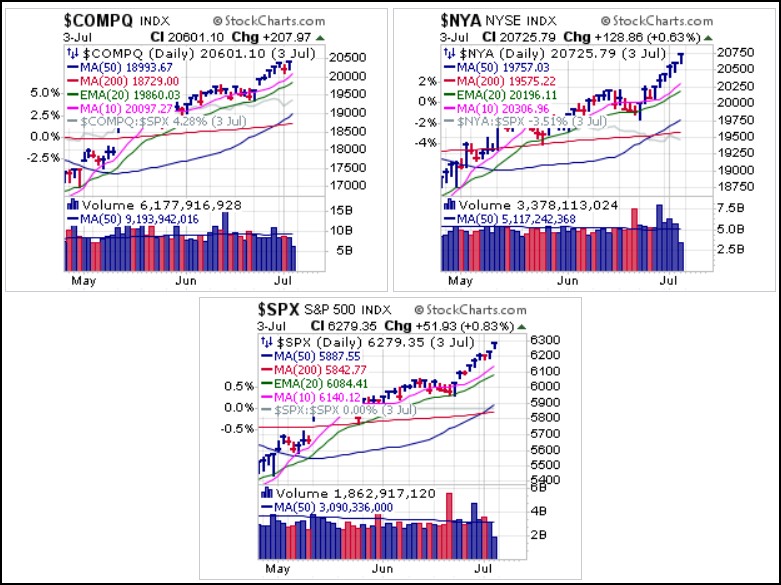

Thursday's Bureau of Labor Statistics’ jobs report helped prod the market higher as the NASDAQ Composite, NYSE Composite, and S&P 500 all added to their string of new highs. June total nonfarm payroll employment increased by 147,000 jobs vs. expectations of 110,000, while non-farm private payrolls rose by 74,000 vs. expectations of 102,000 to 123,000 and the unemployment rate fell to 4.1% vs. expectations of 4.3%. The data was seen as putting the Fed on hold or at least to remain on track for two more rate cuts in 2025.

Currently, however, the Fed Dot Plot shows eight members who project two more cuts, seven who project zero rates cuts, two who project one more rate cut, and two who forecast three more rate cuts. Thus, the Fed's views on a member-by-member basis appears to reflect a certain amount of uncertainty.Meanwhile, major market indexes do not reflect any uncertainty as the keep pushing to new highs. The strong action in the NYSE Composite also speaks to a broadening number of stocks participating in the rally. This is either an indication of constructive breadth or that the dogs are finally starting to bark. Stay tuned.

Late on Thursday, the House passed Trump’s One Big Beautiful Bill Act (OBBBA). And while this was hailed as a great thing for the country, what was less advertised was that the fact that it also raised the debt ceiling by $5 trillion. That is the largest debt ceiling increase ever passed by Congress in a single vote. Thus, OBBBA may more appropriately stand for One Big Bubble Blowing Act as well.

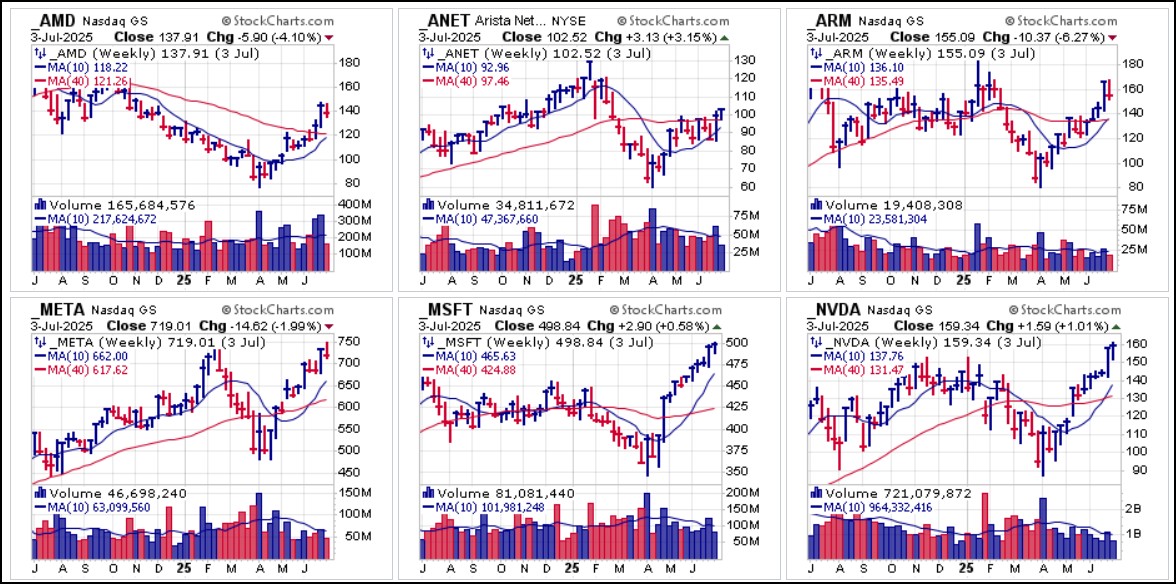

Also late on Thursday, President Trump raised the specter of more trade tensions, warning U.S. trade partners he may start setting levies of as much as 70% unilaterally as soon as Monday ahead of a July 9 deadline for negotiations. That sent stock futures lower overnight and into the Friday morning session. We will see how this all plays out when the new trading week begins.Most of the tech names that we have reported on since the April market lows have continued to trend higher, some at a faster pace than others, and are currently extended. Finding fresh set-ups in this market is a difficult proposition given the extent of the rallies off the April lows, but we continue to be on the lookout for new opportunities as they emerge in real-time.

So far, Bitcoin ($BTCUSD) has reacted in muted fashion to all the news flow on Thursday, as it pulls back from its second breakout attempt since posting all-time highs in the latter half of May.

So far, Bitcoin ($BTCUSD) has reacted in muted fashion to all the news flow on Thursday, as it pulls back from its second breakout attempt since posting all-time highs in the latter half of May.

On Wednesday we reported on the Grayscale Bitcoin Trust (GBTC) when it posted a strong-volume pocket pivot on a gap-up move off the 10-dma and 20-dema. On Thursday it held tight but for now one can watch for pullbacks to the 10-dma/20-dema as potentially lower-risk entry opportunities. The 50-dma for now remains critical moving average support.

Gold and silver also held steady as the SPDR Gold Trust (GLD) and the iShares Silver Trust (SLV) both form constructive bases. On the weekly charts, the GLD is now in an 11-week base as it consolidates near its all-time highs while the SLV hangs tight within a three-week flag formation.

On Thursday we reported on D-Wave Quantum (QBTS) after it posted a pocket pivot on Wednesday. The stock was immediately extended that day but like other quantum computing names we have reported on, QBTS should be monitored as the space continues to evolve and develop. QBTS on July completed a $400 million at-the-market (ATM) equity offering as part of a previously disclosed $400 million shelf registration. So far the stock appears to be absorbing the new supply quite well, so can be watched for pullbacks to the 20-dema as potential lower-risk entry opportunities.

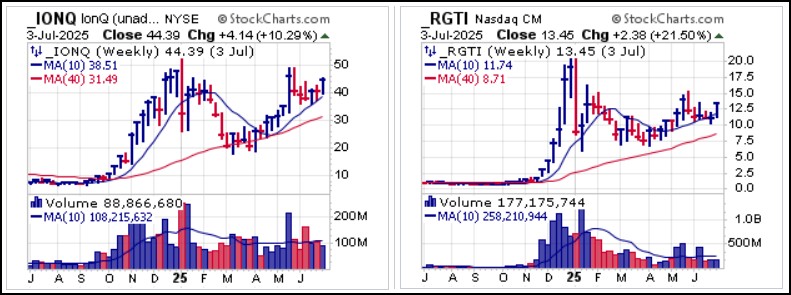

Two other quantum computing names we have reported on previously, IonQ (IONQ) and Rigetti Computing (RGTI) have been buyable along 20-dema support. We first reported on IONQ in mid-May before it launched back towards the $50 highs following a Barron's interview with their CEO who stated that he wanted to make his company "the Nvidia (NVDA) of quantum computing." We have reported on RGTI more recently as it hangs along 10-week moving average support. Both stocks continue to work on potential cup-with-handle formations which we view as constructive.

Two other quantum computing names we have reported on previously, IonQ (IONQ) and Rigetti Computing (RGTI) have been buyable along 20-dema support. We first reported on IONQ in mid-May before it launched back towards the $50 highs following a Barron's interview with their CEO who stated that he wanted to make his company "the Nvidia (NVDA) of quantum computing." We have reported on RGTI more recently as it hangs along 10-week moving average support. Both stocks continue to work on potential cup-with-handle formations which we view as constructive. The Market Direction Model (MDM) remains on a BUY signal.

The Market Direction Model (MDM) remains on a BUY signal.