Major market indexes finally found their feet on Thursday as the S&P 500 and NASDAQ Composite Indexes shook out at their 200-day moving averages, effectively holding support at the line. The indexes looked primed for lower lows on Thursday morning until non-voting Fed member and President of the Atlanta Fed Raphael Bostic made comments that he favored a quarter-point rate hike at the March Fed meeting and believes that the Fed could find itself in a position to pause rate hikes by summer time. That sent the market suddenly rallying to the upside, but from a purely technical standpoint it can be argued that the indexes were simply set up to rally after becoming near-term oversold amid a month-long sell-off from the February 2nd peak.

Early in the week we reported on Meta Platforms (META) on Tuesday as it posted a pocket pivot along its 20-day exponential moving average. It has since moved higher and on Friday posted another pocket pivot on a gap-up move.

We also reported on Osisko Gold Royalties Ltd. (OR) the same day as it posted a pocket pivot two Fridays ago on a massive outside reversal and shakeout after reporting earnings and then posted another one on Tuesday of this past week. It has since moved higher and is now looking to test its late January highs.

We also reported on Osisko Gold Royalties Ltd. (OR) the same day as it posted a pocket pivot two Fridays ago on a massive outside reversal and shakeout after reporting earnings and then posted another one on Tuesday of this past week. It has since moved higher and is now looking to test its late January highs. MP Materials (MP) was reported on as a potential Short-Sale Set-Up (SSS) after it had triggered a double-top entry at the 35.33 February 2nd high and the 36.09 of November 15th. We discussed this in real-time as the set-up was unfolding along the 36.09 high during our live market webinar on Wednesday morning, and MP then gapped lower the next day. It traded down to the 50-dma where it reached a logical cover point after a 15-20% downside break. The stock is now rallying back up through its 200-dma as it makes an attempt to test the Wednesday high.

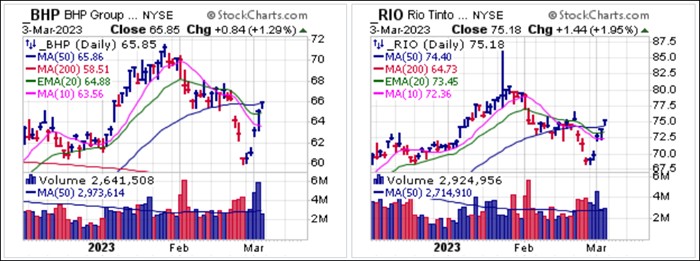

MP Materials (MP) was reported on as a potential Short-Sale Set-Up (SSS) after it had triggered a double-top entry at the 35.33 February 2nd high and the 36.09 of November 15th. We discussed this in real-time as the set-up was unfolding along the 36.09 high during our live market webinar on Wednesday morning, and MP then gapped lower the next day. It traded down to the 50-dma where it reached a logical cover point after a 15-20% downside break. The stock is now rallying back up through its 200-dma as it makes an attempt to test the Wednesday high. We also reported on copper producers BHP Group (BHP) and Rio Tinto (RIO) as stocks to watch for potential short-sale set-ups as they began to rally up towards moving average resistance earlier in the week. So far, BHP has rallied past its 10-dma and 20-dema and is now running into resistance at the 50-day moving average. RIO gapped past its 50-day line on Friday. Both stocks have continued to rally with the market so if this rally gives way at any point, both can be watched for potential short-sale entry triggers as they run into resistance or break back below their respective 50-day moving averages. As always, the short side will tend to work best when the market is going lower.

We also reported on copper producers BHP Group (BHP) and Rio Tinto (RIO) as stocks to watch for potential short-sale set-ups as they began to rally up towards moving average resistance earlier in the week. So far, BHP has rallied past its 10-dma and 20-dema and is now running into resistance at the 50-day moving average. RIO gapped past its 50-day line on Friday. Both stocks have continued to rally with the market so if this rally gives way at any point, both can be watched for potential short-sale entry triggers as they run into resistance or break back below their respective 50-day moving averages. As always, the short side will tend to work best when the market is going lower. On balance, long ideas worked better than our short ideas which is logical given that the market rallied on the final two days of the week, with MP being a welcome exception. The question is whether pocket pivots early in the week in META and OR have the ability sustain more intermediate-term trends or whether they simply play out as swing trades. With both the S&P and the NASDAQ Composite closing above their 10-day and 20-day moving averages, we could potentially test the February 2 highs in another rally within a continuing choppy and trendless market.

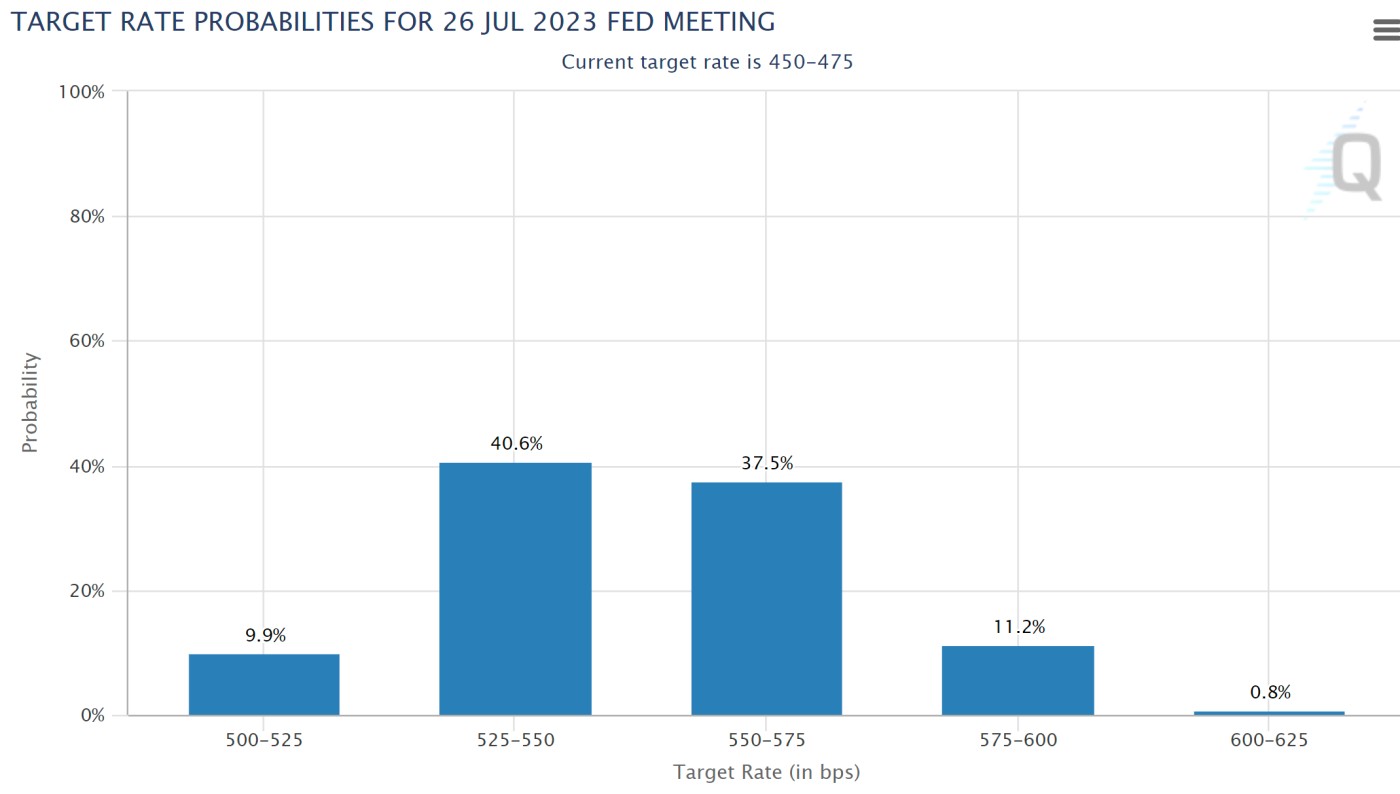

On balance, long ideas worked better than our short ideas which is logical given that the market rallied on the final two days of the week, with MP being a welcome exception. The question is whether pocket pivots early in the week in META and OR have the ability sustain more intermediate-term trends or whether they simply play out as swing trades. With both the S&P and the NASDAQ Composite closing above their 10-day and 20-day moving averages, we could potentially test the February 2 highs in another rally within a continuing choppy and trendless market.The Market Direction Model (MDM) remains on a SELL signal. The economy is not cooling down at the pace the Fed had hoped which is temporarily bullish for the market, but bearish in the longer run as the market is pricing in higher future interest rates and the dollar continues to bounce. The jobs report released Fri March 10 may show, once again, a tight labor market which will further fuel the odds of at least 3 more 25 bps rate hikes. As of now, CME Fed fund futures shows a fourth 25 bps rate hike is in second place at 37.5% which would bring the terminal rate to 550-575.

Given the record pace of rate hikes since the Fed started to tighten, a serious recession in the US, UK, and EU is in the offing as various metrics are already showing that delinquencies are soaring as nearly 2/3 in the US and UK are living paycheck-to-paycheck which will inevitably impact corporate earnings. Meanwhile, sticky inflation persists brought on by persistent supply chain issues, supply shortages of critical commodities such as fertilizer and wheat contributing to food inflation, as well as government overregulation in industries such as healthcare and education which prevents fair competition.