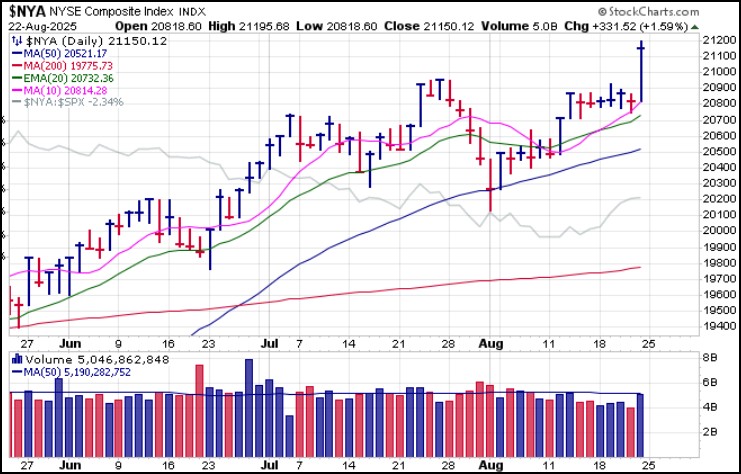

The evidence for this is also found in the sudden emergence of the broad NYSE Composite Index as the de facto big-stock market-leading index after thrusting to all-time highs on Friday while the other indexes rallied back up towards prior highs.

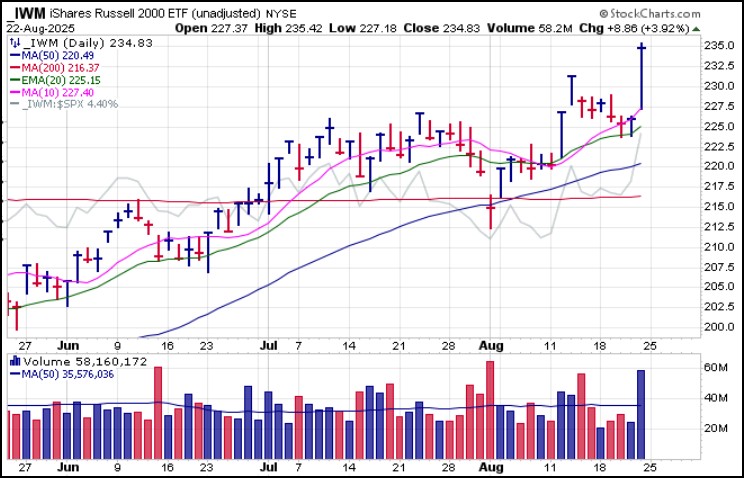

The evidence for this is also found in the sudden emergence of the broad NYSE Composite Index as the de facto big-stock market-leading index after thrusting to all-time highs on Friday while the other indexes rallied back up towards prior highs. The very broad Russell 2000 was the star of the show as it posted a very sharp 3.92% move on Friday as measured by the iShares Russell 2000 (IWM) ETF to lead all indexes as regional financials and other small-cap names exhibited a tidal wave of upside movement in response to a Fed that is now more open to interest rate cuts based on the realization as expressed by Powell on Friday that unemployment is slowing faster than expected.

The very broad Russell 2000 was the star of the show as it posted a very sharp 3.92% move on Friday as measured by the iShares Russell 2000 (IWM) ETF to lead all indexes as regional financials and other small-cap names exhibited a tidal wave of upside movement in response to a Fed that is now more open to interest rate cuts based on the realization as expressed by Powell on Friday that unemployment is slowing faster than expected.This, of course, should be no surprise to anyone after the last train wreck of a jobs report which included massive downside revisions to the two prior month's jobs gains. The only sticking point for Fed rate cuts is the fact that inflation has not abated as price levels consistently rise at an annualized 2.8% to 3.1% based on the government's understated numbers show. This Friday we will see the latest Personal Consumption Expenditures Inflation Index numbers, which could add clarity to the inflation picture.

This may be indicative of rotation into more interest-rate sensitive areas of the market, such as commodity-related names, as the AI-centric tech sector continues to work through concerns of an AI-overbuild in high-PE and high PE-expansion names that currently populate the space. This opens up the potential for money to flow out of overplayed AI-tech and into other areas of the market.

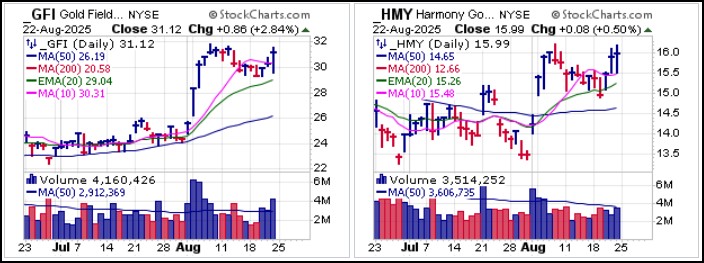

This may be indicative of rotation into more interest-rate sensitive areas of the market, such as commodity-related names, as the AI-centric tech sector continues to work through concerns of an AI-overbuild in high-PE and high PE-expansion names that currently populate the space. This opens up the potential for money to flow out of overplayed AI-tech and into other areas of the market.Gold and silver both rallied, but gold remains in a very tight 18-week base as it continues to tighten up. Friday's Powell speech pushed the SPDR Gold Trust (GLD) back above the 50-dma, although the 50-day line has not been a reliable reference as the yellow metal simply continues to base around the moving average in constructive fashion.

South African gold miners Gold Fields Ltd. (GFI) and Harmony Gold Mining (HMY) both posted pocket pivots on Friday. While miners were up strongly across the board on Friday, many of these are already in extended positions so not in chart positions where long entry set-ups can occur.

South African gold miners Gold Fields Ltd. (GFI) and Harmony Gold Mining (HMY) both posted pocket pivots on Friday. While miners were up strongly across the board on Friday, many of these are already in extended positions so not in chart positions where long entry set-ups can occur. Barrick Mining (B), for example, has been up 13 out of 16 days in a row and well extended on the upside since breaking out three weeks ago.

Barrick Mining (B), for example, has been up 13 out of 16 days in a row and well extended on the upside since breaking out three weeks ago. Silver via the iShares Silver Trust (SLV) posted a strong-volume pocket pivot on Friday off 20-dema support. The move occurred very quickly as Powell began to speak and is extended at this point.

Silver via the iShares Silver Trust (SLV) posted a strong-volume pocket pivot on Friday off 20-dema support. The move occurred very quickly as Powell began to speak and is extended at this point. Bitcoin ($BTCUSD) jacked back up through 50-dma resistance on Friday but over the weekend is slumping back below the 50-day line. This an interesting development ahead of the futures opening up later today on Sunday as you might expect some follow-through.

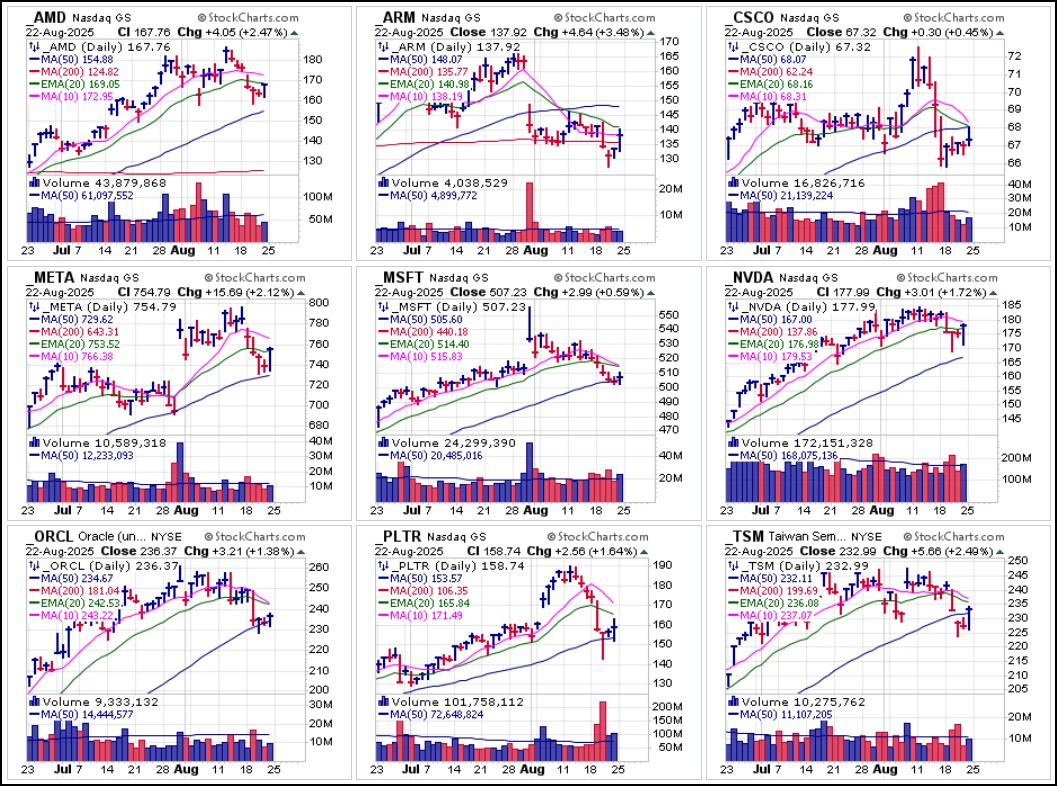

Bitcoin ($BTCUSD) jacked back up through 50-dma resistance on Friday but over the weekend is slumping back below the 50-day line. This an interesting development ahead of the futures opening up later today on Sunday as you might expect some follow-through. Meanwhile, big-stock AI-related techs, which have been beaten-down for several days, mostly staged oversold reaction rallies on Friday in reaction to Powell's speech. Many of these moves were relatively tepid within the context of these stocks' oversold condition coming into Friday. With many of these stocks down deep in their patterns, some have undercut moving averages in MAU&R style so could continue higher as the new trading week begins in potentially normal reaction bounces. Others, such as telecom leader Cisco Systems (CSCO) played out as a short-sale entry as it reversed at 50-dma resistance on Friday while Advanced Micro Devices (AMD) ran into and closed below 20-dema resistance, where it could potentially play out as a short-sale entry.

Meanwhile, big-stock AI-related techs, which have been beaten-down for several days, mostly staged oversold reaction rallies on Friday in reaction to Powell's speech. Many of these moves were relatively tepid within the context of these stocks' oversold condition coming into Friday. With many of these stocks down deep in their patterns, some have undercut moving averages in MAU&R style so could continue higher as the new trading week begins in potentially normal reaction bounces. Others, such as telecom leader Cisco Systems (CSCO) played out as a short-sale entry as it reversed at 50-dma resistance on Friday while Advanced Micro Devices (AMD) ran into and closed below 20-dema resistance, where it could potentially play out as a short-sale entry.Could Friday's move play out as classic one-day wonder rally? That is unknown until the new trading week commences on Sunday afternoon when futures start trading, but it is important to remember that while the media is calling Fed's vague comments a Fed pivot, in fact the Fed pivoted back in September of last year when it lowered rates 1/4% and then proceeded with a 1/2% cut in October before finally cutting rates another 1/4% in December, a total of 1% in four months.

Meanwhile, with Nvidia (NVDA) earnings due out on Wednesday, the AI-tech space will face a meaningful test which could have implications for the broader AI-related tech sector.

The Market Direction Model (MDM) switched to a CASH signal on Wednesday, August 20, 2025 before switching back to a BUY signal on Friday, August 22nd.

The Market Direction Model (MDM) switched to a CASH signal on Wednesday, August 20, 2025 before switching back to a BUY signal on Friday, August 22nd.