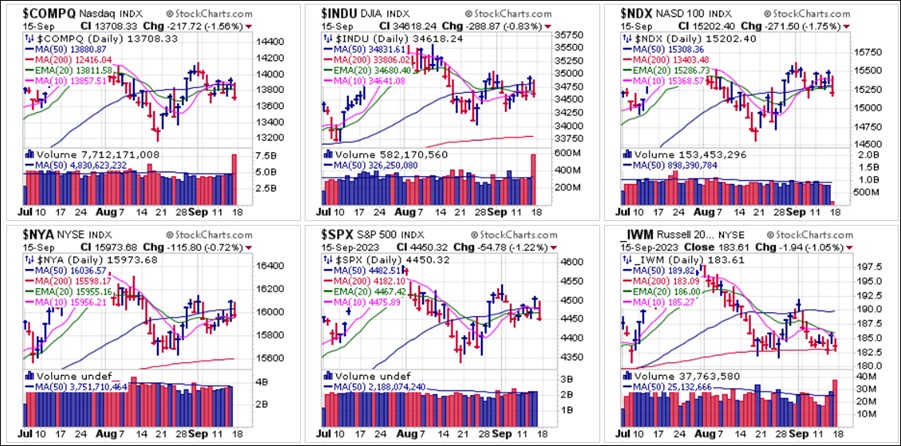

Major market indexes slid back below their 50-day moving averages on Friday after rallying on hot Consumer Price Index and Producer Price Index data on Wednesday and Thursday, respectively. Volume on Friday was very heavy due to quarter-end Quadruple-Witching Options Expiration. Thursday's move amid hot PPI data was a bit of a head scratcher, but may have been related to the massive $3.7 trillion in notional options value that was expiring the day after.

Friday's sell-off thus appeared to be a delayed reaction to what has been unfavorable inflation data for the Fed is Done narrative. This coming week we will see the Fed release its September policy statement, with CME Fed Watch showing a 97% probability that the Fed will leave rates as they are.

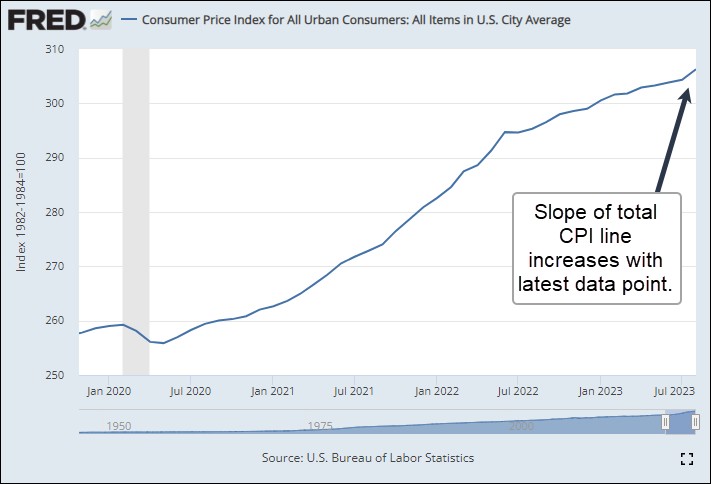

Headline CPI released on Wednesday rose 0.6% MoM (as expected), but the Year-over-Year rate came in at +3.7%, up from 3.2% last month and hotter than the 3.6% YoY number that was expected. The Producer Price Index (PPI) came in on Thursday and surprised with a 0.7% Month-over-Month gain in August vs. expectations of 0.4%. The number was also up from July which came in at 0.3% and was the highest MoM PPI change since June 2022. Year-over-Year, the PPI is up 1.6%.

It is important to understand, as we discussed in last weekend's Focus List Review, that inflation has not reversed. That cannot happen until and unless we see a negative sign (-) in front of the monthly CPI and PPI numbers. The slope of inflation remains positive, as it has since it began its upward trek in the spring of 2020. In addition, CPI data is distorted. The media fails to do its job by informing its audience that currently there is an ongoing monthly adjustment to the health insurance CPI that caused it to collapse by 33.6% year-over-year.The September CPI coming out in October will be the last month with this health insurance CPI adjustment. Therefore, when the October CPI is released in November, it will flip, which will add upward momentum to the CPI readings. CPI, core CPI, and core services CPI have been understated significantly since October last year, when the monthly health insurance adjustment started, basically a large data distortion as a result of coming out of the pandemic.

Even with that health insurance CPI negative adjustment, the CPI is again accelerating to the upside as the slope of the total CPI chart suddenly increases as a result of the latest inflation data release. Meanwhile, the PPI's 0.7% move in August represents a very strong reacceleration in what is considered to be a forward inflation gauge for CPI.

While the indexes tried to hold their ground this week, the underlying action in leading stocks was telling a different story. Since September 6th, we have released several Short-Sale Set-Up (SSS) Reports. We first reported on Nvidia (NVDA) two Wednesdays ago as it broke below the 480.88 left-side peak in its pattern, triggering a double-top short-sale (DTSS) entry at that point. We reported on the stock again on Friday as it triggered another short-sale entry along its 50-day moving average. At this stage rallies back up into the 50-dma would bring the stock back into optimal short-sale range so can be watched for.

While the indexes tried to hold their ground this week, the underlying action in leading stocks was telling a different story. Since September 6th, we have released several Short-Sale Set-Up (SSS) Reports. We first reported on Nvidia (NVDA) two Wednesdays ago as it broke below the 480.88 left-side peak in its pattern, triggering a double-top short-sale (DTSS) entry at that point. We reported on the stock again on Friday as it triggered another short-sale entry along its 50-day moving average. At this stage rallies back up into the 50-dma would bring the stock back into optimal short-sale range so can be watched for. On that same day we reported on several other short-sale set-ups as they were developing, including Broadcom (AVGO) on rallies into the 50-dma. The stock busted the 20-dema on Friday and continues lower such that only rallies into the 20-dema would bring it back into short-sale range.

On that same day we reported on several other short-sale set-ups as they were developing, including Broadcom (AVGO) on rallies into the 50-dma. The stock busted the 20-dema on Friday and continues lower such that only rallies into the 20-dema would bring it back into short-sale range. Rambus (RMBS) was reported on two Wednesday's ago as a possible short-sale entry as it into its 50-dma. However, it continued past the moving average by a reasonable margin before reversing back below the line on Friday. This would serve as a short-sale entry using the 50-dma as a tight covering guide

Rambus (RMBS) was reported on two Wednesday's ago as a possible short-sale entry as it into its 50-dma. However, it continued past the moving average by a reasonable margin before reversing back below the line on Friday. This would serve as a short-sale entry using the 50-dma as a tight covering guide Advanced Micro Devices (AMD) was reported on as a short-sale entry along its 50-dma two Wednesdays ago and it has since come lower. In this position we wouild watch for any rallies back up into the 20-dema which would bring it back into better short-sale range from here.

Advanced Micro Devices (AMD) was reported on as a short-sale entry along its 50-dma two Wednesdays ago and it has since come lower. In this position we wouild watch for any rallies back up into the 20-dema which would bring it back into better short-sale range from here. Meta Platforms (META) has held up along 50-dma support for the past week or so but on Friday dipped below its 50-day moving average where it triggers a short-sale entry using the 50-day line as a covering guide.

Meta Platforms (META) has held up along 50-dma support for the past week or so but on Friday dipped below its 50-day moving average where it triggers a short-sale entry using the 50-day line as a covering guide. Fortinet (FTNT) was another stubborn short-sale target after we reported on its two Wednesdays ago as a possible short-sale entry along 200-dma resistance. As we noted last week, that was perhaps in too far of an oversold position and, as it turned out, FTNT did push through 200-dma resistance before coming back in to break below the line on Friday. That triggered a short-sale entry at that point, using the 200-dma as a covering guide.

Fortinet (FTNT) was another stubborn short-sale target after we reported on its two Wednesdays ago as a possible short-sale entry along 200-dma resistance. As we noted last week, that was perhaps in too far of an oversold position and, as it turned out, FTNT did push through 200-dma resistance before coming back in to break below the line on Friday. That triggered a short-sale entry at that point, using the 200-dma as a covering guide. Marvell Technology (MRVL) continues to drift lower after we reported on it two Wednesday's ago as a short-sale entry along 20-dema resistance. Now we would watch for any rallies back up to the 20-demawhich would bring it back into better short-sale range from here.

Marvell Technology (MRVL) continues to drift lower after we reported on it two Wednesday's ago as a short-sale entry along 20-dema resistance. Now we would watch for any rallies back up to the 20-demawhich would bring it back into better short-sale range from here. We also reported on MongoDB (MDB) two weeks ago as it broke below 50-dma support. Since then it has rallied back up to the line once where a second short-sale opportunity was found, and on Friday ended the week at lower lows since the initial short-sale entry at the 50-dma.

We also reported on MongoDB (MDB) two weeks ago as it broke below 50-dma support. Since then it has rallied back up to the line once where a second short-sale opportunity was found, and on Friday ended the week at lower lows since the initial short-sale entry at the 50-dma. ZScaler (ZS) played out as a double-top short-sale entry (DTSS) along the 164.29 left-side peak in the pattern two Wednesdays ago but was then able to bounce back to the upside and clear to marginal higher highs this past Monday. That simply brought it back into optimal short-sale range by the time it triggered the DTSS entry at 164.29 again on Tuesday. On Friday it broke lower but found support at the 20-dema. If it breaks the 20-dema that would trigger a fresh short-sale entry so can be watched for.

ZScaler (ZS) played out as a double-top short-sale entry (DTSS) along the 164.29 left-side peak in the pattern two Wednesdays ago but was then able to bounce back to the upside and clear to marginal higher highs this past Monday. That simply brought it back into optimal short-sale range by the time it triggered the DTSS entry at 164.29 again on Tuesday. On Friday it broke lower but found support at the 20-dema. If it breaks the 20-dema that would trigger a fresh short-sale entry so can be watched for. On Friday we reported on two new short-sale set-ups. The first was in over-priced yoga pants maker Lululemon Athletica (LULU) as it failed on a recent breakout attempt. The stock is now testing the 20-dema and should be watched for any decisive break below the line which would trigger a short-sale entry using the line as a covering guide. Once LULU breaks 20-dema support it would also trigger an LSFB short-sale set-up in progress.

On Friday we reported on two new short-sale set-ups. The first was in over-priced yoga pants maker Lululemon Athletica (LULU) as it failed on a recent breakout attempt. The stock is now testing the 20-dema and should be watched for any decisive break below the line which would trigger a short-sale entry using the line as a covering guide. Once LULU breaks 20-dema support it would also trigger an LSFB short-sale set-up in progress. The second was CrowdStrike (CRWD) as it posted a double-top short-sale (DTSS) entry at the 166.99 left-side peak of August 1st. The stock closed Friday at 165.45 so remains within short-sale range using the 166.99 left-side peak as a covering guide.

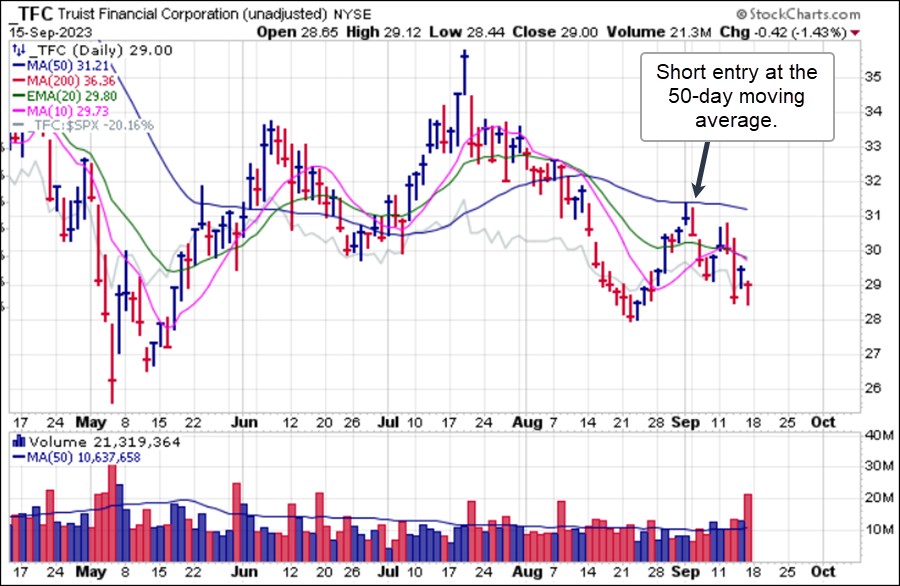

The second was CrowdStrike (CRWD) as it posted a double-top short-sale (DTSS) entry at the 166.99 left-side peak of August 1st. The stock closed Friday at 165.45 so remains within short-sale range using the 166.99 left-side peak as a covering guide. On September 5th we reported on Truist Financial (TFC) as a short-sale entry at 50-dma resistance. It then reversed and has steadily trended lower from there. In this position, only rallies into the 20-dema would bring it back into better short-sale range so can be watched for.

On September 5th we reported on Truist Financial (TFC) as a short-sale entry at 50-dma resistance. It then reversed and has steadily trended lower from there. In this position, only rallies into the 20-dema would bring it back into better short-sale range so can be watched for. Charles Schwab (SCHW) was reported on at the same time as it too ran into 50-dma resistance, offering a reasonable short-sale entry at the line which is then used as a covering guide. T his past week SCHW again rallied up into the 50-dma, giving shorts another shot at the stock and it has moved lower since. From here rallies into the 20-dema would bring it into short-sale range of that moving average while using it as a covering guide.

Charles Schwab (SCHW) was reported on at the same time as it too ran into 50-dma resistance, offering a reasonable short-sale entry at the line which is then used as a covering guide. T his past week SCHW again rallied up into the 50-dma, giving shorts another shot at the stock and it has moved lower since. From here rallies into the 20-dema would bring it into short-sale range of that moving average while using it as a covering guide. So far, short-sale set-ups we identified two Wednesdays ago or earlier have continued to decline. With the NASDAQ Composite closing Friday just 5.11% below its July 19th peak of 14446.55 more downside may be in store after Friday's break back below the 50-dma.

So far, short-sale set-ups we identified two Wednesdays ago or earlier have continued to decline. With the NASDAQ Composite closing Friday just 5.11% below its July 19th peak of 14446.55 more downside may be in store after Friday's break back below the 50-dma.The Market Direction Model (MDM) remains on a SELL signal.