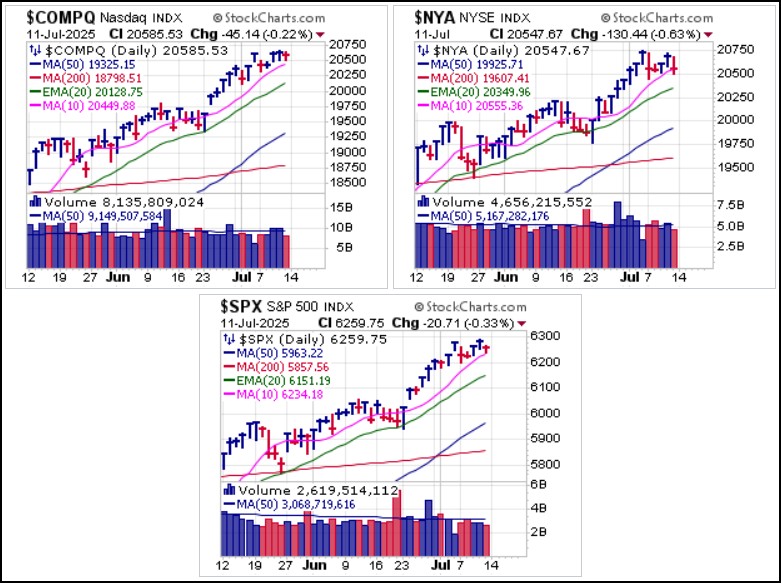

Major market indexes endured a week of tariff surprises as Trump sent tariff notification letters to various U.S. trading partners. Some of the whoppers: a 50% tariff on copper, a 50% punitive tariff on Brazil, 25% tariffs on Canada and Mexico, and 20% tariffs on the EU. In spite of all that the NASDAQ Composite and S&P 500 remained above 10-dma support, mostly due to big-stock techs holding steady. Other areas of the market as better represented by the NYSE Composite Index as it closes below 10-dma support. And while the indexes appear relatively calm on the surface, Friday’s breadth was decidedly negative, with 782 up vs. 1918 down on the NYSE 1238 up vs. 3260 down on the NASDAQ.

On Saturday morning the President came out swinging with the announcement of 30% tariffs on Mexico and the EU unless a trade deal is made by the new August 1st deadline. This may put additional pressure on the markets, but so far the indexes have refused to crack in any meaningful way.

Silver was one of the big stories of the week as it powerfully broke out to a new 13-year high on Friday when COMEX Silver Futures printed an intraday peak of $39.225 an ounce. The iShares Silver Trust (SLV) shows a pocket pivot on Thursday followed by a BGU breakout on Friday. We last discussed an entry in the SLV at the 20-dema two weeks ago in this report, on June 29th, obviously an earlier and more propitious entry. Anyone long silver on that basis ahead of the Thursday and Friday move enjoyed a pleasant ride into the end of the week.

Silver was one of the big stories of the week as it powerfully broke out to a new 13-year high on Friday when COMEX Silver Futures printed an intraday peak of $39.225 an ounce. The iShares Silver Trust (SLV) shows a pocket pivot on Thursday followed by a BGU breakout on Friday. We last discussed an entry in the SLV at the 20-dema two weeks ago in this report, on June 29th, obviously an earlier and more propitious entry. Anyone long silver on that basis ahead of the Thursday and Friday move enjoyed a pleasant ride into the end of the week. Gold remains within 4-5% of its all-time highs as it continues to base-build. It is now twelve weeks into a new base it has formed since going parabolic into mid-April. While many wanted to call that a climax top, it is important to remember that gold is not a stock, and buying over the past two years has come from global central banks. They are likely not buying for a trade, as gold is now the #2 reserve asset in the world, behind the U.S. Dollar and ahead of the Euro. As this base potentially continues to tighten up, it could set up a move to higher prices at some point.

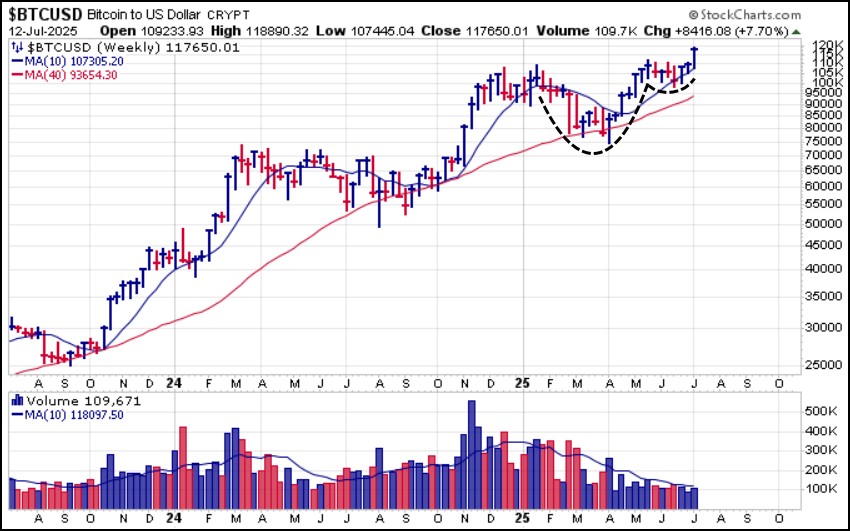

Gold remains within 4-5% of its all-time highs as it continues to base-build. It is now twelve weeks into a new base it has formed since going parabolic into mid-April. While many wanted to call that a climax top, it is important to remember that gold is not a stock, and buying over the past two years has come from global central banks. They are likely not buying for a trade, as gold is now the #2 reserve asset in the world, behind the U.S. Dollar and ahead of the Euro. As this base potentially continues to tighten up, it could set up a move to higher prices at some point. Two weeks ago, in this report, we also discussed the tightening action in Bitcoin ($BTCUSD) as it was working on the handle area of a 23-week cup-with-handle formation. This past week King Crypto made good on that tight action by breaking out to all-time highs.

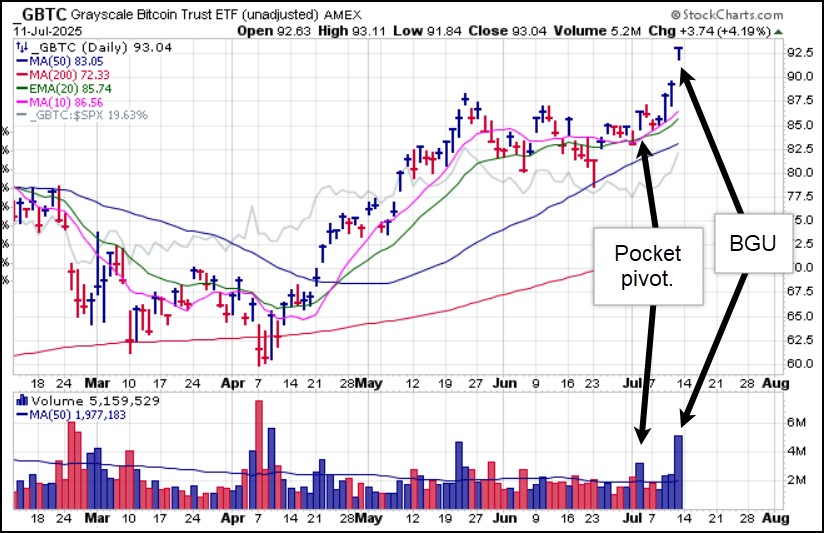

Two weeks ago, in this report, we also discussed the tightening action in Bitcoin ($BTCUSD) as it was working on the handle area of a 23-week cup-with-handle formation. This past week King Crypto made good on that tight action by breaking out to all-time highs. While weekly volume on the $BTCUSD chart was light, we saw much heavier volume in the Grayscale Bitcoin Trust (GBTC) ETF as it broke out Thursday on above-average volume. Friday saw GBTC gap higher on huge volume in a technical buyable gap-up set-up, but may be less significant since $BTCUSD trades 24/7 and thus cannot by definition have gap-up moves.

While weekly volume on the $BTCUSD chart was light, we saw much heavier volume in the Grayscale Bitcoin Trust (GBTC) ETF as it broke out Thursday on above-average volume. Friday saw GBTC gap higher on huge volume in a technical buyable gap-up set-up, but may be less significant since $BTCUSD trades 24/7 and thus cannot by definition have gap-up moves.No worries. On July 2nd, we issued a Pocket Pivot Report on GBTC as it popped off the 10-dma and 20-dema and then pulled back into the 10-dma over the next two days, putting it in a prime entry position based on the prior pocket pivot. That preceded the breakout and eliminated any need to chase Friday's strength. Interestingly, the breakout at the end of the week in $BTCUSD/GBTC looks very similar to the action in silver and the SLV at the same time. So, as Bitcoin is the new silver, silver is likewise the new Bitcoin.

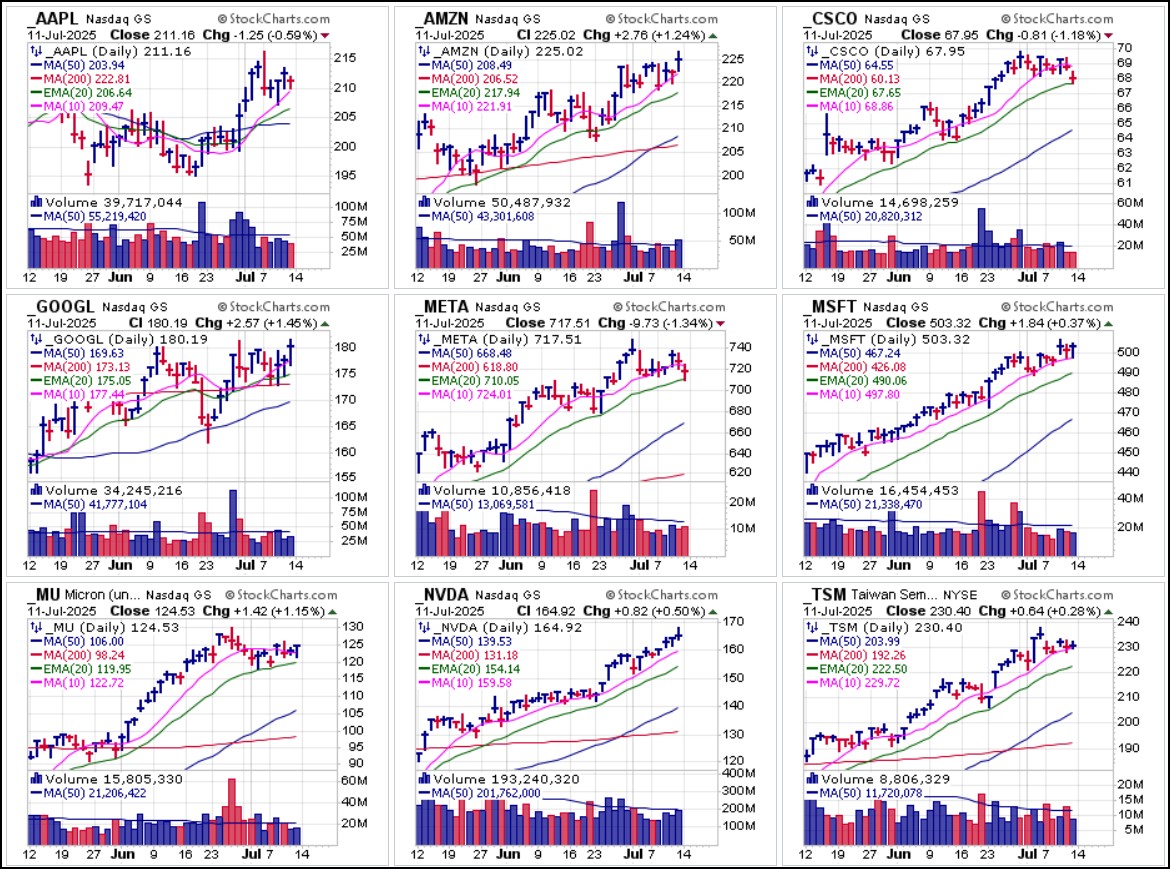

Stocks, meanwhile, remain a mixed bag. While big-stock NASDAQ techs and most semiconductors hold up relatively well, big-stock clouds Salesforce.com (CRM), ServiceNow (NOW), and Workday (WDAY), along with many of their smaller cousins had a rough week.

Stocks, meanwhile, remain a mixed bag. While big-stock NASDAQ techs and most semiconductors hold up relatively well, big-stock clouds Salesforce.com (CRM), ServiceNow (NOW), and Workday (WDAY), along with many of their smaller cousins had a rough week. And as other big-stock techs hang in there, the market sees the arrival of earnings season which may offer the proverbial proof in the pudding for this rally off the early April lows that has taken the NASDAQ and S&P 500 indexes back to all-time highs. Earnings may be the last obstacle left in the market's path as it has rallied impetuously since early April, laughing in the face of Trump's tariffs, war in the Mid-East that included the first-ever bombing of Iranian soil by the U.S., continuing and expanding war in Ukraine, riots over mass deportation policy, ever-deepening U.S. national debt, etc. Thus, earnings season may be pivotal in determining the market's direction as we move through summer 2025.

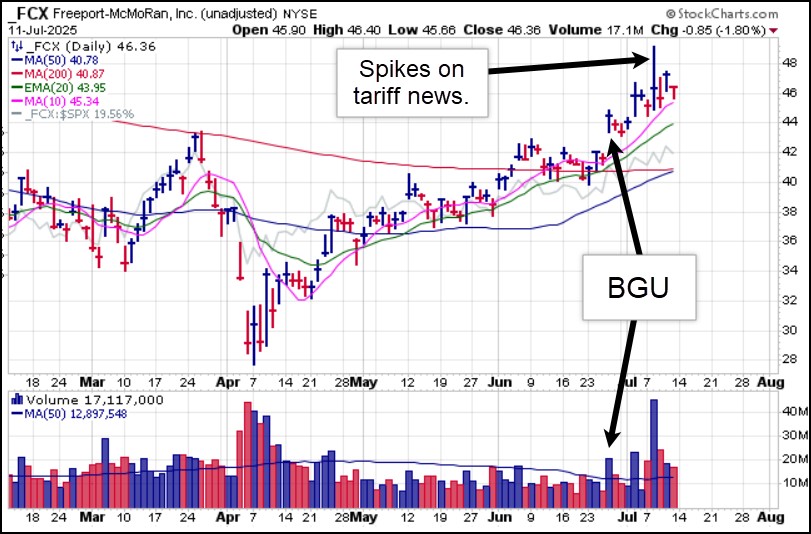

And as other big-stock techs hang in there, the market sees the arrival of earnings season which may offer the proverbial proof in the pudding for this rally off the early April lows that has taken the NASDAQ and S&P 500 indexes back to all-time highs. Earnings may be the last obstacle left in the market's path as it has rallied impetuously since early April, laughing in the face of Trump's tariffs, war in the Mid-East that included the first-ever bombing of Iranian soil by the U.S., continuing and expanding war in Ukraine, riots over mass deportation policy, ever-deepening U.S. national debt, etc. Thus, earnings season may be pivotal in determining the market's direction as we move through summer 2025. On June 26th we issued a Buyable Gap-Up Report for big-stock copper miner Freeport-McMoRan (FCX). The has since continued higher and on Tuesday spiked higher after Trump threatened 50% tariffs on copper. FCX is a U.S. copper producers, and was immediately seen as a beneficiary of those tariffs. That move was sold into, however, and FCX has since backed down into its 10-dma where it may present a secondary entry using the 10-day as a selling guide.

On June 26th we issued a Buyable Gap-Up Report for big-stock copper miner Freeport-McMoRan (FCX). The has since continued higher and on Tuesday spiked higher after Trump threatened 50% tariffs on copper. FCX is a U.S. copper producers, and was immediately seen as a beneficiary of those tariffs. That move was sold into, however, and FCX has since backed down into its 10-dma where it may present a secondary entry using the 10-day as a selling guide.We tend to think that the imposition of 50% tariffs for the alleged purpose of "bringing copper production back to the U.S." to be something of a pipe dream. Even if it motivates mining concerns to build smelters and refineries in the U.S., it will take years to do so, subjecting U.S. industries that use copper to higher input prices for years. It is possible that the market figured this out as sellers hit the news spike on Tuesday. This will be an interesting soap opera, along with the rest of the newly announced tariffs, that will continue to play out ahead of the alleged, "final" August 1st deadline. This in turn could produce opportunities in a number of areas, particularly industrial metals.

The Market Direction Model (MDM) remains on a BUY signal.

The Market Direction Model (MDM) remains on a BUY signal.