Major market indexes slowed this past week ahead of the Consumer Price Index and Producer Price Index reports on Tuesday and Wednesday, respectively and the main event, Wednesday's Fed policy announcement. Fed Fund Futures currently predict at 76.2% chance of a Fed skip as the markets expect the Fed to sit tight and keep rates unchanged. Markets gapped higher at the open on Friday on media hype claiming that the S&P 500 had emerged from a bear market by virtue of the fact that it had rallied 20% off the March lows. This is a highly arbitrary method of determining bull and bear market since nearly 4/5ths of the S&P’s performance in 2023 is due to the performance of five big-cap AI-meme related stocks, Apple (AAPL), Amazon.com (AMZN), Alphabet (GOOG), Microsoft (MSFT) and Nvidia (NVDA) while all of the NASDAQ’s performance in 2023 has been due entirely to AI meme-related stocks. In our view, this is an overly simplistic and misleading way of declaring a new bull market. Thus, superficial percentage rallies in the major market indexes are sliced and diced to conform to a generic market view that does not sync very well with the underlying reality of the market as a whole.

Inflation data and the Fed policy announcement this coming week will likely play a strong role in determining future market direction. If inflation comes in hot, the Fed will likely have to hike more than once. If inflation continues to cool AND comes in at or below expectations, we could see a continuation of the very narrowly led rally. Markets have not been this lopsided in history with so many industry groups trading sideways or in downtrends. The advance/decline line across major indices speaks to this fact.

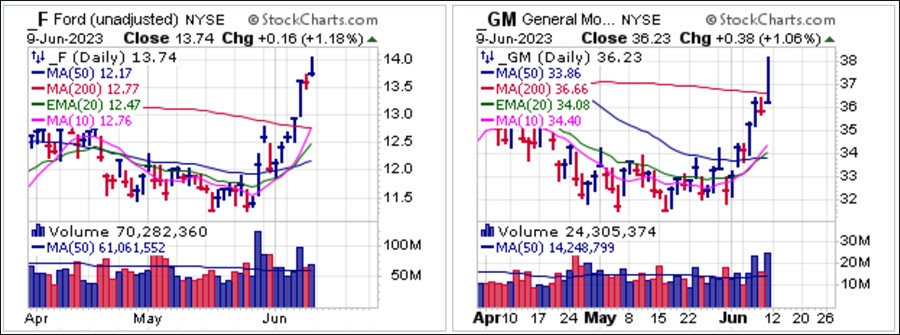

On Friday we reported on several exhaustion gap moves. Two of the more prominent exhaustion gaps were seen in Ford (F) and General Motors (GM) as they gapped higher on news that F had reached an agreement whereby its electric vehicles would be able to charge up as Tesla's Supercharger Stations. GM had previously reached such an agreement with TSLA. F reversed from an early gap-up open to close near its intraday lows while GM reversed even more sharply from opening gap-up highs to close back below its 200-dma, triggering a short-sale entry at the line which is then used as a covering guide.

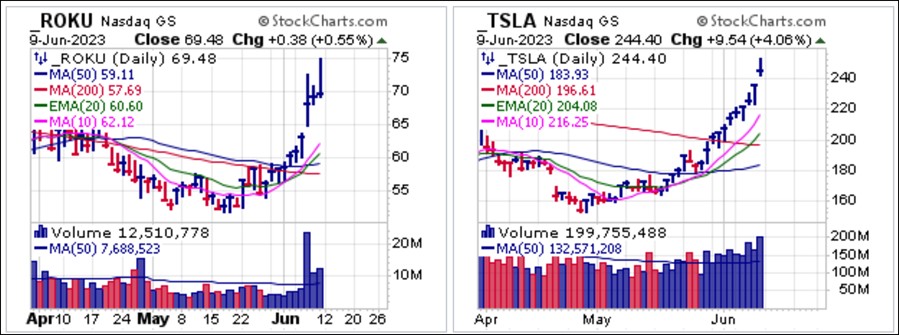

Similar exhaustion moves were also seen in Roku (ROKU) and Tesla (TSLA). TSLA was of course gapping higher after an extended parabolic move to the upside from the late April and early May lows on the news of its agreement with F. This may turn out as an exhaustion gap with the simple idea of any break below the 242.02 intraday low of Friday's gap-up move triggering a short-sale entry using that same 242.02 level as a covering guide. ROKU rallied on Friday after its soon-to-be ex-CFO presented at research firm Rosenblatt's Age of AI Conference pitching what is essentially targeted advertising technology as the Age of AI.

We also revised our view on Adobe (ADBE) which was originally reported on as a buyable gap-up. Certainly, it can be treated as a buyable gap-up but if Friday's intraday low at 453.09 is broken it could easily trigger as a short-sale entry into the gap-up move. Note the extended nature of the current trend. Typically, buyable gap-up moves closer to an area of consolidation will have a better success rate. In addition, it is not advisable to take a position in this extended state given that ADBE is expected to report earnings this Thursday after the close.

Market Direction Model (MDM) remains on a CASH signal.