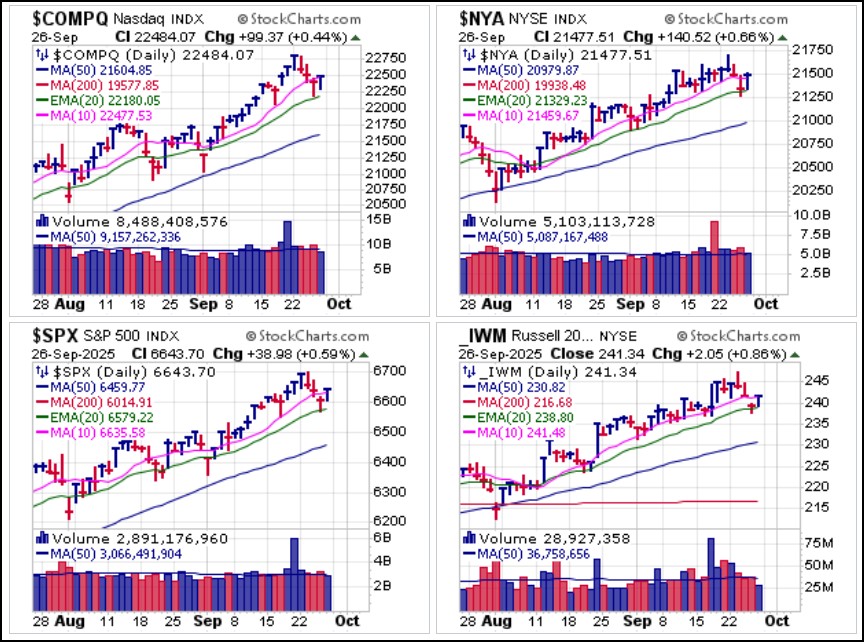

Major market indexes started the week off with news highs in the NASDAQ Composite, NYSE Composite, S&P 500, and Russell 2000 before a 2-3 day sell-off ensued over the middle three days of the week. The S&P 500 held out on the upside on Tuesday before getting dragged down into a two-day sell-off as the other three indexes posted three-day sell-offs. While the indexes closed down on Thursday, they found meaningful intraday support at their 20-demas before rallying back above 10-dma support on Friday. Only the Russell 2000, via the iShares Russell 2000 (IWM) ETF fell short of what remains 10-dma resistance.

While the Fed rate cut last week has kept the Three-Month Treasury Yield ($IRX) within a 3.8% to 3.9% range, the Ten-Year Treasury Yield ($TNX) continues to rise off the lows posted when the Fed policy announcement was made two Wednesdays, or eight trading days, ago. So, while the Trumpkins got what they wanted with the latest 1/4% rate cut from the Fed, it did not produce the desired effect of lowering credit costs.

While the Fed rate cut last week has kept the Three-Month Treasury Yield ($IRX) within a 3.8% to 3.9% range, the Ten-Year Treasury Yield ($TNX) continues to rise off the lows posted when the Fed policy announcement was made two Wednesdays, or eight trading days, ago. So, while the Trumpkins got what they wanted with the latest 1/4% rate cut from the Fed, it did not produce the desired effect of lowering credit costs. It is important to understand that mortgage rates are benchmarked to the $TNX, which is rising. This has sent homebuilding stocks careening lower after peaking three weeks ago. The SPDR S&P Homebuilders (XHB) ETF illustrates a steady downtrend that finally pierced 50-dma support on Wednesday. Given the expectations of a 1/4% rate cut from the Fed, the homebuilders were already showing signs of weakness as the market sorted out exactly what a 1/4% rate cut would mean for the housing sector.

It is important to understand that mortgage rates are benchmarked to the $TNX, which is rising. This has sent homebuilding stocks careening lower after peaking three weeks ago. The SPDR S&P Homebuilders (XHB) ETF illustrates a steady downtrend that finally pierced 50-dma support on Wednesday. Given the expectations of a 1/4% rate cut from the Fed, the homebuilders were already showing signs of weakness as the market sorted out exactly what a 1/4% rate cut would mean for the housing sector. One of the big stories of the week has been silver, where COMEX Silver Futures hit a new 14-year high, ending the week at $46.36 an ounce. Spot Silver closed the week at 46.04. Since silver cleared the $40 level in early September, the $50 level has acted like a magnet, seemingly pulling the white metal higher. We reported on silver and the iShares Silver Trust (SLV) in late August as it was starting to emerge from a five-week base. We would not be surprised to see silver hit $50.00 an ounce given the current trend. Silver is also under consideration for inclusion on the Strategic Metals list

One of the big stories of the week has been silver, where COMEX Silver Futures hit a new 14-year high, ending the week at $46.36 an ounce. Spot Silver closed the week at 46.04. Since silver cleared the $40 level in early September, the $50 level has acted like a magnet, seemingly pulling the white metal higher. We reported on silver and the iShares Silver Trust (SLV) in late August as it was starting to emerge from a five-week base. We would not be surprised to see silver hit $50.00 an ounce given the current trend. Silver is also under consideration for inclusion on the Strategic Metals list Gold posted all-time highs on Tuesday as Spot Gold hit $3,791.09 an ounce on Tuesday before closing at $3,754.06 on Friday. COMEX Gold Futures printed $3,824.60 an ounce before settling in to end the week at $3,789.80. This keeps gold in a short four-week bull flag as it continues to follow the 10-day moving average since breaking out in late August.

Gold posted all-time highs on Tuesday as Spot Gold hit $3,791.09 an ounce on Tuesday before closing at $3,754.06 on Friday. COMEX Gold Futures printed $3,824.60 an ounce before settling in to end the week at $3,789.80. This keeps gold in a short four-week bull flag as it continues to follow the 10-day moving average since breaking out in late August. Bitcoin ($BTCUSD) triggered a short-sale entry at the 50-dma last week, and after a brief rally back into 50-dma resistance it has broken lower again. It is now testing the early September low as it starts to outline a potential "pinhead & shoulders" type of formation. A test of the neckling of this H&S variant would potentially take $BTCUSD down to the 200-dma.

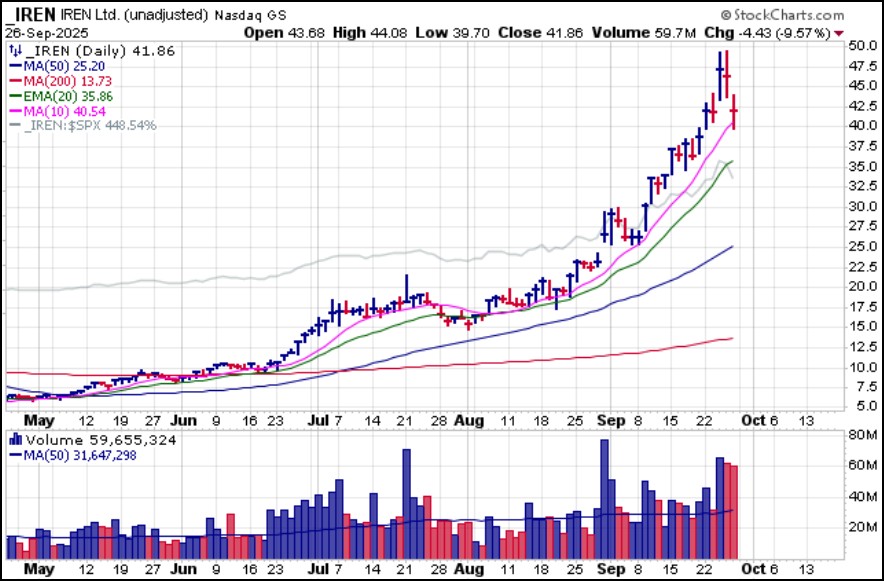

Bitcoin ($BTCUSD) triggered a short-sale entry at the 50-dma last week, and after a brief rally back into 50-dma resistance it has broken lower again. It is now testing the early September low as it starts to outline a potential "pinhead & shoulders" type of formation. A test of the neckling of this H&S variant would potentially take $BTCUSD down to the 200-dma. IREN Ltd. (IREN), which recently shifted its business focus from crypto mining to data center power and infrastructure was by far our best-performing long stock idea. We first reported on the stock on June 8th as a pocket pivot in our Weekend Review, formerly known as the Focus List Review, when it was trading at around $11. In three months it has gone up more than four-fold. As we noted last weekend, IREN has obeyed the 10-week line now for the past seven weeks, so one can implement the Seven-Week Rule and use a violation of the 10-week line as a selling guide.

IREN Ltd. (IREN), which recently shifted its business focus from crypto mining to data center power and infrastructure was by far our best-performing long stock idea. We first reported on the stock on June 8th as a pocket pivot in our Weekend Review, formerly known as the Focus List Review, when it was trading at around $11. In three months it has gone up more than four-fold. As we noted last weekend, IREN has obeyed the 10-week line now for the past seven weeks, so one can implement the Seven-Week Rule and use a violation of the 10-week line as a selling guide. At this stage of the market cycle, finding fresh, new long set-ups that are not extended, at least where they have worked on the upside, is becoming more difficult. So, staying with what continues to hold its uptrend while it does and sitting tight until trailing stops are hit is the prudent approach until we see some new merchandise appear on the horizon.

At this stage of the market cycle, finding fresh, new long set-ups that are not extended, at least where they have worked on the upside, is becoming more difficult. So, staying with what continues to hold its uptrend while it does and sitting tight until trailing stops are hit is the prudent approach until we see some new merchandise appear on the horizon.The Market Direction Model remains on a BUY signal.