AI-related tech names are proving to be no less resistance to the virtuous cycle of creation and destruction that drives innovation in the tech space. Two weeks ago leading memory chip maker Micron Technology (MU) was pushing to all-time highs ahead of its earnings report on March 18th. Despite blowing away estimates and raising guidance, the stock tanked badly, triggering a double-top short-sale (DTSS) entry at the 455.50 left-side peak last week. It has continued to decline and now sits below the lows of its prior base from which it broke out two weeks ago.

AI-related tech names are proving to be no less resistance to the virtuous cycle of creation and destruction that drives innovation in the tech space. Two weeks ago leading memory chip maker Micron Technology (MU) was pushing to all-time highs ahead of its earnings report on March 18th. Despite blowing away estimates and raising guidance, the stock tanked badly, triggering a double-top short-sale (DTSS) entry at the 455.50 left-side peak last week. It has continued to decline and now sits below the lows of its prior base from which it broke out two weeks ago.The culprit behind the sell-off? Alphabet’s (GOOGL) new TurboQuant technology, which is “a compression algorithm developed by Google researchers that significantly reduces the working memory (e.g., for activations and KV cache in inference) required to run large language models (LLMs) and vector search engines—by a factor of at least six—without sacrificing performance or requiring model retraining. It improves efficiency in AI systems, making inference up to 8x faster in some cases while using far less memory.”

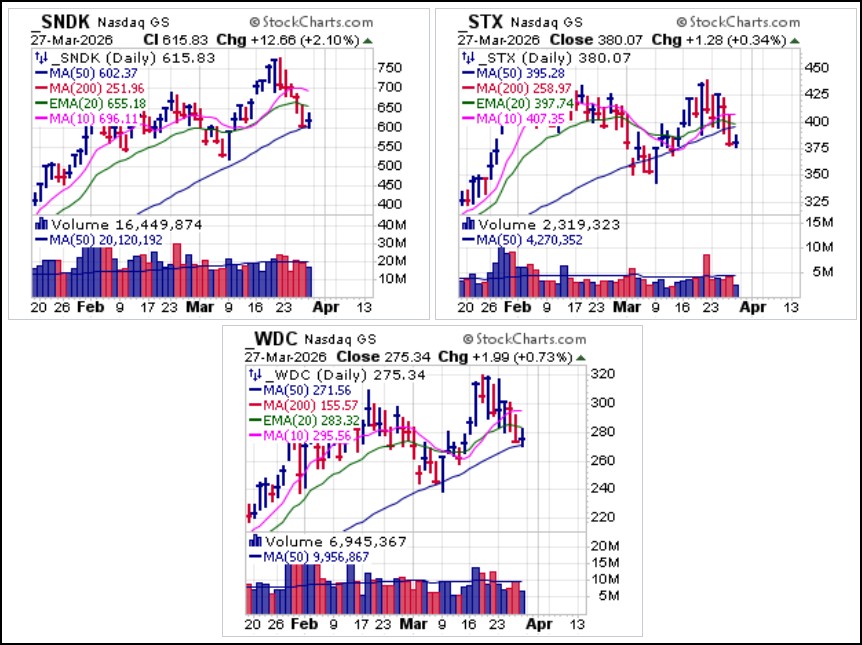

This news also affected fellow memory chip leader Western Digital Corp. (WDC), along with storage names SanDisk (SNDK) and Seagate Technologies (STX), all recent leaders that have otherwise stood out from the rest of the pack in the semiconductor sector. All three stocks triggered short-sale entries at their 20-demas on Thursday with STX triggering a second short entry on the same day as it broke 50-dma support. It now sits 3.8% below the line, so that any rallies up closer to the 50-day could bring it back into short-sale range so can be watched for. SNDK and WDC held up at 50-dma support on Friday, but should be watched for any shortable rallies into 20-dema support or any breaks below the 50-day line as this would trigger fresh short-sale entries if they occur.

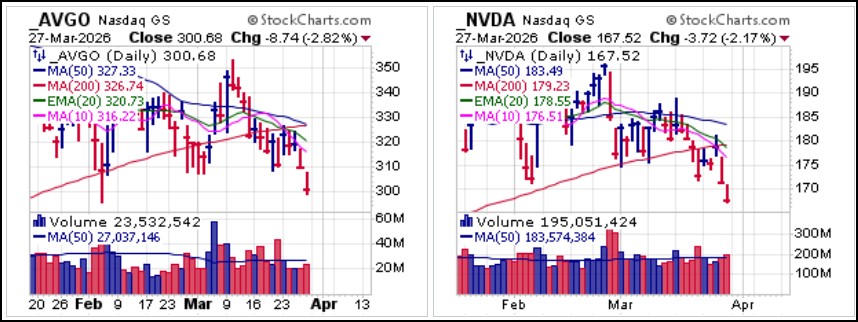

This news also affected fellow memory chip leader Western Digital Corp. (WDC), along with storage names SanDisk (SNDK) and Seagate Technologies (STX), all recent leaders that have otherwise stood out from the rest of the pack in the semiconductor sector. All three stocks triggered short-sale entries at their 20-demas on Thursday with STX triggering a second short entry on the same day as it broke 50-dma support. It now sits 3.8% below the line, so that any rallies up closer to the 50-day could bring it back into short-sale range so can be watched for. SNDK and WDC held up at 50-dma support on Friday, but should be watched for any shortable rallies into 20-dema support or any breaks below the 50-day line as this would trigger fresh short-sale entries if they occur.  Broadcom (AVGO) and Nvidia (NVDA) also continue to suffer as both stocks were short-sale entries at 200-dma resistance earlier in the week before breaking to lower lows on Friday.

Broadcom (AVGO) and Nvidia (NVDA) also continue to suffer as both stocks were short-sale entries at 200-dma resistance earlier in the week before breaking to lower lows on Friday. The need for fewer memory chips as a result of TurboQuant also negatively impacted semiconductor equipment makers Applied Materials (AMAT), ASML Holdings (ASML), KLA Corp. (KLAC) and Lam Research (LRCX). Fewer chips require fewer manufacturing equipment to make them, and so down these stocks went following the TurboQuant news. Among these, AMAT and KLAC are nearest to the undersides of their 50-day moving averages so can be watched for any shortable rallies back up into resistance at the 50-day.

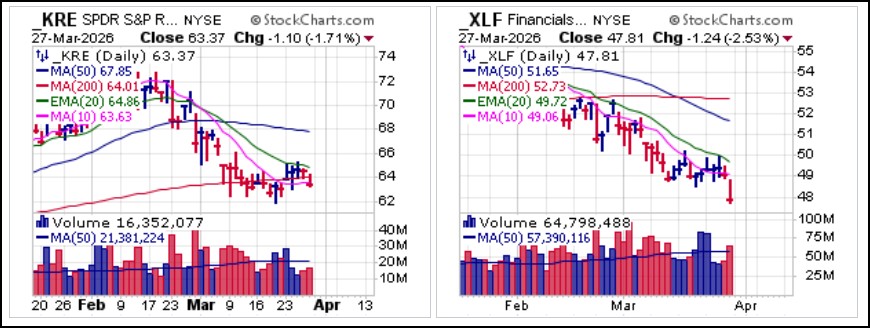

The need for fewer memory chips as a result of TurboQuant also negatively impacted semiconductor equipment makers Applied Materials (AMAT), ASML Holdings (ASML), KLA Corp. (KLAC) and Lam Research (LRCX). Fewer chips require fewer manufacturing equipment to make them, and so down these stocks went following the TurboQuant news. Among these, AMAT and KLAC are nearest to the undersides of their 50-day moving averages so can be watched for any shortable rallies back up into resistance at the 50-day. Financials remain an area of bearish concern for the market as they often signal potential issues with the broader financial system. The SPDR Regional Banking (KRE) and SPDR Select Sector Financials (XLF) ETFs both broke to the downside on Friday. The KRE posted a fresh short-sale entry as it breached 200-dma support while the XLF continues to cascade to lower lows.

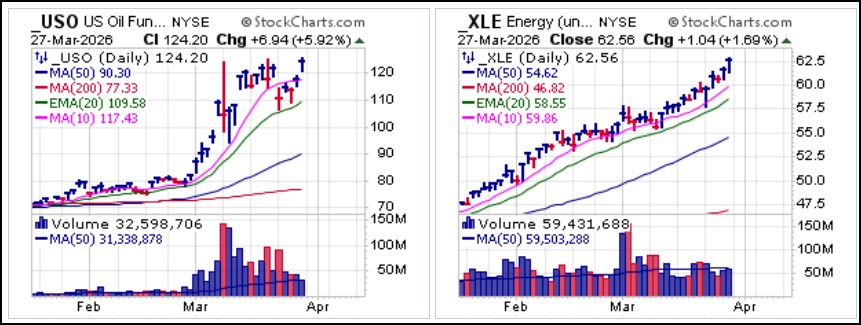

Financials remain an area of bearish concern for the market as they often signal potential issues with the broader financial system. The SPDR Regional Banking (KRE) and SPDR Select Sector Financials (XLF) ETFs both broke to the downside on Friday. The KRE posted a fresh short-sale entry as it breached 200-dma support while the XLF continues to cascade to lower lows. The lone wolf, or rather lone bull, in this market remains the oil patch as oil prices surge back above $100 a barrel. This sent the United States Oil Fund (USO) on a breakout from a three-week flag formation while the SPDR Select Sector Energy (XLE) ETF continues to trend higher and well above its rising 10-dma. As with the bearish side of the current market environment, this sector remains highly news-sensitive as any positive news out of the Middle East and the Iran War could send oil prices and the oil patch plummeting. Such extreme news dependency makes this a potentially treacherous market for the long or short side, and thus is only suitable to nimble short-term traders. Otherwise, cash remains king until further notice.

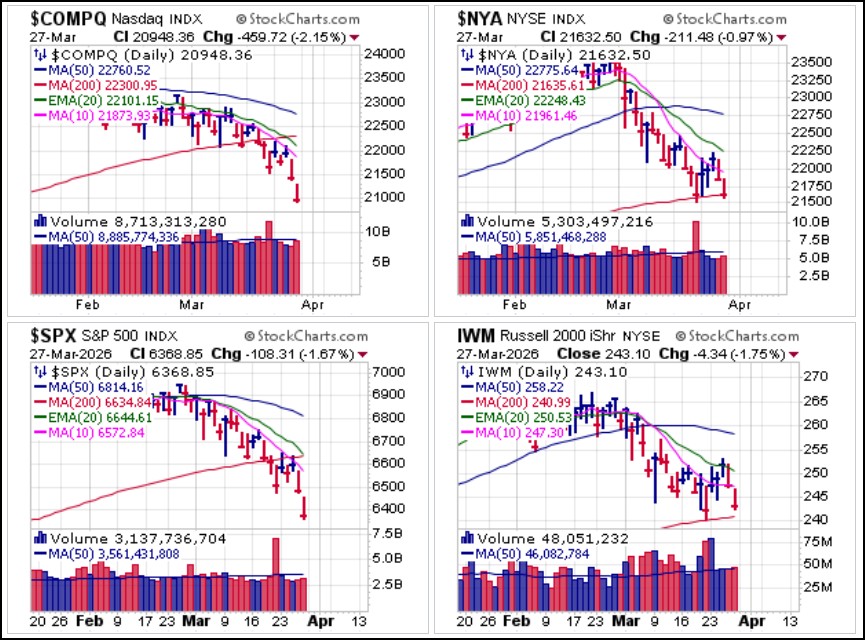

The lone wolf, or rather lone bull, in this market remains the oil patch as oil prices surge back above $100 a barrel. This sent the United States Oil Fund (USO) on a breakout from a three-week flag formation while the SPDR Select Sector Energy (XLE) ETF continues to trend higher and well above its rising 10-dma. As with the bearish side of the current market environment, this sector remains highly news-sensitive as any positive news out of the Middle East and the Iran War could send oil prices and the oil patch plummeting. Such extreme news dependency makes this a potentially treacherous market for the long or short side, and thus is only suitable to nimble short-term traders. Otherwise, cash remains king until further notice. The Market Direction Model remains on a SELL signal since it last switched on February 27th, well before the current market correction gathered its current downside momentum.

The Market Direction Model remains on a SELL signal since it last switched on February 27th, well before the current market correction gathered its current downside momentum.