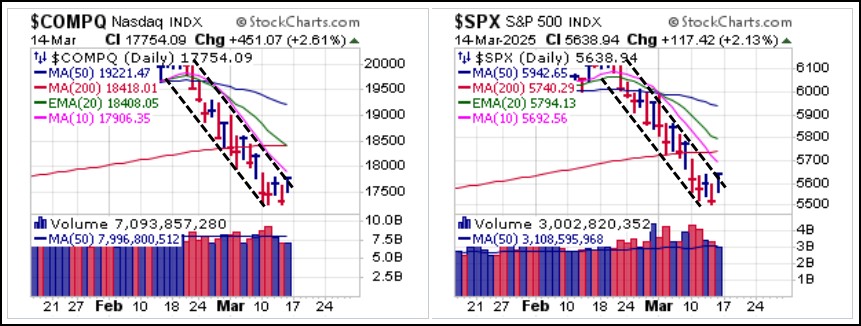

The S&P 500 posted the fifth fastest 10% decline off the peak in over the past 75 years before bouncing at the end of the week as it attempts to find a low. Overall, however, the action in both the NASDAQ Composite and S&P 500 does not so far argue for anything beyond a bear flag type of consolidation of the prior sharp break off the peak, pending further evidence to the contrary.

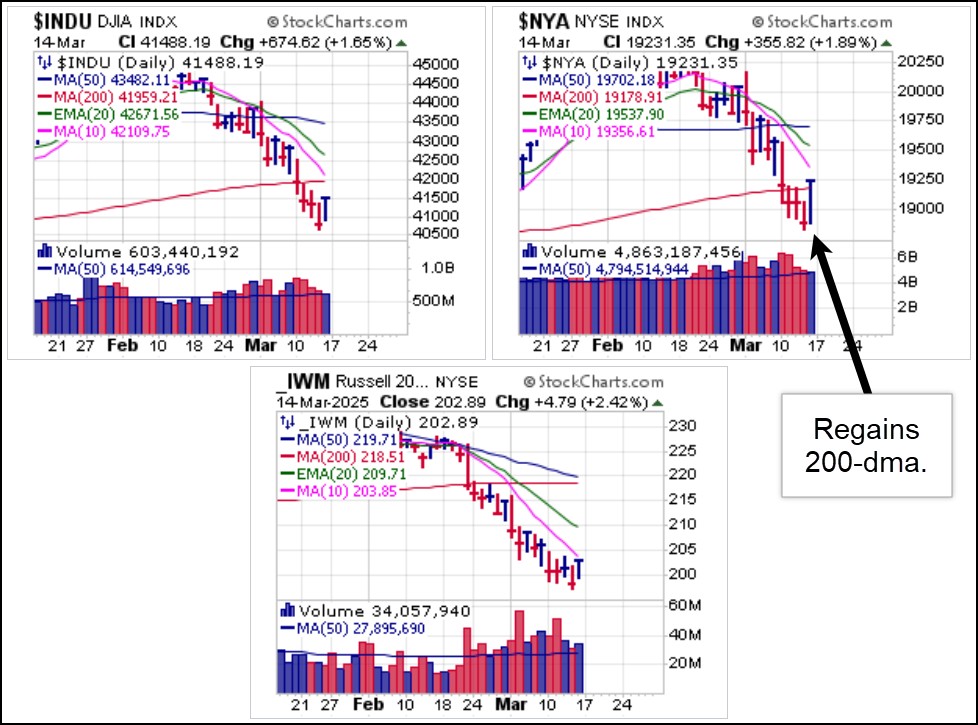

A subtle shift may be developing after all the major market indexes broke below 200-dma support early in the week. On Friday the broad NYSE Composite Index became the first of the major market indexes to regain 200-dma support. The index is decidedly non tech-centric and could potentially indicate rotation into previously underplayed areas of the market.

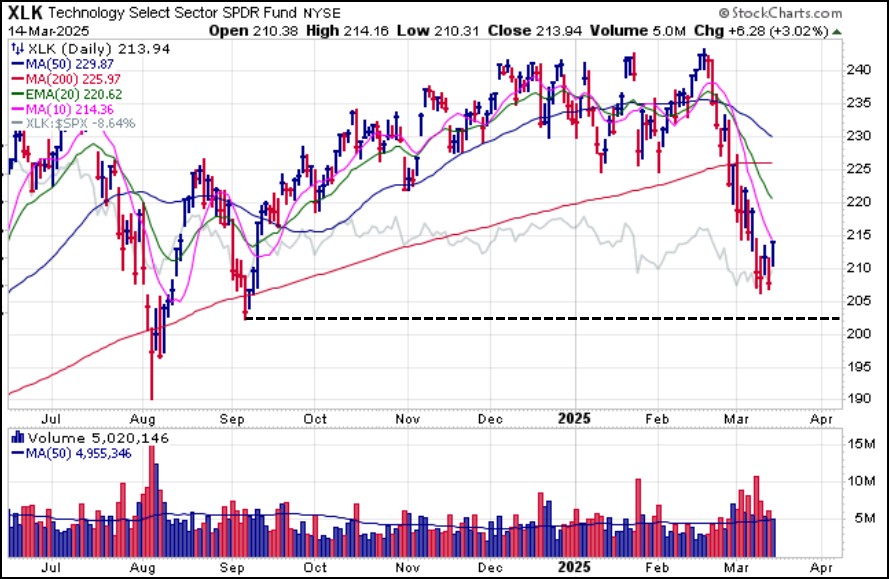

A subtle shift may be developing after all the major market indexes broke below 200-dma support early in the week. On Friday the broad NYSE Composite Index became the first of the major market indexes to regain 200-dma support. The index is decidedly non tech-centric and could potentially indicate rotation into previously underplayed areas of the market.  Over owned, overplayed, and overvalued tech stocks have taken the brunt of the selling over the past three weeks, and this is quite evident on the daily chart of the SPDR Select Sector Technology Fund (XLK) ETF. While the XLK and the general market could go lower, an oversold reflex rally from current levels is not out of the question either. Thus, we tend to think that the short-side game has become somewhat long in the tooth. We would therefore prefer to assess any oversold rally from current levels as a potential opportunity to re-enter shorts into such a rally.

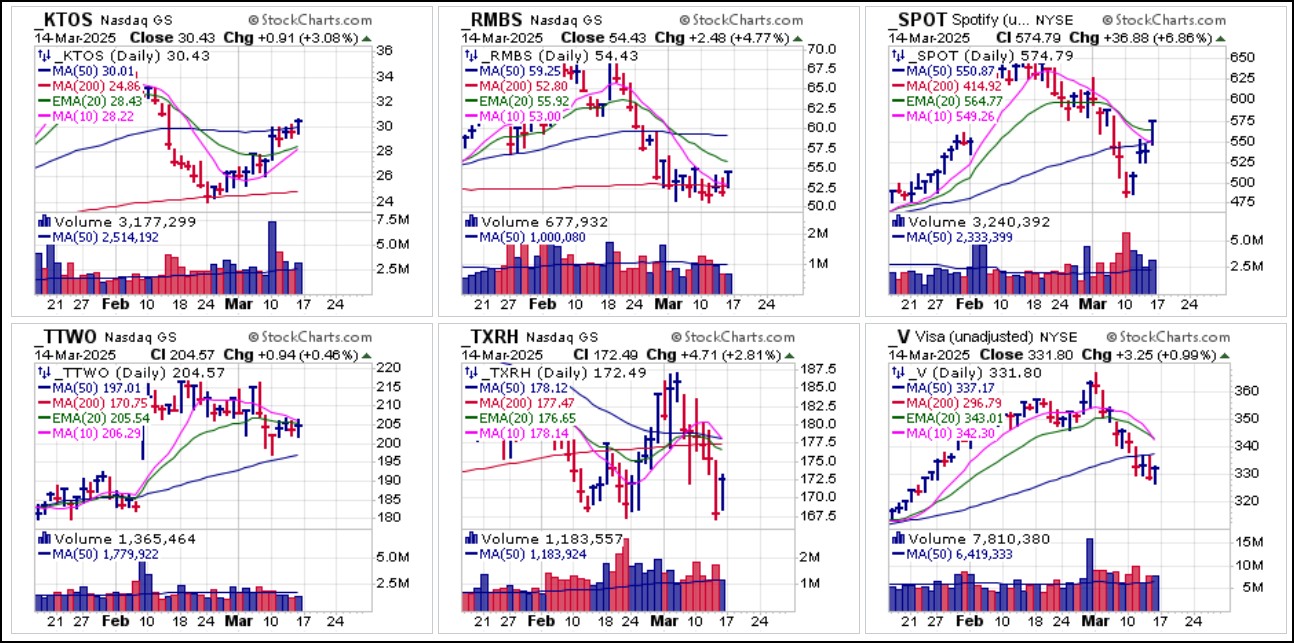

Over owned, overplayed, and overvalued tech stocks have taken the brunt of the selling over the past three weeks, and this is quite evident on the daily chart of the SPDR Select Sector Technology Fund (XLK) ETF. While the XLK and the general market could go lower, an oversold reflex rally from current levels is not out of the question either. Thus, we tend to think that the short-side game has become somewhat long in the tooth. We would therefore prefer to assess any oversold rally from current levels as a potential opportunity to re-enter shorts into such a rally. When the market sell-off began, over three weeks ago, we reported on several short-sale ideas via our Short-Sale Set-Up (SSS) reports at that time. All six shown below then moved lower from there, but more recently have begun to stabilize and turn. Obviously, as stocks continue to come down the odds of an oversold reflex rally increase, so timing is everything.

When the market sell-off began, over three weeks ago, we reported on several short-sale ideas via our Short-Sale Set-Up (SSS) reports at that time. All six shown below then moved lower from there, but more recently have begun to stabilize and turn. Obviously, as stocks continue to come down the odds of an oversold reflex rally increase, so timing is everything. We also note that SSS reports sent out on other stocks over the past week or so are also turning, and many, like Kratos Defense (KTOS) and Spotify (SPOT) are regaining 50-dma support. This offers market feedback that adds evidence that the short side is potentially near-term overplayed and ready to turn.

We also note that SSS reports sent out on other stocks over the past week or so are also turning, and many, like Kratos Defense (KTOS) and Spotify (SPOT) are regaining 50-dma support. This offers market feedback that adds evidence that the short side is potentially near-term overplayed and ready to turn. Gold remains the top-performing asset of 2025, now up 13.5% vs. stocks at -1.0%. Gold Futures ended the week at another all-time high, closing above the $3,000/oz. level for the first time. Gold's move to new highs comes two weeks after it posted its first down week of the year and looked set for a test of 50-dma support. The action lends credence to the argument that the move in gold is less about technicals and more about fundamentals.

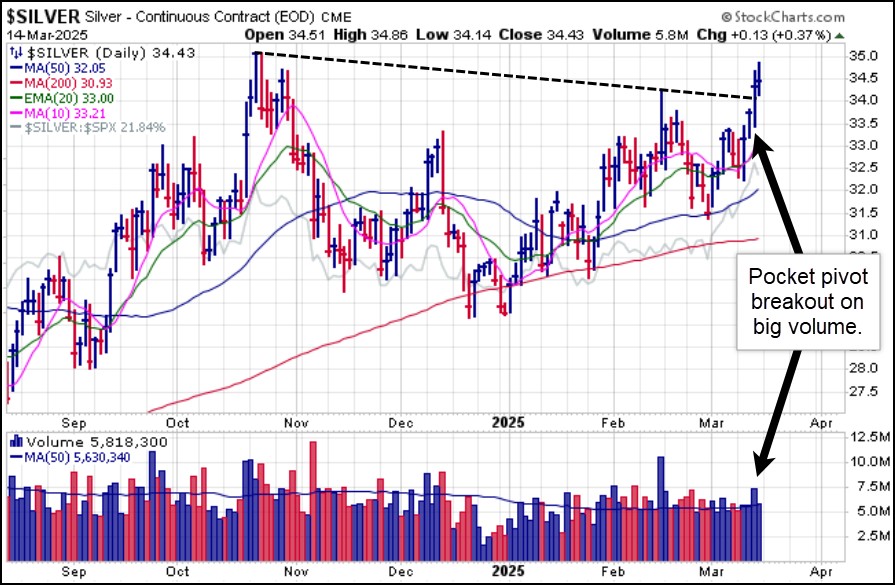

Gold remains the top-performing asset of 2025, now up 13.5% vs. stocks at -1.0%. Gold Futures ended the week at another all-time high, closing above the $3,000/oz. level for the first time. Gold's move to new highs comes two weeks after it posted its first down week of the year and looked set for a test of 50-dma support. The action lends credence to the argument that the move in gold is less about technicals and more about fundamentals. As gold has pushed to all-time highs silver follows along, but remains well below its early 2011 highs near $50. Silver Futures posted a pocket pivot trendline breakout on Thursday and ended the week at $34.43/oz., their highest close since mid-October of last year. As gold contents with the psychologically important $3,000 level, where some backing-and-filling could occur, silver may continue to play catch up as the current Gold-to-Silver ratio reaches 87.1, above the allegedly key 80 level where silver becomes compelling cheap relative to gold. We would look for support on any pullbacks at the rapidly rising 10-dma and 20-dema from here.

As gold has pushed to all-time highs silver follows along, but remains well below its early 2011 highs near $50. Silver Futures posted a pocket pivot trendline breakout on Thursday and ended the week at $34.43/oz., their highest close since mid-October of last year. As gold contents with the psychologically important $3,000 level, where some backing-and-filling could occur, silver may continue to play catch up as the current Gold-to-Silver ratio reaches 87.1, above the allegedly key 80 level where silver becomes compelling cheap relative to gold. We would look for support on any pullbacks at the rapidly rising 10-dma and 20-dema from here. As gold and silver rally, gold and silver mining stocks move up sharply and in some cases have broken out to new highs. Agnico-Eagle Mines (AEM) this past week broke out and cleared the $100 Century Mark for the first time, triggering a Livermore Century Mark Rule long entry using the $100 level as a selling guide. Strength was seen across the board in both gold and silver miners, with now big-stock silver miner First Majestic Silver (AG) posting several big-volume pocket p ivot signatures as it cleared 200-dma resistance early in the week.

As gold and silver rally, gold and silver mining stocks move up sharply and in some cases have broken out to new highs. Agnico-Eagle Mines (AEM) this past week broke out and cleared the $100 Century Mark for the first time, triggering a Livermore Century Mark Rule long entry using the $100 level as a selling guide. Strength was seen across the board in both gold and silver miners, with now big-stock silver miner First Majestic Silver (AG) posting several big-volume pocket p ivot signatures as it cleared 200-dma resistance early in the week.  Bitcoin ($BTCUSD) remains below 200-dma resistance where it is technically a short entry at the line which is then used as a covering guide. It is difficult to discern where any further potential upside catalysts for Bitcoin will come from unless the former CEO of Strategy (MSTR) Michael Saylor is able to cajole the Trump Administration into the absurd idea of buying up 25% of all Bitcoin in order to drive up prices and magically eliminate the current U.S. debt of $36.6 trillion. The idea that one can eliminate one's debt by cornering crypto and driving up the price fails on one basic reality: once you have driven the price higher, to whom do you sell it?

Bitcoin ($BTCUSD) remains below 200-dma resistance where it is technically a short entry at the line which is then used as a covering guide. It is difficult to discern where any further potential upside catalysts for Bitcoin will come from unless the former CEO of Strategy (MSTR) Michael Saylor is able to cajole the Trump Administration into the absurd idea of buying up 25% of all Bitcoin in order to drive up prices and magically eliminate the current U.S. debt of $36.6 trillion. The idea that one can eliminate one's debt by cornering crypto and driving up the price fails on one basic reality: once you have driven the price higher, to whom do you sell it?And if this "strategy" is indeed sound, why not apply it to any asset, like Apple (AAPL) or Virgin Galactic (SPCE) stock or even Copper or Silver Futures as part of a broader Sovereign Wealth Fund strategy? It is also quite ironic that while Bitcoin was supposedly going to free the humanoid inhabitants of Planet Earth from the "shackles of corrupt governments" it now relies on those same governments to buy it and hoard it in order to drive the price higher. It is the ultimate act of talking your book in the most hypocritical of terms.

Perhaps Bitcoin will find saving grace in MSTR's continued Ponzi Scheme of issuing debt in order to buy and prop up the price of $BTCUSD. Last week the company dumped a $21 billion at-the-market secondary stock offering of Series A Preferred shares into the market to raise money to buy, what else, more $BTCUSD. Perhaps MSTR as a single major buyer can only hope to corner the $BTCUSD market, but ultimately this cannot be healthy for the future of crypto. Hopefully, Bitcoin can find its true compass once again and regroup after declining over 30% from the mid-January peak without all the hype, hoopla, and manipulation.

The Market Direction Model (MDM) remains on a SELL signal.

The Market Direction Model (MDM) remains on a SELL signal.