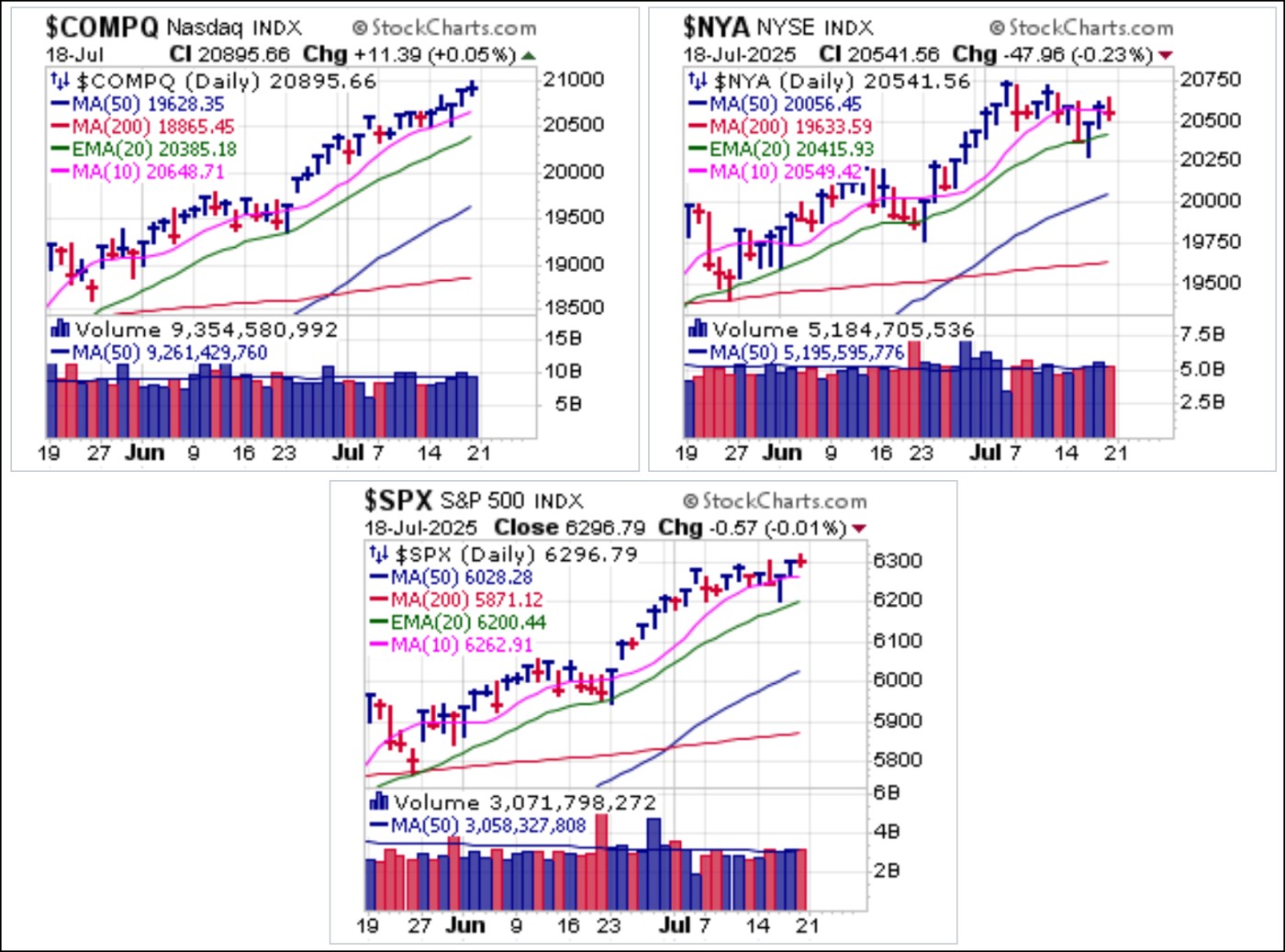

Major market indexes continued to post higher highs on the back of soft CPI and PPI data on Tuesday and Wednesday. Against this backdrop of benign inflation data were voices emanating from the Trump Administration calling for the resignation and/or prosecution of Fed Chairman Jerome Powell for cause. The NASDAQ Composite and S&P 500 both posted new all-time highs on Friday morning before rolling back off the early morning peak. The NASDAQ ended the day at another all-time high as the NYSE Composite and S&P both closed slightly negative on higher OpEx volume.

This appears to be something of a sell the news situation after a steady flow of favorable news regarding crypto-related legislation. First, the GENIUS Act (308-122 vote): establishes a regulatory framework for stablecoins, requiring issuers to back tokens with liquid assets like U.S. dollars and disclose reserves monthly. This bill, already passed by the Senate, was signed into law by President Trump on Friday, July 18th. In addition, two other pieces of crypto-legislation are making positive progress through the Congressional approval process:

This appears to be something of a sell the news situation after a steady flow of favorable news regarding crypto-related legislation. First, the GENIUS Act (308-122 vote): establishes a regulatory framework for stablecoins, requiring issuers to back tokens with liquid assets like U.S. dollars and disclose reserves monthly. This bill, already passed by the Senate, was signed into law by President Trump on Friday, July 18th. In addition, two other pieces of crypto-legislation are making positive progress through the Congressional approval process:- The Digital Asset Clarity Act passed by the House (294-134 vote) defines when cryptocurrencies are securities (regulated by the SEC) or commodities (regulated by the CFTC), aiming to clarify regulatory jurisdiction. This bill has been sent to the Senate for further consideration.

- The Anti-CBDC Surveillance State Act, also passed by the House (219-210 vote) prohibits the Federal Reserve from issuing a central bank digital currency, citing privacy concerns. This bill also awaits Senate approval.

Regardless of the tepid reaction from $BTCUSD this past week in the wake of this news, last week's breakout held up as buyers and sellers met en masse to keep King Crypto essentially unchanged for the week, thus the action can be seen as a technical Transfer of Ownership as weak hands sell to new, potentially stronger hands. We see the recent decoupling from stocks as positive for $BTCUSD as it starts to act more like an alternative-currency in the face of a U.S. National Debt that only a week or so ago crossed the $37 trillion level, now at $37.1 trillion.

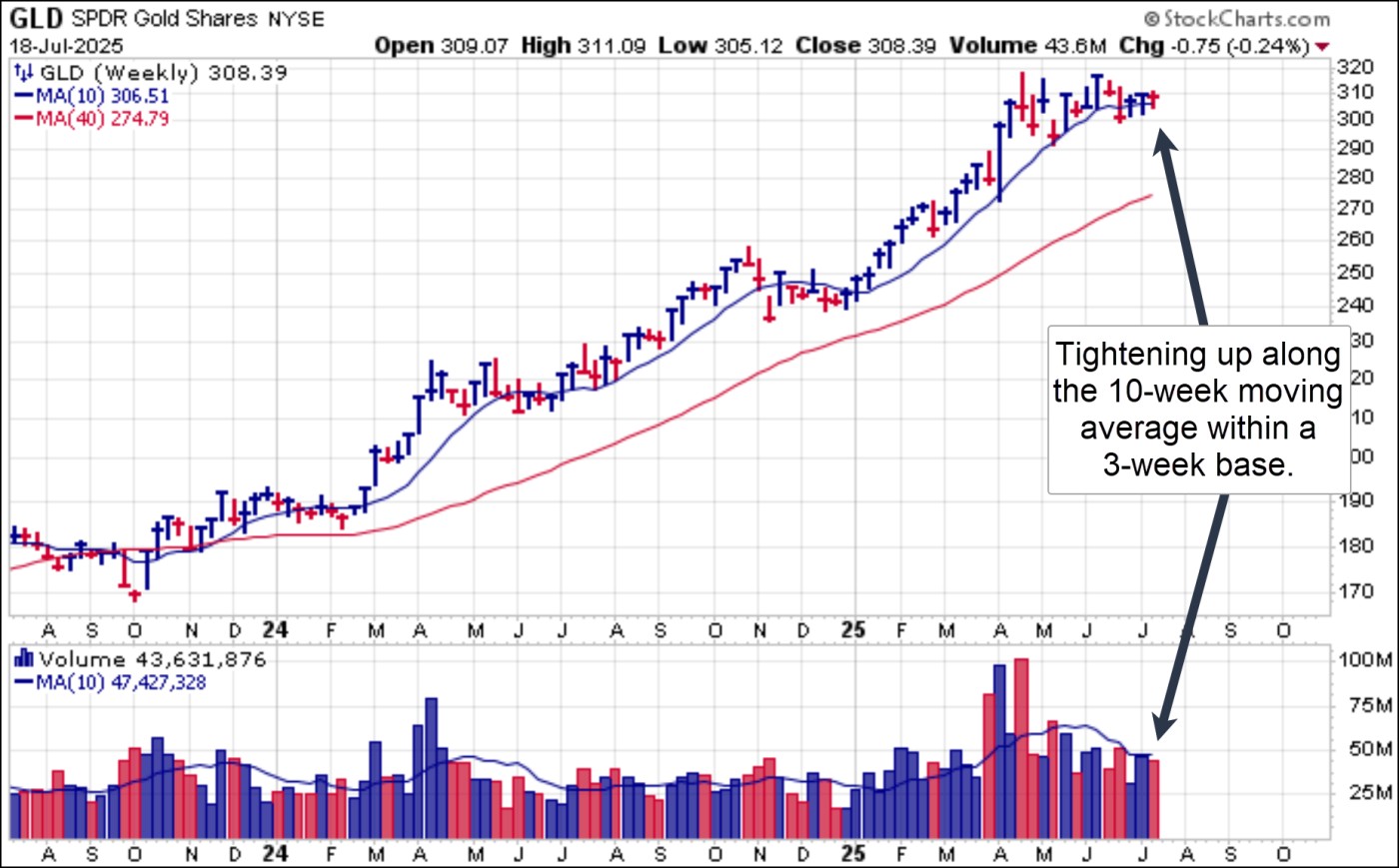

In the same alternative-currency space, gold via the SPDR Gold Trust (GLD) continues to track tight sideways on the weekly chart. After working on a a flat base for the past thirteen weeks, the GLD has tightened up considerably along 10-week moving average support, setting up a possible breakout. On Wednesday, the GLD posted a strong pocket pivot move at the 50-dma, which remains in force as a long entry using the 50-day line as a tight selling guide.

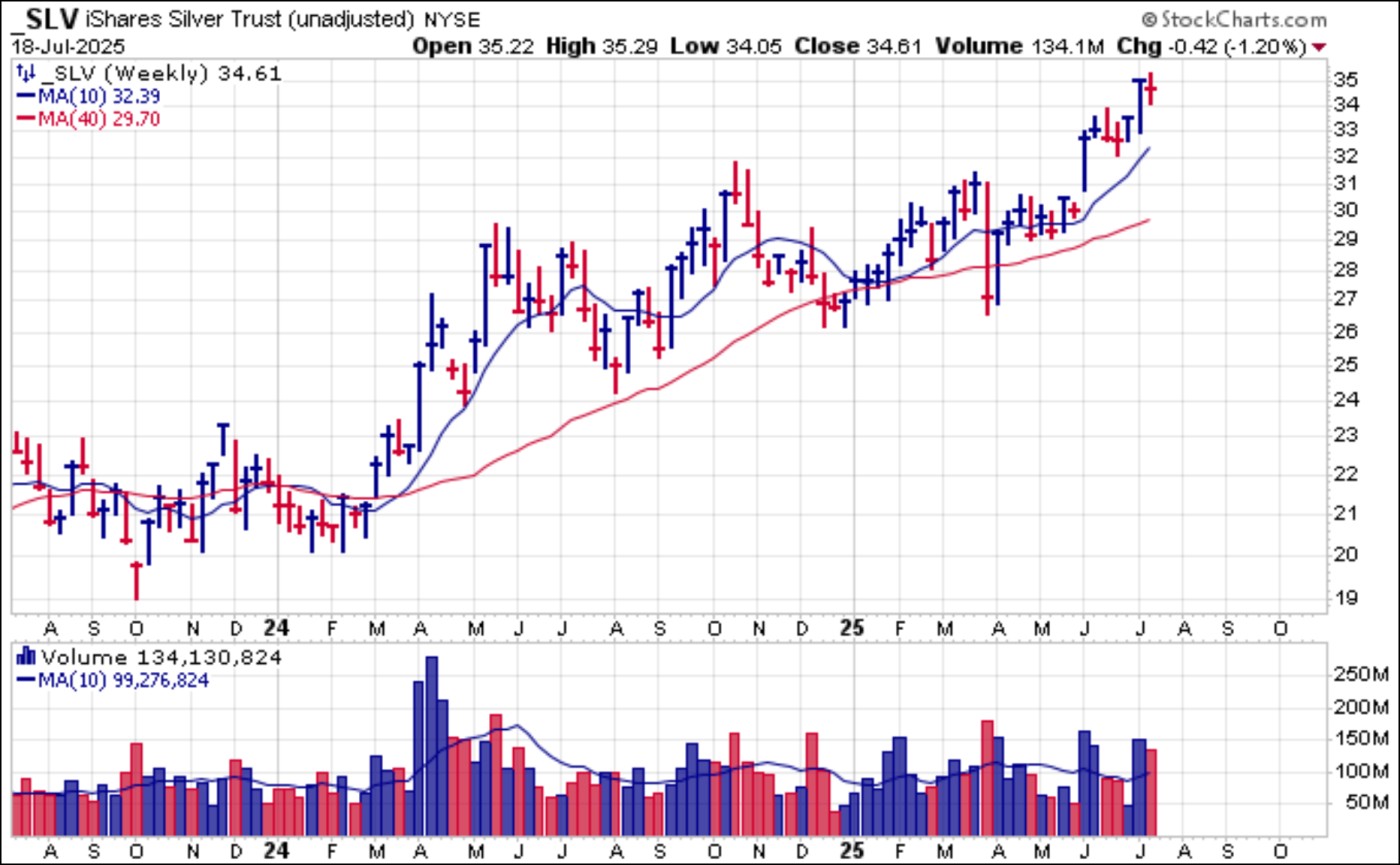

Silver via the iShares Silver Trust (SLV) is holding up relatively well near last week's 13-year highs following a short flag breakout. For now, the uptrend in silver remains in force.

Silver via the iShares Silver Trust (SLV) is holding up relatively well near last week's 13-year highs following a short flag breakout. For now, the uptrend in silver remains in force. Earnings will likely be the litmus test for this rally as we move into the end of July and early August, the thickest part of the earnings season jungle. Netflix (NFLX) illustrates this as it succumbed to selling on Thursday after reporting earnings Thursday after the close. Despite beating earnings estimates and raising guidance, the stock was punished on a Shortable Gap-Down (SGD) move through the 10-dma and 20-dema.

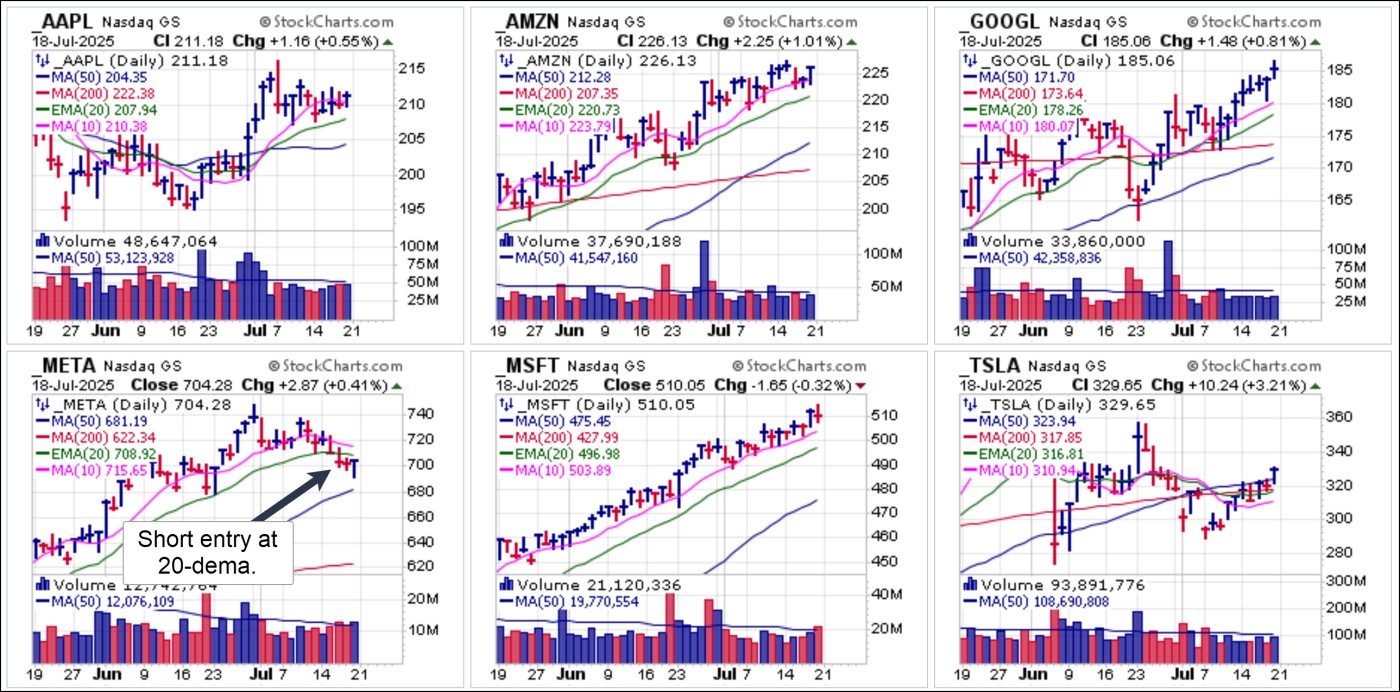

Earnings will likely be the litmus test for this rally as we move into the end of July and early August, the thickest part of the earnings season jungle. Netflix (NFLX) illustrates this as it succumbed to selling on Thursday after reporting earnings Thursday after the close. Despite beating earnings estimates and raising guidance, the stock was punished on a Shortable Gap-Down (SGD) move through the 10-dma and 20-dema. This coming week we will see earnings from big-stock NASDAQ names Alphabet (GOOGL) and Tesla (TSLA), both on Wednesday, July 23, after the close. Amazon (AMZN), Apple (AAPL), Meta Platforms (META), and Microsoft (MSFT) will report the following week. MSFT is expected to report earnings on Tuesday, July 29, META on Wednesday, July 30, and AMZN and AAPL on Thursday July 31st. Most of these names continue to act well, and we suspect that earnings will likely affect how these charts resolve. META is one exception as it triggered a short entry at the 20-dema on Wednesday. We would not recommend taking initial positions in any of these just ahead of earnings unless one has a reasonable profit cushion from a prior entry lower in the pattern.

This coming week we will see earnings from big-stock NASDAQ names Alphabet (GOOGL) and Tesla (TSLA), both on Wednesday, July 23, after the close. Amazon (AMZN), Apple (AAPL), Meta Platforms (META), and Microsoft (MSFT) will report the following week. MSFT is expected to report earnings on Tuesday, July 29, META on Wednesday, July 30, and AMZN and AAPL on Thursday July 31st. Most of these names continue to act well, and we suspect that earnings will likely affect how these charts resolve. META is one exception as it triggered a short entry at the 20-dema on Wednesday. We would not recommend taking initial positions in any of these just ahead of earnings unless one has a reasonable profit cushion from a prior entry lower in the pattern. One of the best-performing emerging sectors lately has been the Quantum Computing space. On July 3rd we reported on a pocket pivot in D-Wave Quantum (QBTS) as it regained the 10-dma and 20-dema. On Thursday of this week it posted a big-volume pocket pivot breakout and held up well on Friday. On June 30th we reported on pocket pivots in IonQ (IONQ) and Rigetti Computing (RGTI) as they came up off their late June lows. IONQ has pushed back towards the highs of its current base after posting a pocket pivot at the 10-dma on Friday. RGTI posted a massive-volume gap-up move on Wednesday after announcing that it had achieved a mid-year performance milestone with its new 36-qubit quantum computer system, demonstrating a 99.5% median two-qubit gate fidelity. This represents a 2x reduction in error rate compared to its previous 84-qubit Ankaa-3 system. It ended the week at higher highs.

One of the best-performing emerging sectors lately has been the Quantum Computing space. On July 3rd we reported on a pocket pivot in D-Wave Quantum (QBTS) as it regained the 10-dma and 20-dema. On Thursday of this week it posted a big-volume pocket pivot breakout and held up well on Friday. On June 30th we reported on pocket pivots in IonQ (IONQ) and Rigetti Computing (RGTI) as they came up off their late June lows. IONQ has pushed back towards the highs of its current base after posting a pocket pivot at the 10-dma on Friday. RGTI posted a massive-volume gap-up move on Wednesday after announcing that it had achieved a mid-year performance milestone with its new 36-qubit quantum computer system, demonstrating a 99.5% median two-qubit gate fidelity. This represents a 2x reduction in error rate compared to its previous 84-qubit Ankaa-3 system. It ended the week at higher highs. On the weekly chart, RGTI finished up the week with a strong-volume trendline breakout from a cup-with-handle formation. Any pullbacks closer to the breakout point would bring it back into buying range so can be watched for.

On the weekly chart, RGTI finished up the week with a strong-volume trendline breakout from a cup-with-handle formation. Any pullbacks closer to the breakout point would bring it back into buying range so can be watched for.

Ambarella (AMBA), which designs AI semiconductors used in drones, posted what can be interpreted as a pocket pivot on Thursday. This is because Monday's action constituted a supporting pocket pivot at the 20-dema so that we would count the volume on that day as an up-volume day in the pocket pivot volume count. Friday's small pullback brings the stock back into buying range.

The market has mostly become a market of stocks as individual sectors like quantum computing, drones, small modular nuclear reactor makers, and space names, arguably more speculative areas of the market, acted well this past week. Is the speculative fever in these hot areas of the market a cautionary contrarian sign? Earning season, as the litmus test for individual leading stocks off the April lows, will likely decide the issue. Markets are expecting stocks to rise on an easy earnings beat, given that second-quarter year-over-year earnings growth was cut from 8.5% at the start of the year to 3.7% due to the tariffs issue.

The Market Direction Model (MDM) remains on a BUY signal.