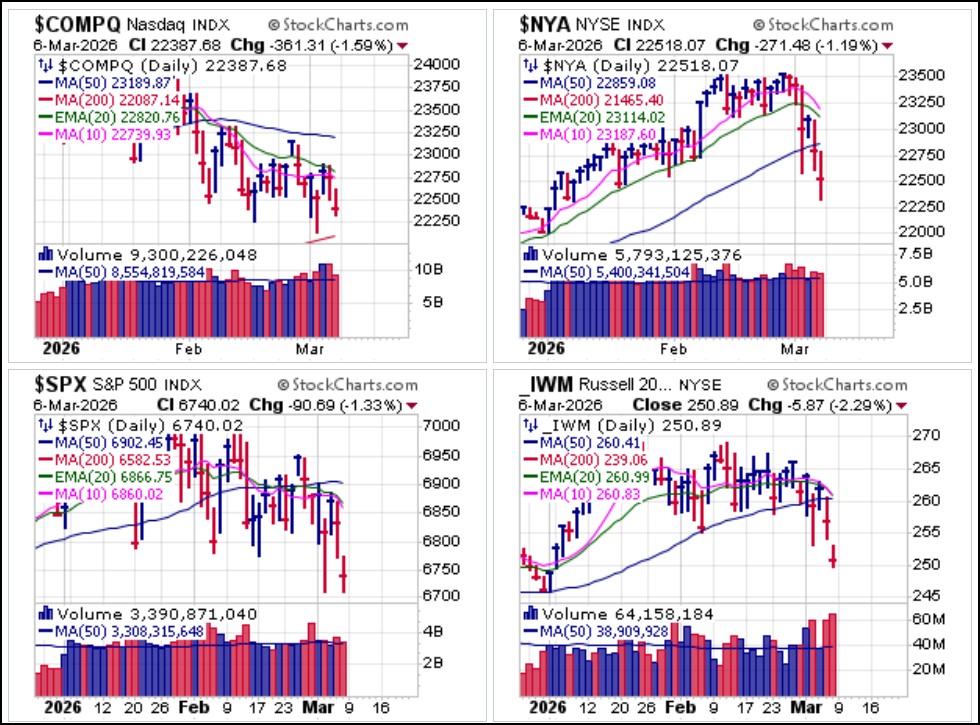

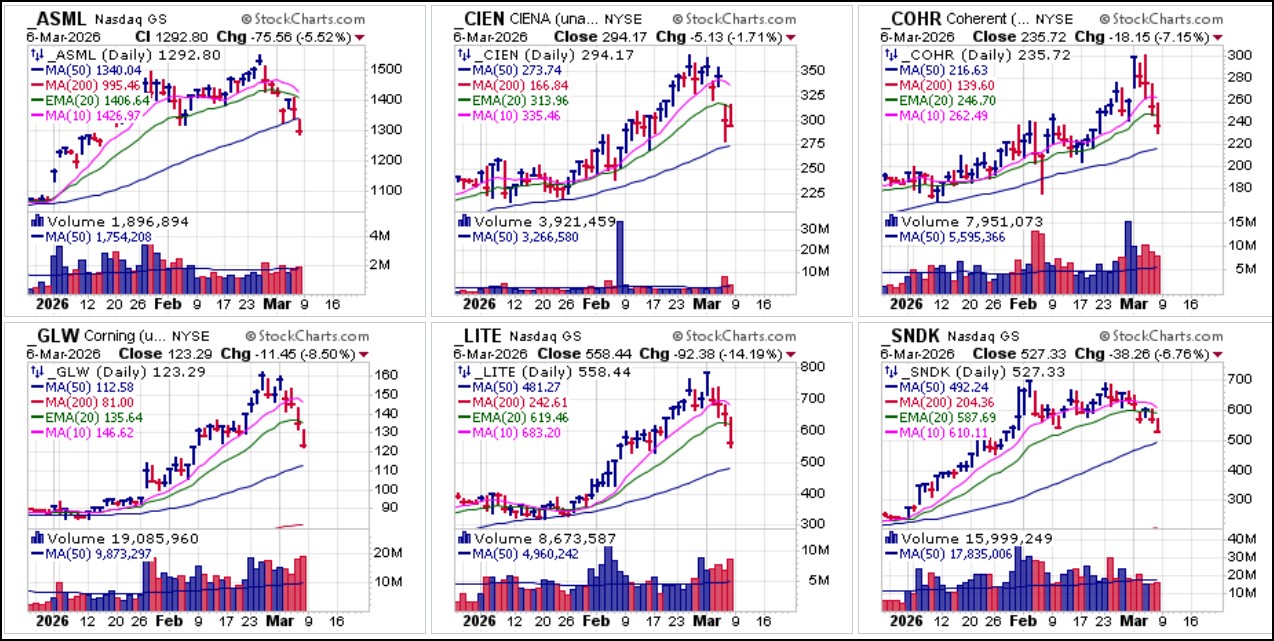

Most, if not all, of the last remaining AI leaders that were holding up well, including selected semiconductor equipment and memory makers and AI data center-related telecoms all came loose this past week after many posted new highs over the past 1-2 weeks.

Most, if not all, of the last remaining AI leaders that were holding up well, including selected semiconductor equipment and memory makers and AI data center-related telecoms all came loose this past week after many posted new highs over the past 1-2 weeks. Even precious metals, which one might expect to rally in the face of war, are suffering from forced selling as the market continues lower. Both the SPDR Gold Trust (GLD) and the iShares Silver Trust (SLV) stabilized after breaking to the downside earlier in the week. However, it the general market situation continues to worsen, triggering margin calls and necessitating institutional reliquification, anything that is not nailed down has the potential to be sold as a fungible source of cash.

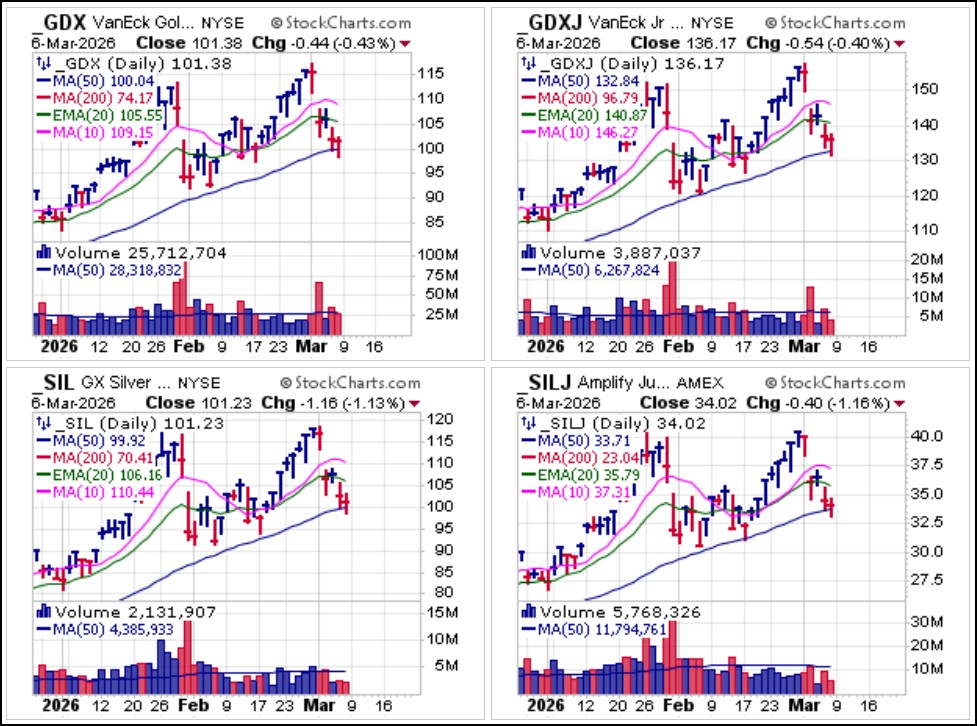

Even precious metals, which one might expect to rally in the face of war, are suffering from forced selling as the market continues lower. Both the SPDR Gold Trust (GLD) and the iShares Silver Trust (SLV) stabilized after breaking to the downside earlier in the week. However, it the general market situation continues to worsen, triggering margin calls and necessitating institutional reliquification, anything that is not nailed down has the potential to be sold as a fungible source of cash. Mining stocks, which were leading the market into last week as many pushed to higher highs have most certainly succumbed to forced selling. Gold prices over $5,000 and silver prices over $80 an ounce will still result in major earnings increases for the miners, but forced selling will drag them lower. There is also the potential for the war in Iran to impact production costs along with higher overall inflation which has recently reared its head once again. The four primary mining ETFs, the VanEck Gold Miners (GDX), the VanEck Junior Gold Miners (GDXJ), the Global X Silver Miners (SIL) and the Amplify Junior Silver Miners (SILJ) ETFs all posted MAU&Rs at 50-dma support on Monday but it is not clear whether they will be able to hold in the face of more general market selling.

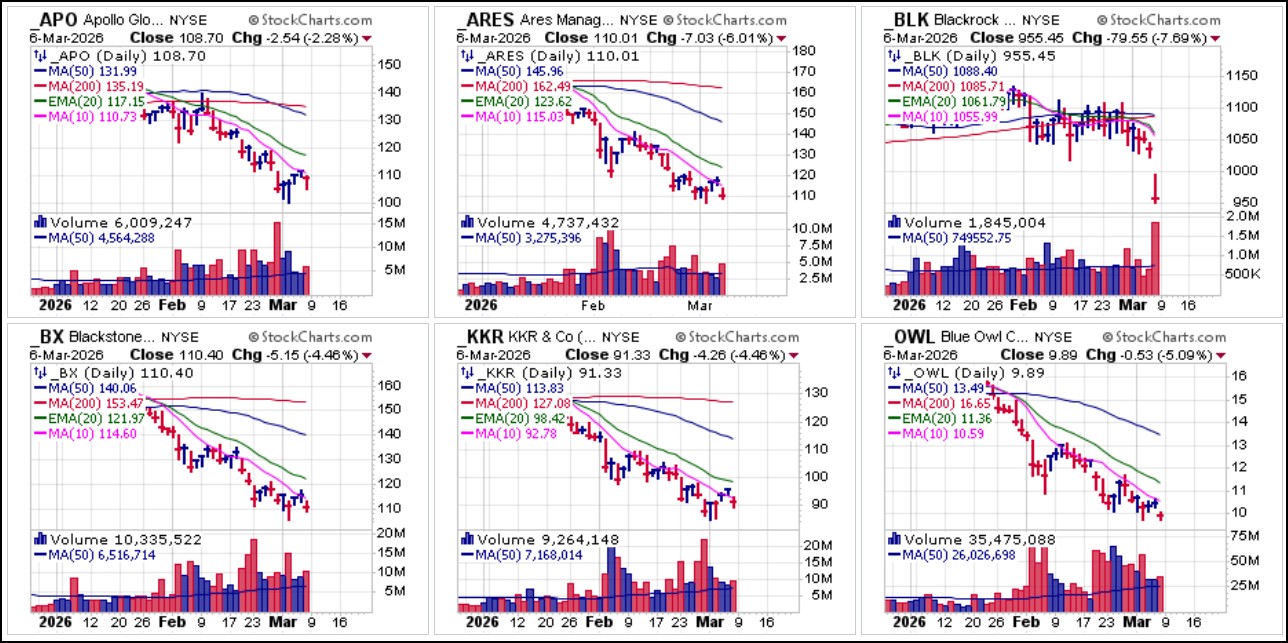

Mining stocks, which were leading the market into last week as many pushed to higher highs have most certainly succumbed to forced selling. Gold prices over $5,000 and silver prices over $80 an ounce will still result in major earnings increases for the miners, but forced selling will drag them lower. There is also the potential for the war in Iran to impact production costs along with higher overall inflation which has recently reared its head once again. The four primary mining ETFs, the VanEck Gold Miners (GDX), the VanEck Junior Gold Miners (GDXJ), the Global X Silver Miners (SIL) and the Amplify Junior Silver Miners (SILJ) ETFs all posted MAU&Rs at 50-dma support on Monday but it is not clear whether they will be able to hold in the face of more general market selling. On Friday, big-stock asset manager Blackrock (BLK) gapped lower and declined over 7% after announcing that its flagship private credit firm, HPS Corporate Lending Fund, is now limiting investor withdrawals. This comes in the wake of other redemption bans from Blackstone Group (BX) and Blue Owl Capital (OWL). These three names and other related private credit issuers shown in the group chart below all topped in early January and have all steadily trended lower in what has been an ongoing private credit train wreck in progress.

On Friday, big-stock asset manager Blackrock (BLK) gapped lower and declined over 7% after announcing that its flagship private credit firm, HPS Corporate Lending Fund, is now limiting investor withdrawals. This comes in the wake of other redemption bans from Blackstone Group (BX) and Blue Owl Capital (OWL). These three names and other related private credit issuers shown in the group chart below all topped in early January and have all steadily trended lower in what has been an ongoing private credit train wreck in progress. As we see it, there are a multitude of negatives, both well-established and newly-emerging, that may keep the pressure up on stocks until they are resolved. The Fed also may soon be forced to act, but it may be too little too late in the face of a tidal wave of negative developments currently besetting the market. An AI-generated list of these woes below:

As we see it, there are a multitude of negatives, both well-established and newly-emerging, that may keep the pressure up on stocks until they are resolved. The Fed also may soon be forced to act, but it may be too little too late in the face of a tidal wave of negative developments currently besetting the market. An AI-generated list of these woes below:- Geopolitical Conflicts and Wars: Escalating tensions, particularly the U.S.-Iran war, along with related issues in the Middle East (e.g., Strait of Hormuz disruptions) and Afghanistan-Pakistan relations, are heightening investor anxiety. These conflicts could expand, leading to broader instability and military interventions abroad, which are seen as mounting political risks.

- Rising Oil Prices and Energy Risks: Oil has spiked above $90 per barrel, potentially heading toward $100, due to geopolitical disruptions in supply routes. This increases costs for airlines, travel, and manufacturing sectors, while fueling broader inflation pressures and economic uncertainty.

- Higher and Sticky Inflation: Inflation remains elevated and broad-based, closer to 3% than the Fed's 2% target, with risks skewed upward due to tariffs, oil shocks, health insurance, and electricity price hikes. Recent hot inflation prints and potential stagflation (high inflation with stagnant growth) are major concerns, limiting the Fed's ability to ease rates.

- Weak Labor Market and Unemployment: Unemployment has risen to 4.4%, with negative payroll numbers, widespread job cuts (e.g., Block reducing its workforce by 40%), and a "low-hire, low-fire" environment signaling slowdown. This could morph into a sharp recession, eroding consumer confidence and spending.

- Recession and Economic Slowdown Fears: There's a 35% probability of a U.S. and global recession in 2026, driven by weak business sentiment, tepid growth, and declining consumer spending. Affordability crises, weaker GDP, and a potential sharp rise in unemployment add to the instability. Countering this is global liquidity, AI productivity gains, and potentially lower rates due to the $8-9 T rollover later this year.

- Private Credit and Credit Market Fears: Red flags include loose underwriting standards, write-downs, fraud, and rising defaults (e.g., the Blue Owl Capital (OWL) situation), squeezing borrowers in tech/AI and other sectors. Credit issues could be more widespread than in 2008, with leverage risks amplifying downturns. Tech credit spreads are widening amid refinancing challenges.

- High Valuations and Bubble Risks: The CAPE ratio is near 39-40, the highest since the dot-com era, signaling overstretched P/Es and limited upside with increased downside potential. The equity risk premium is now negative, offering zero risk-adjusted returns. Parabolic sectors like AI are at risk of correction.

- Tech/AI Sector Concentration and Disruption: Heavy reliance on a few mega-caps, with AI capex far ahead of monetization and profit pools, is cracking under scrutiny. Ongoing bubble debates, regulatory crackdowns (e.g., on Anthropic for military access), and disruption fears are driving volatility and sector rotations away from tech. Legal issues like the OpenAI vs. Elon Musk trial add uncertainty.

- Fiscal Debt and Government Bond Turbulence: Unsustainable U.S. deficits (7-8% of GDP) and rising debt-to-GDP ratios lack a credible stabilization plan, risking ripples through markets and higher interest rates demanded by foreign holders.

We reiterate: unless one is skilled in short-selling and able to maintain a nimble approach to what is a very volatile market environment, cash remains king.

The Market Direction Model (MDM) remains on a SELL signal.