The NASDAQ Composite, NASDAQ 100, and S&P 500 Indexes all forged new highs on Friday following the Bureau of Labor Statistics' monthly jobs report. June Nonfarm Payrolls beat estimates at 206,000 vs. 185,000, while Nonfarm Private Payrolls came in light at 136,000 vs. estimates of 169.000. 70,000 jobs came from the government sector while another 82,500 jobs came from the health care and social assistance sector.

Also, it is perhaps meaningful to note that the prior months' Nonfarm Payrolls number was revised downward, to 218,000 from 272,000. This has been a noticeable pattern with government economic data for about the last year as various economic reports get revised downward, although this is mostly ignored by the media.

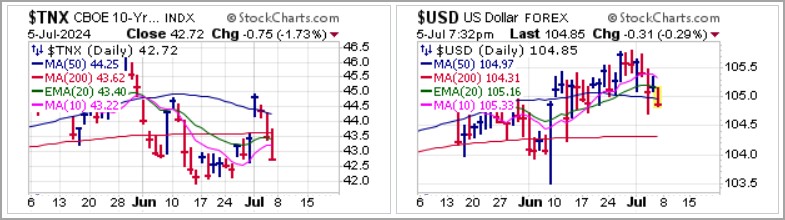

Interest rates via the 10-Year Treasury Yield ($TNX) and the U.S. Dollar($USD) both moved lower after the jobs report.

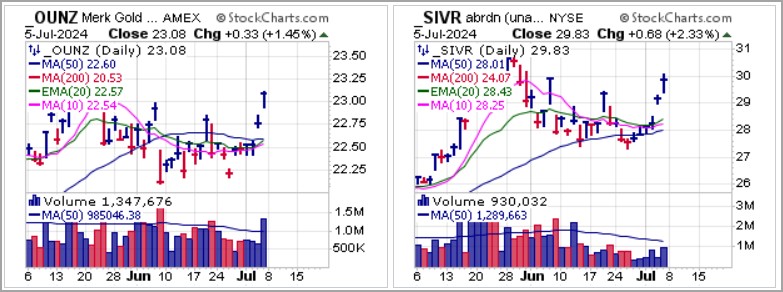

Precious metals moved higher The VanEck Merk Gold Trust (OUNZ) and the Aberdeen Physical Silver Shares (SIVR) both gapped higher on Friday and are extended as they approach their prior May highs corresponding to $2454 an ounce for gold and $32.75 an ounce for silver.

Bitcoin ($BTCUSD) was trashed as it busted 200-dma support on Thursday. That breach of the 200-dma coincided with news that collapsed crypto exchange Mt. Gox officially began repaying its debts yesterday (on one of the most illiquid days of the year, of course) in Bitcoin and Bitcoin Cash ($BCHUSD). The German government has also been selling seized Bitcoin contributing to the selling pressure of Bitcoin but still holds more than 40K BTC, worth over $2.3 billion. It had been feared that those Mt. Gox users who have been repaid will want to sell, putting downward pressure on $BTCUSD. If that is true, and the conversion runs its course, and Germany finishes selling the last of its 40K BTC, $BTCUSD could then rally. But global liquidity must also participate. So far in 2024, it has been on an overall downtrend. Nevertheless, stealth QE continues onwards and upwards as nearly $2 trillion from the US Fed alone has been pledged for 2024 in addition to QE raised for major Japanese banks to prevent them from selling US Treasuries. This will help create a floor for Bitcoin after the Mt. Gox and German selling has subsided.

On Friday, $BTCUSD reached an intraday low of $53,538.09, undercutting its $56,516.09 low of May 1st. It ended the regular session on Friday at $56435.64, just below the May 1st low. If it can decisively regain that low it would potentially trigger a price U&R long entry, after which we would likely want to see it quickly regain the 200-dma as well to trigger a moving average U&R. As of Sunday morning, $BTCUSD is trading at $56,817.40, just above the $56,519.09 May 1st low, but is now reversing at 200-dma resistance, so the situation remains unclear as of the time of this writing.

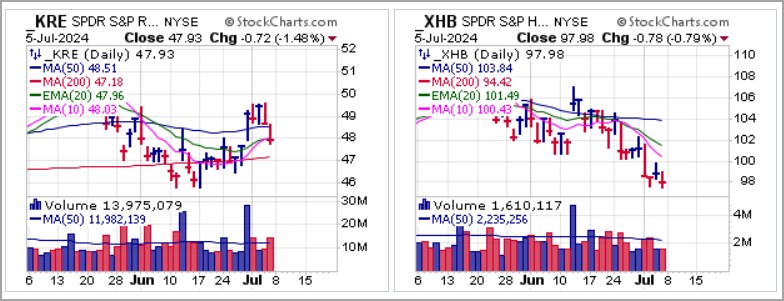

With interest rates moving lower on Friday, it would be expected that Regional Banks and also Homebuilders would respond positively. In an odd cross current, both sectors traded lower as the charts of the SPDR Regional Banking ETF (KRE) and SPDR S&P Homebuilders ETF (XHB) show. KRE has reversed back below its 50-dma while the XHB remains in a downtrend as it gets ever more extended from the underbelly of its own 50-dma.

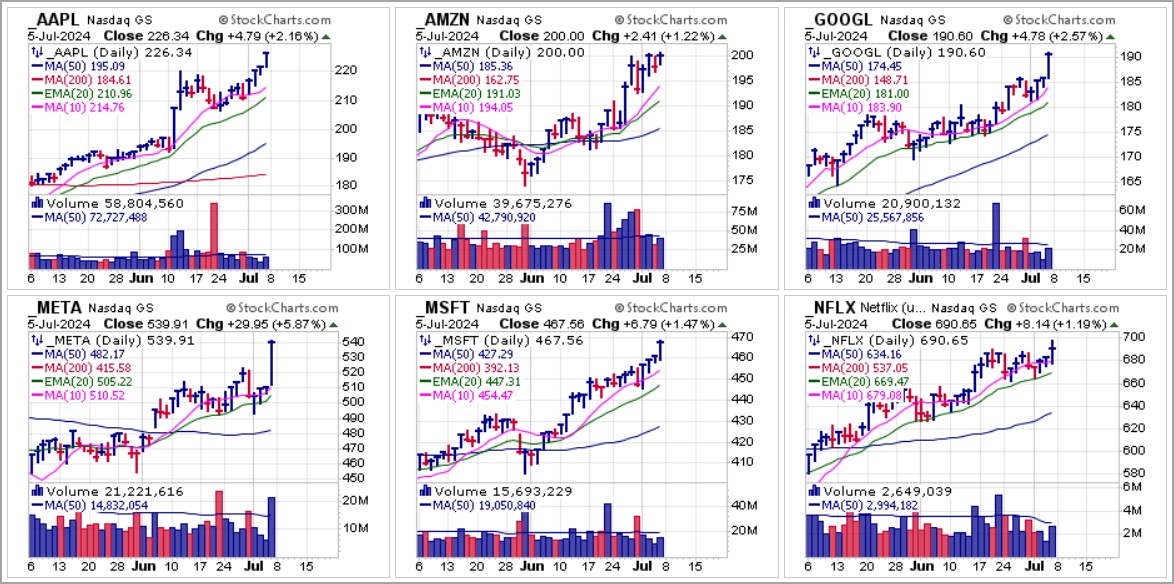

Money continues to pour into the biggest of the mega-cap NASDAQ names, as Apple (AAPL), Amazon.com (AMZN), Alphabet (GOOGL), Meta Platforms (META), Microsoft (MSFT), and Netflix (NFLX) continue to move higher. Volume has been low for the most part, but META broke out of a 13-week base formation Friday on strong volume. AMZN closed right at the $200.00 Century Mark, so for now sits on the fence between playing out as a possible Jesse Livermore Century Mark long entry if it can decisively clear $200 or a Century Mark short entry if it fails at the $200 level.

This week we will see the Consumer Price Index (CPI) on Thursday morning, expected to be up 0.1%, while the Producer Price Index (PPI) will be released on Friday morning. On Tuesday, Fed Chair Jerome Powell begins his multi-day testimony before Congress. All of this has the potential to move markets so we would remain alert to potential changes as stocks react to the data and Powell's testimony.

The Market Direction Model (MDM) switched to a BUY signal on Friday, July 5, 2024.