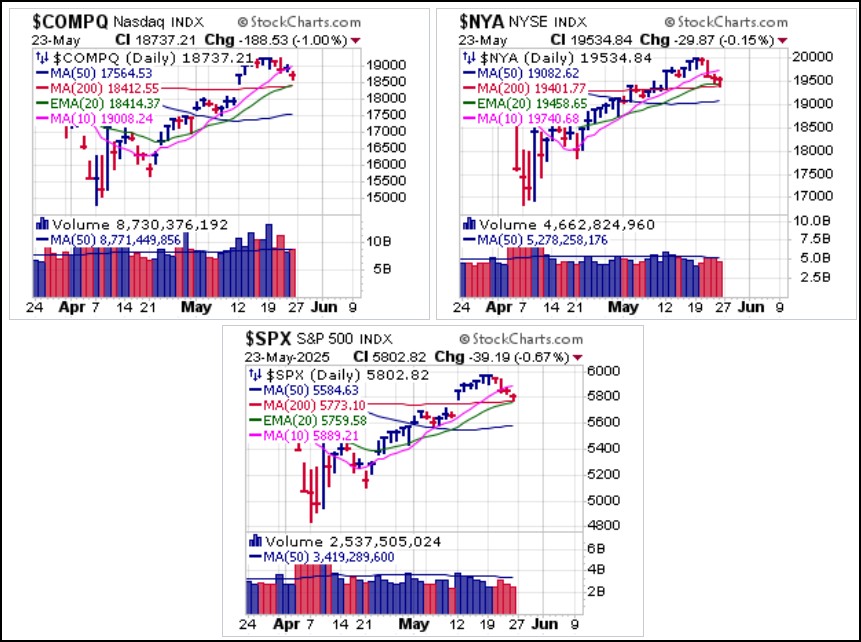

Major market indexes rolled over into the end of the week following a weak 20-Year U.S. Treasury auction on Wednesday. This was followed on Friday by the President threatening 50% tariffs on the European Union as he claimed that "trade talks are going nowhere." The President also threatened a 25% tariff on Apple products, specifically iPhones, if the company does not shift manufacturing to the United States.

The tariff news upset a flattish futures market early on Friday before the open, and while the NASDAQ Composite sold off exactly -1.00%, the S&P 500 was down -0.67% and the much broader non-techcentric NYSE Composite sold off just a hair -0.15%. Nevertheless, the indexes spent the balance of the week pulling back and are now testing 200-dma support.

The Friday action, which was relatively contained, seemed indicative of a market weighing the possibility that the tariff threats are just another Chicken Trade where the President is merely engaged in a trade-related Game of Chicken and is not likely to follow-through on his threats. Either way, the idea that trade talks with the EU are going nowhere flies in the face of the Administration's claims of great progress on the trade front as U.S. trade partner countries allegedly line up around the block to make a deal. Meanwhile, the President's Big, Beautiful Bill is up for a vote in the Senate after passing through the House last week, but ultimately it does not address the 800-lb. gorilla in the room, the growing government spending deficit, national debt, and the cost of servicing that debt.

The Friday action, which was relatively contained, seemed indicative of a market weighing the possibility that the tariff threats are just another Chicken Trade where the President is merely engaged in a trade-related Game of Chicken and is not likely to follow-through on his threats. Either way, the idea that trade talks with the EU are going nowhere flies in the face of the Administration's claims of great progress on the trade front as U.S. trade partner countries allegedly line up around the block to make a deal. Meanwhile, the President's Big, Beautiful Bill is up for a vote in the Senate after passing through the House last week, but ultimately it does not address the 800-lb. gorilla in the room, the growing government spending deficit, national debt, and the cost of servicing that debt.This keeps alternative-currencies in focus, as gold found ready support at the 50-dma and is now on the verge of a trendline breakout. It was last buyable as it shook out along 50-dma support, finishing the week at $3,358.00 an ounce.

Silver also trended higher for the week. On Tuesday the iShares Silver Trust (SLV) posted a pocket pivot trendline breakout and then retested that breakout level and 50-dma support the next day. It held and bounced back to the upside on Friday as it looks to challenge the prior late April highs.

Silver also trended higher for the week. On Tuesday the iShares Silver Trust (SLV) posted a pocket pivot trendline breakout and then retested that breakout level and 50-dma support the next day. It held and bounced back to the upside on Friday as it looks to challenge the prior late April highs. As the market pulls back and the U.S. Dollar ($USD continues to sink, Bitcoin's ($BTCUSD) mettle as an alternative-currency will be put to the test. Since the early April stock market lows, it has rallied with stocks as a risk-on asset. If the stock market continues to come off and $BTCUSD holds its ground, it raises the possibility of a new emphasis on King Crypto as an alternative-currency. Meanwhile, $BTCUSD has failed to hold a breakout to all-time highs, reversing earlier in the week at the $109,340.21 left-side peak in the pattern.

As the market pulls back and the U.S. Dollar ($USD continues to sink, Bitcoin's ($BTCUSD) mettle as an alternative-currency will be put to the test. Since the early April stock market lows, it has rallied with stocks as a risk-on asset. If the stock market continues to come off and $BTCUSD holds its ground, it raises the possibility of a new emphasis on King Crypto as an alternative-currency. Meanwhile, $BTCUSD has failed to hold a breakout to all-time highs, reversing earlier in the week at the $109,340.21 left-side peak in the pattern.That said, it has had quite a run off the April lows so is entitled to a period of consolidation, and an area of double-top resistance along the left-side of a big cup formation is logical. $BTCUSD is now testing 10-dma support where a potential pullback entry is possible using the 10-day line as a tight selling guide for any portion of a position added at these higher prices.

As tech stocks have led the market rally off the April lows, expect them to lead any pullback in the major market indexes. The SPDR Select Sector Technology (XLK) ETF illustrates the group pullback towards 200-dma support that correlates to the tech-centric index action.

As tech stocks have led the market rally off the April lows, expect them to lead any pullback in the major market indexes. The SPDR Select Sector Technology (XLK) ETF illustrates the group pullback towards 200-dma support that correlates to the tech-centric index action.

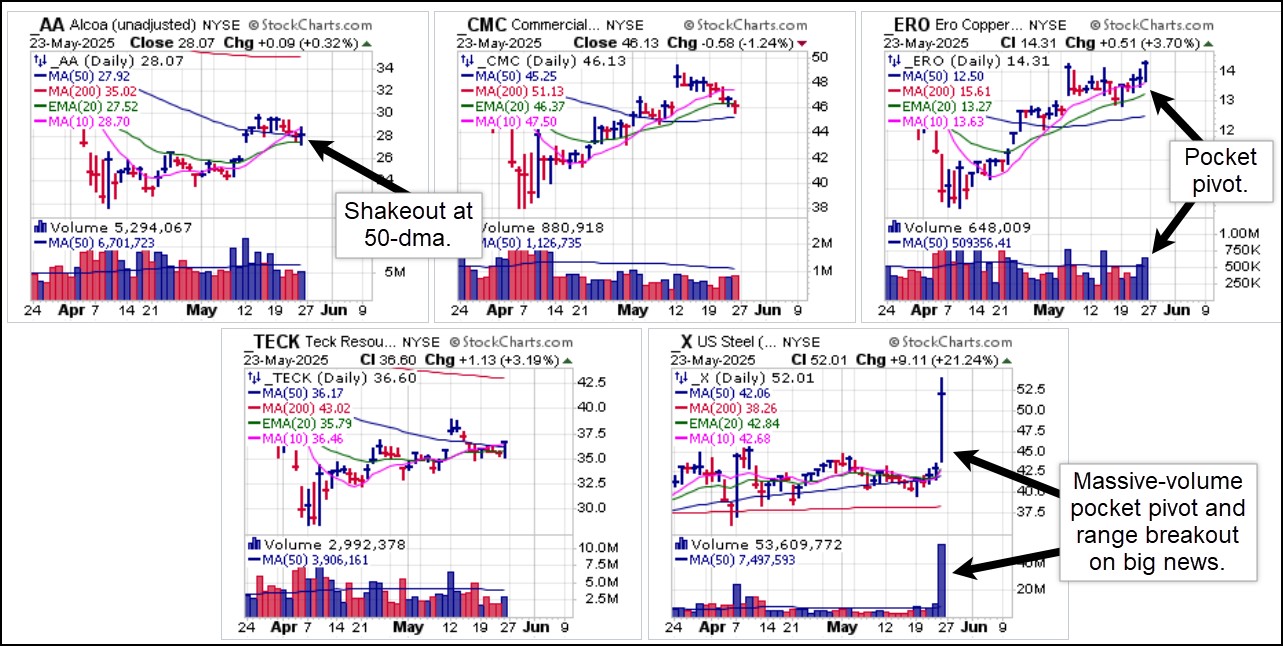

We tend to think that if this market rally is going to continue, the action will have to expand into different areas. Industrial metals has been one such are where we have seen constructive action, but in many cases it has not resulted in significant price upside, if at all. On Wednesday we reported on low-volume and VDU pullbacks in aluminum Alcoa (AA), steels Commercial Metals (CMC) and U.S. Steel (X), and coppers Ero Copper (ERO) and Teck Resources (TECK). With the exception of ERO and X, the action since then has been tepid and slightly to the downside.

That said, AA shook out at 50-dma support on Friday, a moving average U&R at the line while TECK did the same. CMC continues to drift lower and is now pulling into 50-dma support, below what is now 20-dema resistance. ERO came through with a big-volume pocket pivot move on Friday as it posted a higher closing in a three-week flag breakout attempt. X held support along the 50-dma until Friday when it blasted higher after President Trump said he would approve a business combination between X and Nippon Steel. That sent X on a massive-volume pocket pivot and range breakout to higher highs, and any VoSI members who bought this along the 50-dma on Wednesday or Thursday had a very nice end to their trading week.

This remains a challenging market, where the potential for Black Swans to suddenly appear remains high, such as we saw two Friday's ago with Moody's downgrade of the U.S. credit rating to AA1 from AAA, the weak Japanese government bond auction on Tuesday, and the weak 20-Year U.S. Treasury auction on Wednesday, followed by Trump's threat of 50% tariffs on the EU on Friday. Nevertheless, the market has held up relatively well in part due to ongoing measures of quantitative easing in all its forms which spurs global liquidity. But the question remains whether Trump's threat is just another Chicken Trade, or an indication that the trade negotiations following the initial tariff salvo on April 2nd, the so-called Liberation Day are deteriorating?

We will look for further answers this coming week as May comes to a close. Also note that big-stock AI tech darling Nvidia (NVDA) may serve as a market catalyst for the tech sector when it reports earnings as expected on Wednesday after the close.

The Market Direction Model (MDM) switched to a SELL signal on Monday, May 19, 2024, and then switched to a BUY signal on Tuesday, May 20, 2024, where it remains.