We can surmise that the market expects that the Iran War is close to ending as the U.S. blockade of Iranian shipping theoretically strips Iran of any leverage it exerts through controlling the Strait of Hormuz. The evidence is shown not only on the wild rally seen in the indexes since the late March/early April lows but also in the action of various defense stocks. If war is big business for defense companies, it does not appear to be apparent on these charts. General Dynamics (GD), however, finally bucked the trend on Wednesday when it posted a bottom-fishing buyable gap-up (BFBGU) after reporting 12% earnings growth. While the move stalled at the 200-dma on Wednesday the stock continued to push higher, ending the week back above the 50-dma. As other defense names start to report, we may gain better insight into just how, if at all, the Iran War benefits their earnings profile.

We can surmise that the market expects that the Iran War is close to ending as the U.S. blockade of Iranian shipping theoretically strips Iran of any leverage it exerts through controlling the Strait of Hormuz. The evidence is shown not only on the wild rally seen in the indexes since the late March/early April lows but also in the action of various defense stocks. If war is big business for defense companies, it does not appear to be apparent on these charts. General Dynamics (GD), however, finally bucked the trend on Wednesday when it posted a bottom-fishing buyable gap-up (BFBGU) after reporting 12% earnings growth. While the move stalled at the 200-dma on Wednesday the stock continued to push higher, ending the week back above the 50-dma. As other defense names start to report, we may gain better insight into just how, if at all, the Iran War benefits their earnings profile. This market remains all about the semiconductor space as these names continue to shrug off pullback after pullback. Even SanDisk (SNDK), which was hit in the after-hours on Thursday, shrugged off an overnight sell-off down towards the $1000 Millennial Mark where it found support and then turned back to the upside to post yet another new all-time high. Seagate Technology (STX) reported earnings Tuesday after the close and posted a buyable gap-up on Wednesday. On Friday it streaked through the $700 Century Mark to post a Livermore Century Mark long entry. Western Digital (WDC) reported on Thursday night with SNDK and rallied back from an early sell-off as it found support at the 10-dma and the $400 Century Mark. The stock bounced well enough to close relatively unchanged, down -0.69% on the day.

This market remains all about the semiconductor space as these names continue to shrug off pullback after pullback. Even SanDisk (SNDK), which was hit in the after-hours on Thursday, shrugged off an overnight sell-off down towards the $1000 Millennial Mark where it found support and then turned back to the upside to post yet another new all-time high. Seagate Technology (STX) reported earnings Tuesday after the close and posted a buyable gap-up on Wednesday. On Friday it streaked through the $700 Century Mark to post a Livermore Century Mark long entry. Western Digital (WDC) reported on Thursday night with SNDK and rallied back from an early sell-off as it found support at the 10-dma and the $400 Century Mark. The stock bounced well enough to close relatively unchanged, down -0.69% on the day. Other semiconductors that we have reported on have presented something of a mixed bag. Micron Technology (MU) remains relatively robust after clearing the $500 Century Mark earlier in the week and then holding support there on Friday before launching to a new all-time high. Nvidia (NVDA) is failing on a recent small flag breakout and pocket pivot at the 10-dma. It in fact triggered an aggressive short-sale entry at the 10-dma before dipping just below the $200 Century Mark before holding at 20-dema support on Friday. Taiwan Semiconductor (TSM), which had posted a BGU after earnings the prior week immediately failed at the $400 Century Mark and on Friday edged up to that price level before closing at 397.67. If it can regain the $400 level it would trigger a second Century Mark long entry, otherwise it could play out as a short entry if the $400 level serves as key price resistance.

Other semiconductors that we have reported on have presented something of a mixed bag. Micron Technology (MU) remains relatively robust after clearing the $500 Century Mark earlier in the week and then holding support there on Friday before launching to a new all-time high. Nvidia (NVDA) is failing on a recent small flag breakout and pocket pivot at the 10-dma. It in fact triggered an aggressive short-sale entry at the 10-dma before dipping just below the $200 Century Mark before holding at 20-dema support on Friday. Taiwan Semiconductor (TSM), which had posted a BGU after earnings the prior week immediately failed at the $400 Century Mark and on Friday edged up to that price level before closing at 397.67. If it can regain the $400 level it would trigger a second Century Mark long entry, otherwise it could play out as a short entry if the $400 level serves as key price resistance. Semiconductors Applied Materials (AMAT) and Advanced Micro Devices (AMD), both of which we have reported on previously also present a mixed bag. AMAT reversed at its 10-dma and resistance at the $400 Century Mark after peaking at 398.64 on Friday. That set up a short entry using the $400 level as a selling guide. AMD, which posted a very extended BGU type of move last Friday in sympathy to Intel (INTC) earnings, immediately failed but found support at the 10-dma before rising to new highs on Friday as volume declines. AMD is expected to report earnings this week, which in turn may have a significant effect on the semiconductor space, one way or another. For this reason it will be one to watch this week.

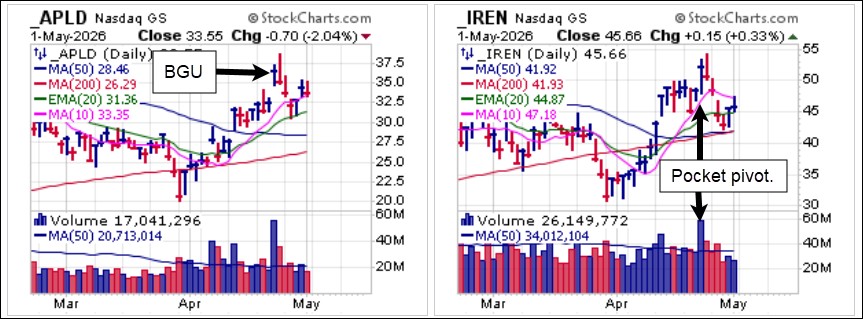

Semiconductors Applied Materials (AMAT) and Advanced Micro Devices (AMD), both of which we have reported on previously also present a mixed bag. AMAT reversed at its 10-dma and resistance at the $400 Century Mark after peaking at 398.64 on Friday. That set up a short entry using the $400 level as a selling guide. AMD, which posted a very extended BGU type of move last Friday in sympathy to Intel (INTC) earnings, immediately failed but found support at the 10-dma before rising to new highs on Friday as volume declines. AMD is expected to report earnings this week, which in turn may have a significant effect on the semiconductor space, one way or another. For this reason it will be one to watch this week. Other techs we have reported on have fared less well, but likely because they are AI Data Center related names and not semiconductors per se. Applied Digital (APLD) failed badly after posting a BGU two Thursdays ago while IREN Ltd. (IREN) quickly failed after posting what was an impressive, big-volume pocket pivot before triggering an aggressive short entry at the 10-dma this past Monday. IREN is expected to report earnings Thursday after the close.

Other techs we have reported on have fared less well, but likely because they are AI Data Center related names and not semiconductors per se. Applied Digital (APLD) failed badly after posting a BGU two Thursdays ago while IREN Ltd. (IREN) quickly failed after posting what was an impressive, big-volume pocket pivot before triggering an aggressive short entry at the 10-dma this past Monday. IREN is expected to report earnings Thursday after the close.Data center stocks such as APLD and IREN can absolutely trend higher over the next 12–24 months, but expect a slower, more volatile grind driven by actual GPU deployments and revenue ramps rather than the same near-vertical 2025-style moves. The next catalyst is Q3 FY26 earnings on May 7, 2026 — strong execution there could restart upward momentum, but any slippage on timelines would likely cause more downside pressure.

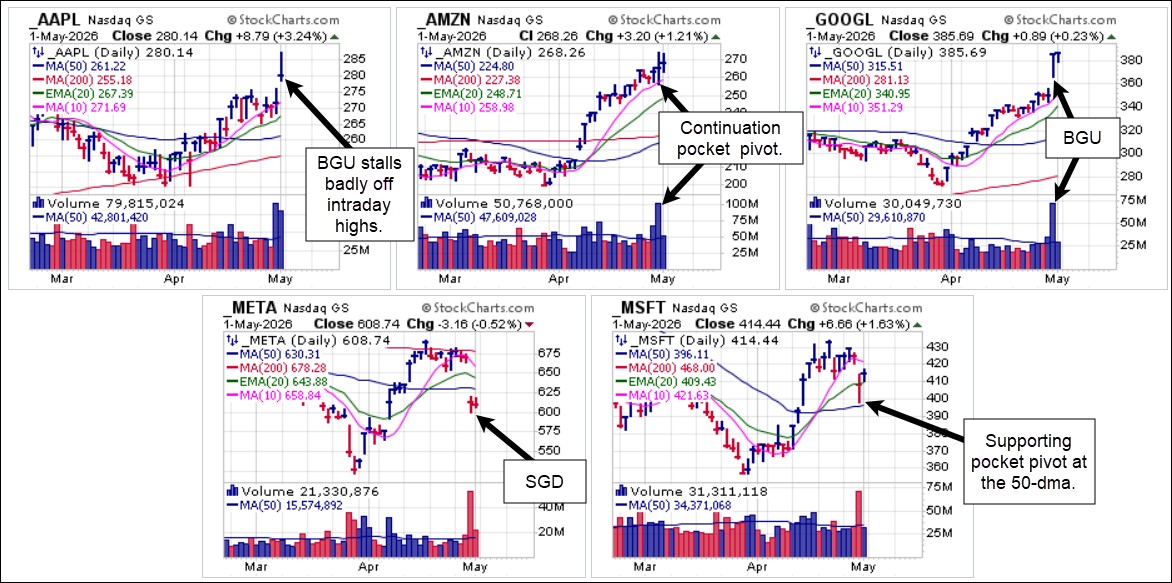

This past week was also interesting in that we saw for the first time in a while four big-stock NASDAQ names report on a single day. Amazon.com (AMZN), Alphabet (GOOGL), Meta Platforms (META) and Microsoft (MSFT) all reported earnings on Wednesday with mixed results. AMZN posted a continuation pocket pivot at the 10-dma while GOOGL posted a BGU with an intraday low of 365.82. Apple (AAPL) reported on Thursday evening and gapped up Friday in a big stalling BGU move. This looks bearish on its face, but if it holds the intraday low at 278.37 the BGU would remain in force.

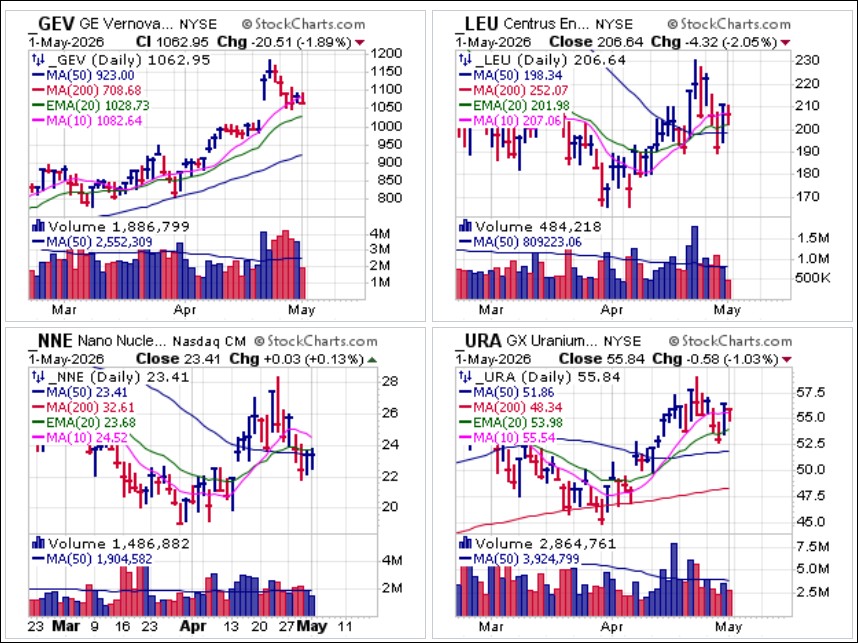

This past week was also interesting in that we saw for the first time in a while four big-stock NASDAQ names report on a single day. Amazon.com (AMZN), Alphabet (GOOGL), Meta Platforms (META) and Microsoft (MSFT) all reported earnings on Wednesday with mixed results. AMZN posted a continuation pocket pivot at the 10-dma while GOOGL posted a BGU with an intraday low of 365.82. Apple (AAPL) reported on Thursday evening and gapped up Friday in a big stalling BGU move. This looks bearish on its face, but if it holds the intraday low at 278.37 the BGU would remain in force. Other non-tech names that we have reported on recently have only served to confirm that this market is all about one group, and one group only, semiconductors. Nuclear power related names reported on over a week ago have all demonstrated little inclination to move higher. GE Vernova (GEV), which builds nuclear reactors, is failing on a prior post-earnings BGU attempt as it now wavers at 10-dma support. Small modular reactor maker Nano Nuclear Energy (NNE) has now failed back below 50-dma support where it starts to look more like a short entry. Uranium refiner Centrus Energy (LEU) is wobbling along 50-dma support although could be treated as an MAU&R following Thursday's recover at the 50-dma which is then used as a tight selling guide. It is expected to report earnings Tuesday after the close. Meanwhile, the Global X Uranium Miners (URA) ETF is meandering between 10-dma resistance and 20-dema support.

Other non-tech names that we have reported on recently have only served to confirm that this market is all about one group, and one group only, semiconductors. Nuclear power related names reported on over a week ago have all demonstrated little inclination to move higher. GE Vernova (GEV), which builds nuclear reactors, is failing on a prior post-earnings BGU attempt as it now wavers at 10-dma support. Small modular reactor maker Nano Nuclear Energy (NNE) has now failed back below 50-dma support where it starts to look more like a short entry. Uranium refiner Centrus Energy (LEU) is wobbling along 50-dma support although could be treated as an MAU&R following Thursday's recover at the 50-dma which is then used as a tight selling guide. It is expected to report earnings Tuesday after the close. Meanwhile, the Global X Uranium Miners (URA) ETF is meandering between 10-dma resistance and 20-dema support.### Why Higher Uranium Prices Are Likely

- **Structural supply deficit**: Uranium production has lagged while demand is accelerating from nuclear restarts, new reactor builds, and surging electricity needs (especially AI data centers). Many analysts see the deficit widening into the late 2020s.

- **Policy & energy security tailwinds**: Governments worldwide are supporting nuclear as clean, reliable baseload power. This includes potential U.S. strategic reserves and life extensions/restarts.

- **Price momentum**: Spot prices have been firm, with forecasts for sustained strength or upside as utilities return to long-term contracting.

### Risks & Realism on Uranium

- **Near-term volatility**: Bottlenecks in power, permitting, and infrastructure could slow rollout and cause pullbacks (as seen in some 2026 reactions). The sector is sentiment-driven and can overshoot on hype.

- **Not guaranteed**: If economic slowdown reduces energy demand or new supply comes online faster than expected, upside could be capped.

- **Timing**: The strongest moves often come when contracting accelerates and inventories tighten — analysts point to 2026–2027 as a key window.

Unless you are playing semiconductor stocks in this market you are having a difficult time making money. If you are, however, then you are experiencing a rush of parabolic upside reminiscent of the DotCom price action seen in late 1999 and early 2000. What makes this run in semis quite different is that the stocks actually have real products with real earnings and sales. At some point, parabolic moves either climax top or go into necessary consolidations of some duration, but as of yet most semiconductors show little inclination to do so as we move into the new trading month.

Unless you are playing semiconductor stocks in this market you are having a difficult time making money. If you are, however, then you are experiencing a rush of parabolic upside reminiscent of the DotCom price action seen in late 1999 and early 2000. What makes this run in semis quite different is that the stocks actually have real products with real earnings and sales. At some point, parabolic moves either climax top or go into necessary consolidations of some duration, but as of yet most semiconductors show little inclination to do so as we move into the new trading month.The Market Direction Model (MDM) remains on a BUY signal.