength lead over the past week. While silver reversed at higher highs on Tuesday, the first trading day of the year, gold has proceeded to post higher highs with futures closing the week at $1869.70/oz. while silver rebounded off its 20-dma on Friday to close the first week of the trading year at 23.98. We have previously discussed gold miners AngloGold-Ashanti (AU) and Gold Fields (GFI) as two of the leading names in the space. They broke out of bases this week on moves that started on Tuesday, long before Friday's jobs number, ISM, and Factory Orders data came out. What did they all know and when did they know it?

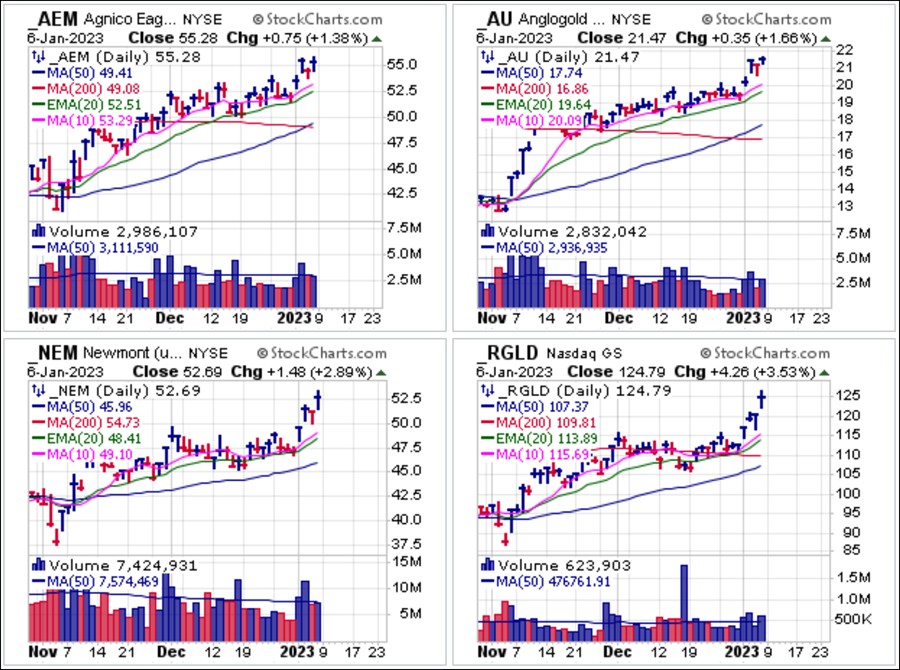

We have previously discussed gold miners AngloGold-Ashanti (AU) and Gold Fields (GFI) as two of the leading names in the space. They broke out of bases this week on moves that started on Tuesday, long before Friday's jobs number, ISM, and Factory Orders data came out. What did they all know and when did they know it? In fact, we also reported on several gold miners that posted pocket pivots on Tuesday, Agnico-Eagle Mines (AEM), AngloGold-Ashanti (AU), Newmont Corp. (NEM), and Royal Gold (RGLD).

In fact, we also reported on several gold miners that posted pocket pivots on Tuesday, Agnico-Eagle Mines (AEM), AngloGold-Ashanti (AU), Newmont Corp. (NEM), and Royal Gold (RGLD).

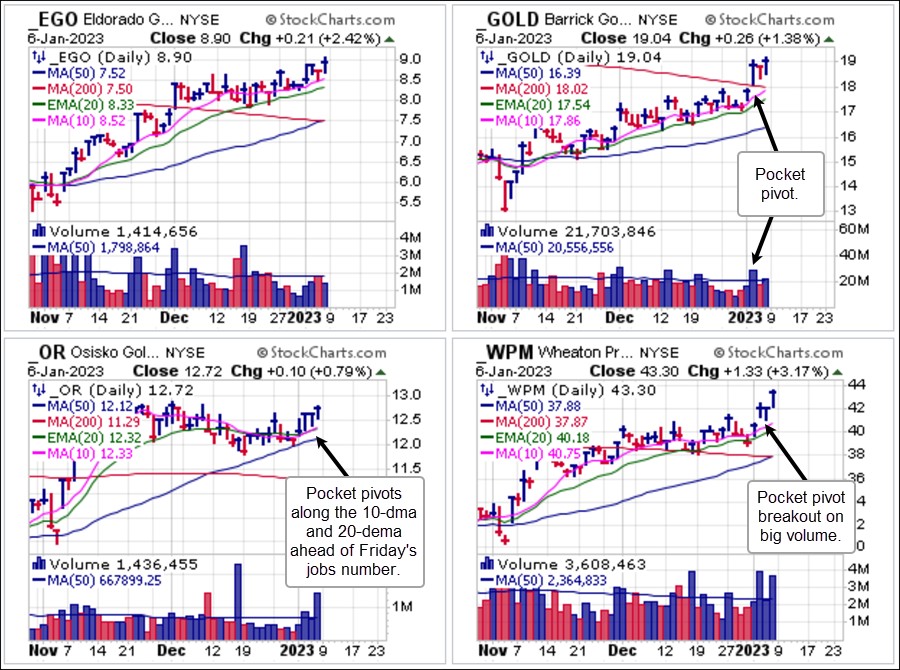

The strength in gold miners is broad, and with institutional favorites like those shown above moving briskly higher appear to indicate a more concerted move by institutions into the space. Here we note a pocket pivot through the 200-dma in Barrick Gold (GOLD) on Wednesday, three pocket pivots along the 10-dma and 20-dema by Osisko Gold Royalties (OR) on the first three trading days of the New Year, and a gap-up pocket pivot breakout in Wheaton Precious Metals (WPM) on Wednesday. OR and WPM are both owners of gold productions streams and do not mine the stuff themselves. Note that all of this strong action among golds occurred well before Friday's economic data brought a Fed pivot rally into force in the rest of the market. What did these stocks know, and when did they know it? That is a fair question to ask, and an intriguing one.

Friday's rally was certainly a robust and broad one as most stocks rallied from deeply oversold positions. Not so with the precious metals space, which was setting up and moving early in the week. The question now is that while Friday's rally on hopes of a Fed pivot was triggered by the data on that day, the market still has more data hurdles to clear. The most important of these will be this Thursday's Consumer Price Index where core CPI is expected to come in at 0.3% to 0.4% vs. last month's 0.1%. If the data comes in as expected then it would imply that the inflation genie remains out of the bottle, and any Fed pivot rally might be short-lived as a result. Shelter which makes up 40% of the CPI can remain stubbornly high though the Fed has said they are aware of this thus are likely to put more weight on other shelter metrics which are less lagging such as the rate for new leases which is coming down.

Friday's rally was certainly a robust and broad one as most stocks rallied from deeply oversold positions. Not so with the precious metals space, which was setting up and moving early in the week. The question now is that while Friday's rally on hopes of a Fed pivot was triggered by the data on that day, the market still has more data hurdles to clear. The most important of these will be this Thursday's Consumer Price Index where core CPI is expected to come in at 0.3% to 0.4% vs. last month's 0.1%. If the data comes in as expected then it would imply that the inflation genie remains out of the bottle, and any Fed pivot rally might be short-lived as a result. Shelter which makes up 40% of the CPI can remain stubbornly high though the Fed has said they are aware of this thus are likely to put more weight on other shelter metrics which are less lagging such as the rate for new leases which is coming down. The Market Direction Model (MDM) remains on a SELL signal.