It has been a wild week for the major market indexes after last weekend's events in Israel. An initial sell-off on Monday was rebuffed as a relief rally off the intraday lows ensued based on three factors: 1) by Monday the situation in Israel did not worsen, 2) hopes that the Fed would now have to respond to the Israeli crisis by lowering interest rates, and 3) an excessive amount of bearish sentiment and positioning from the prior week that still needed to burn off.

On Wednesday, the Producer Price Index (PPI) came in hot as the headline number printed 0.5% vs. expectations of 0.3%. One might have expected to see the market sell-off on such a report but instead the NASDAQ was able to push just above the 50-day moving average. Thursday's Consumer Price Index (CPI), which also came in hot with the headline number printing 0.4% vs. expectations of 0.3%, looked like it was going to trigger another rally early in the day but the prospect of higher inflation for longer and its implications for interest rates finally turned tipped the cart. The NASDAQ Composite ended the day reversing back to the downside and closing back below the 50-dma on heavy selling volume.By Friday, the situation in Israel was starting to heat up as the IDF began to move into Gaza, pouring fuel on the Thursday's selling fire. Volume was light as buyers stepped aside, unwilling to take fresh positions ahead of a potentially news volatile weekend as the news flow out of Israel remains extremely fluid. For now the index remains in a well-defined downtrend channel off the mid-July highs. In our view, there is no confirmed uptrend, which strikes as a naive fantasy. Underlying conditions in the current environment are nowhere near what they need to be in order foster an intermediate-term bull trend, and outside of normal reaction rallies, that may remain the case for some time.

We reported on several short-sale set-ups during the week as the NASDAQ rallied to and then failed at 50-day moving average resistance.

We reported on several short-sale set-ups during the week as the NASDAQ rallied to and then failed at 50-day moving average resistance.On Tuesday, October 10th, we reported on Apple (AAPL) and Adobe Systems (ADBE) as potential short-sale set-ups. We continue to look for a break below the 50-dma in AAPL as a potential short-sale entry trigger that then uses the 50-day as a covering guide. We were looking for the same thing in ADBE on Tuesday, but it kept rallying up to its prior early September highs.

By Thursday that set up a double-top short-sale (DTSS) entry along the left-side peak at 569.98 as it trade past the left-side peak and then reversed back below it to trigger the short-sale entry using the left-side peak at 569.98 as a selling guide. ADBE then pressed lower from there on Friday.

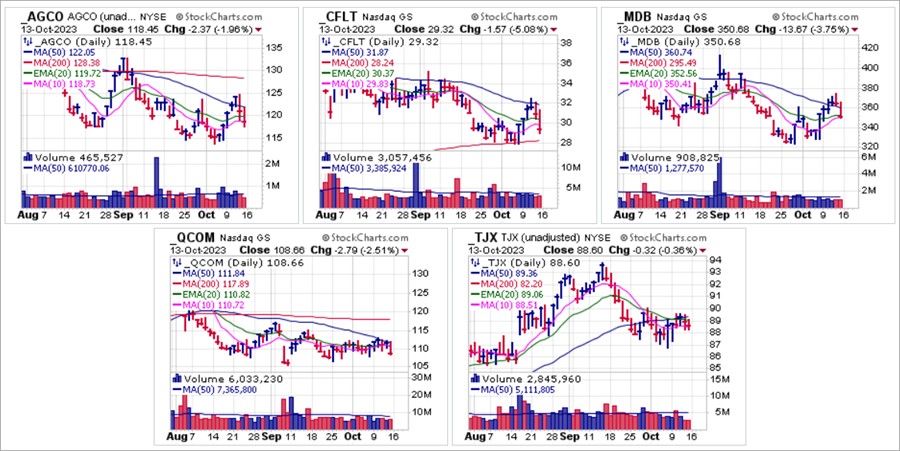

On Wednesday, October 11th, we reported on Agco (AGCO), Confluence (CFLT), MongoDB (MDB), Qualcomm (QCOM), and TJX Companies (TJX). All five of these were simple short-sale entries at their 50-day moving averages as they either reversed immediately at the line or traded just above it before reversing back below to trigger short-sale entries at that point. Of the five, the only one that remains within short-sale range of the 50-dma is TJX, using the 50-day line as a covering guide.

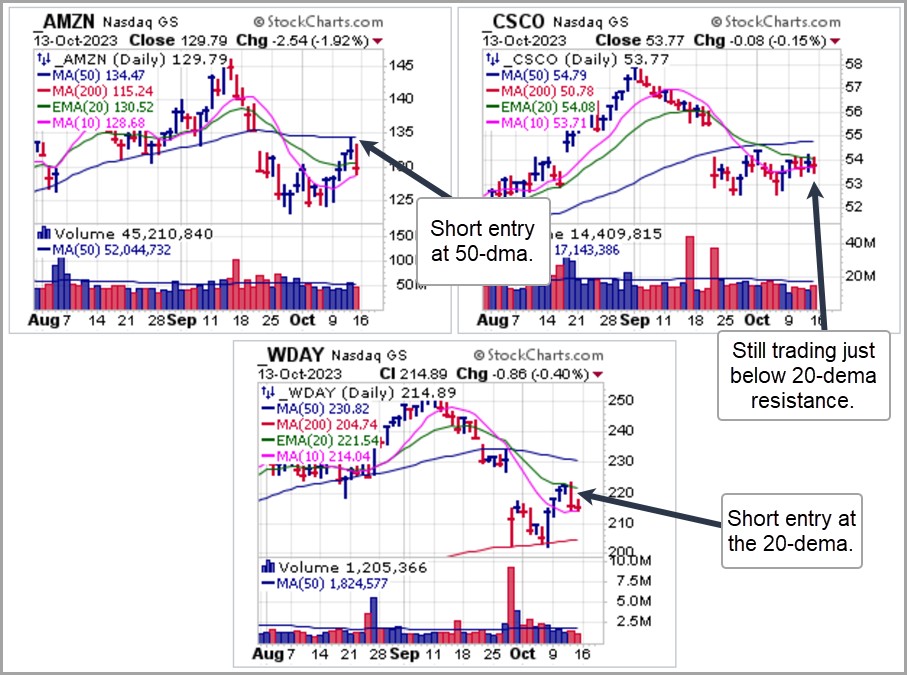

On Wednesday, October 11th, we reported on Agco (AGCO), Confluence (CFLT), MongoDB (MDB), Qualcomm (QCOM), and TJX Companies (TJX). All five of these were simple short-sale entries at their 50-day moving averages as they either reversed immediately at the line or traded just above it before reversing back below to trigger short-sale entries at that point. Of the five, the only one that remains within short-sale range of the 50-dma is TJX, using the 50-day line as a covering guide. On Thursday, we reported on Amazon.com (AMZN), Cisco Systems (CSCO), and Workday (WDAY). At that time, AMZN was pushing into shortable resistance at its 50-dma and it reversed beautifully back to the downside from there. On Friday it triggered a second short-sale entry at the 20-dema and finished the day just below the line. CSCO remains just below 20-dema resistance which puts it in a short-sale entry position using the 20-dema as a covering guide. WDAY on Thursday was pushing into 20-dema resistance where it presented a short-sale entry opportunity at the line and then reversed back to the downside from there. It closed Friday just above the 10-dma and can be watched for any break below the 10-day line that would trigger a fresh short-sale entry.

On Thursday, we reported on Amazon.com (AMZN), Cisco Systems (CSCO), and Workday (WDAY). At that time, AMZN was pushing into shortable resistance at its 50-dma and it reversed beautifully back to the downside from there. On Friday it triggered a second short-sale entry at the 20-dema and finished the day just below the line. CSCO remains just below 20-dema resistance which puts it in a short-sale entry position using the 20-dema as a covering guide. WDAY on Thursday was pushing into 20-dema resistance where it presented a short-sale entry opportunity at the line and then reversed back to the downside from there. It closed Friday just above the 10-dma and can be watched for any break below the 10-day line that would trigger a fresh short-sale entry. The Market Direction Model (MDM) remains on a SELL signal.

The Market Direction Model (MDM) remains on a SELL signal.