Friday's jobs number, which showed only 22,000 new nonfarm payrolls vs. estimates of 75,000 as well as a revision to June numbers that set the latest number at -13,000, initially wowed investors as the markets started the day to the upside. The initial wow factor resulted from the idea that such weak jobs numbers made a 50 basis point rate cut from the Fed a veritable slam-dunk. The NASDAQ Composite, NASDAQ 100, NYSE Composite, and S&P 500 Indexes all started the morning off at fresh all-time highs.

However the other side of the weak jobs = Fed rate cut equation is the fact that rapidly weakening employment is symptomatic of economic malaise. The -13,000 revision to the June number was the first such revision into negative territory since December 2007. JOLTS data released earlier in the week also showed there are now more unemployed than there are job openings for the first time since the Covid Panic of 2020 show that the Fed's fears of weakening employment. It all combined to confirm the Fed's fear of weakening employment as expressed by Head Fedhead Jerome Powell during his Jackson Hole speech two weeks ago.

Eventually, that seeped into the market's consciousness and the indexes soon reversed to close down on the day across the board. This resulted, at least for the moment, in double-top type action in all four of those indexes as represented by the daily chart of the NASDAQ Composite, below. For now, the indexes are clinging to 10-dma support as the underlying situation with respect to individual stocks remains mixed.

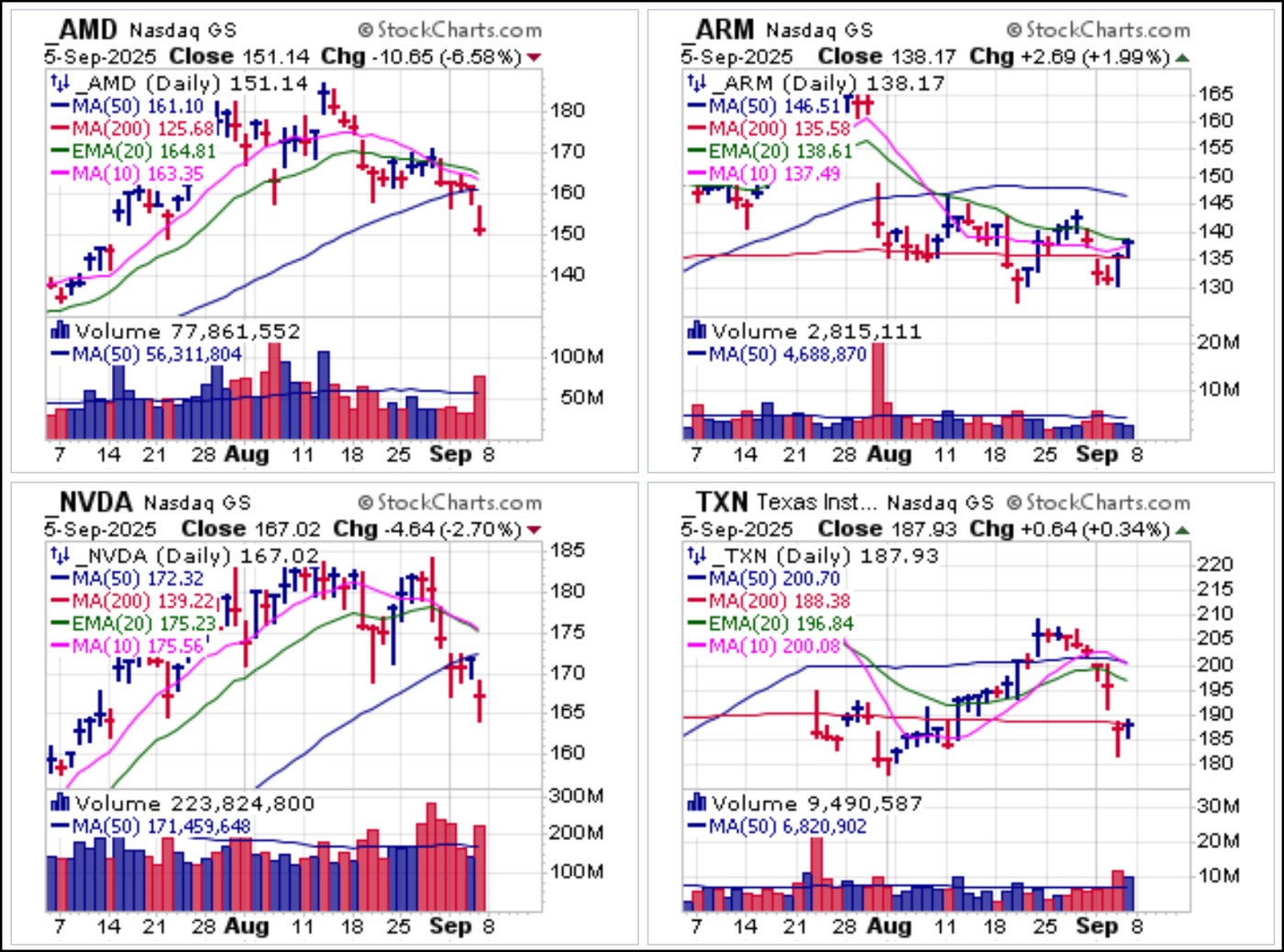

Last week we reported on Nvidia (NVDA) as a short-sale entry as it broke 50-dma support and the stock ended lower for the week. Other big-stock semiconductor leaders, such as Advanced Micro Devices (AMD), Arm Holdings (ARM), and Texas Instruments (TXN) illustrate various states of disrepair as they trend lower or lurk in the lower reaches of their charts.

Last week we reported on Nvidia (NVDA) as a short-sale entry as it broke 50-dma support and the stock ended lower for the week. Other big-stock semiconductor leaders, such as Advanced Micro Devices (AMD), Arm Holdings (ARM), and Texas Instruments (TXN) illustrate various states of disrepair as they trend lower or lurk in the lower reaches of their charts. On the other end of the spectrum, big-stock techs that have shown constructive basing action contrast sharply. Broadcom (AVGO), Ciena (CIEN), Credo Tech Group (CRDO), and Alphabet (GOOGL) all posted buyable gap-up moves (BGU) after earnings this week and as of Friday's close all remain above the intraday lows of their respective BGU price ranges. Technically this would make them actionable as BGUs as close to the intraday low as possible, while then using the same low as a selling guide.

On the other end of the spectrum, big-stock techs that have shown constructive basing action contrast sharply. Broadcom (AVGO), Ciena (CIEN), Credo Tech Group (CRDO), and Alphabet (GOOGL) all posted buyable gap-up moves (BGU) after earnings this week and as of Friday's close all remain above the intraday lows of their respective BGU price ranges. Technically this would make them actionable as BGUs as close to the intraday low as possible, while then using the same low as a selling guide. Gold posted fresh all-time highs this week as Spot Gold cleared the $3,600 level for the first time before ending the week at $3,587.00 an ounce. The SPDR Gold Trust (GLD) followed through on last week's slight breakout from an 180-week base. Technically, it remains within buying range of the breakout.

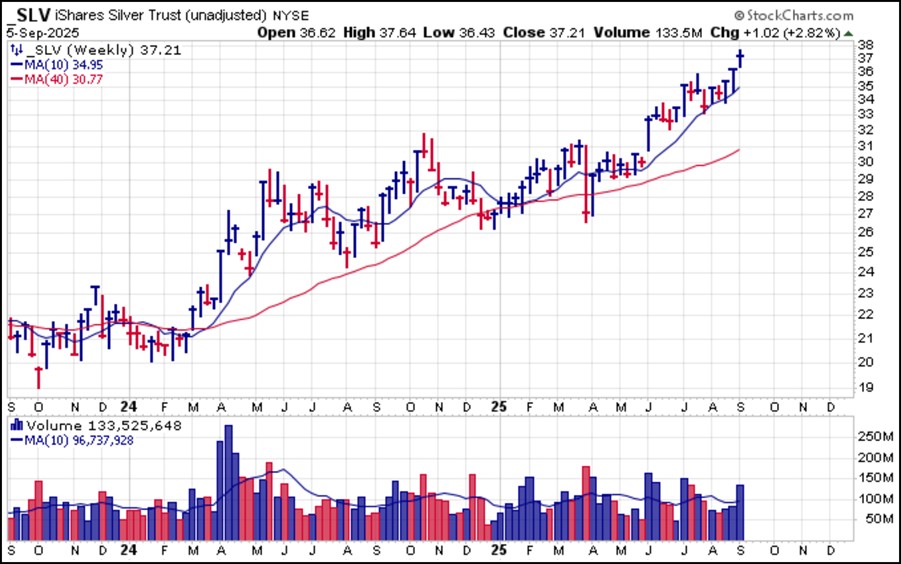

Gold posted fresh all-time highs this week as Spot Gold cleared the $3,600 level for the first time before ending the week at $3,587.00 an ounce. The SPDR Gold Trust (GLD) followed through on last week's slight breakout from an 180-week base. Technically, it remains within buying range of the breakout. Silver also followed through on last week's breakout from a short five-week base by posting a nearly 14-year high as Spot Silver hit a peak of 41.47 before settling in to end the week at 40.92. With the $40.00 an ounce level now in the rear view mirror, the $50 peak seen back in 2011 edges ever closer.

Silver also followed through on last week's breakout from a short five-week base by posting a nearly 14-year high as Spot Silver hit a peak of 41.47 before settling in to end the week at 40.92. With the $40.00 an ounce level now in the rear view mirror, the $50 peak seen back in 2011 edges ever closer. Gold and silver miners have, for the most part, moved sharply higher with gold and silver this past week, as the VanEck Gold Miners (GDX) and Global X Silver Miners (SIL) ETFs show below. These are now quite extended from their 10-day moving averages.

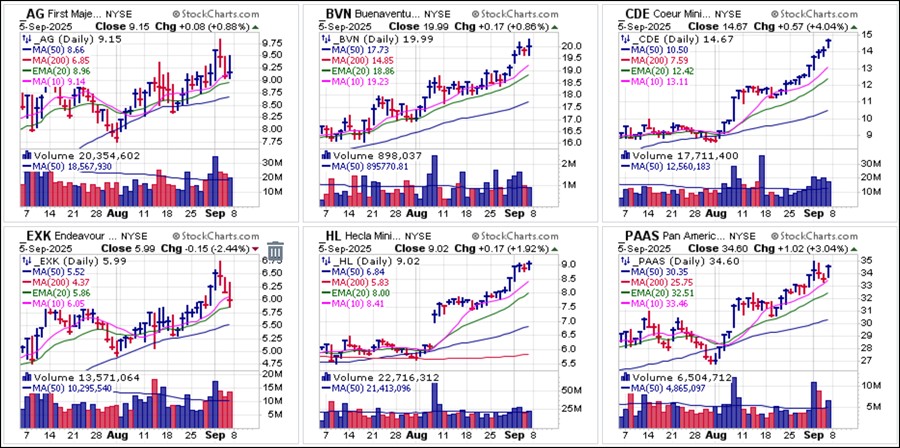

Gold and silver miners have, for the most part, moved sharply higher with gold and silver this past week, as the VanEck Gold Miners (GDX) and Global X Silver Miners (SIL) ETFs show below. These are now quite extended from their 10-day moving averages. Silver miners are mostly trending higher, but there are two notable exceptions among the six shown below. First Majestic Silver (AG) has pulled into 10-dma support, typically a long entry position using the 10-dma or 20-dema as a selling guide. Endeavour Silver (EXK) has declined nearly 13% off Wednesday's intraday peak on heavy selling volume over those three days. We would want to see volume rapidly dry up here along 20-dema support before seeking entry.

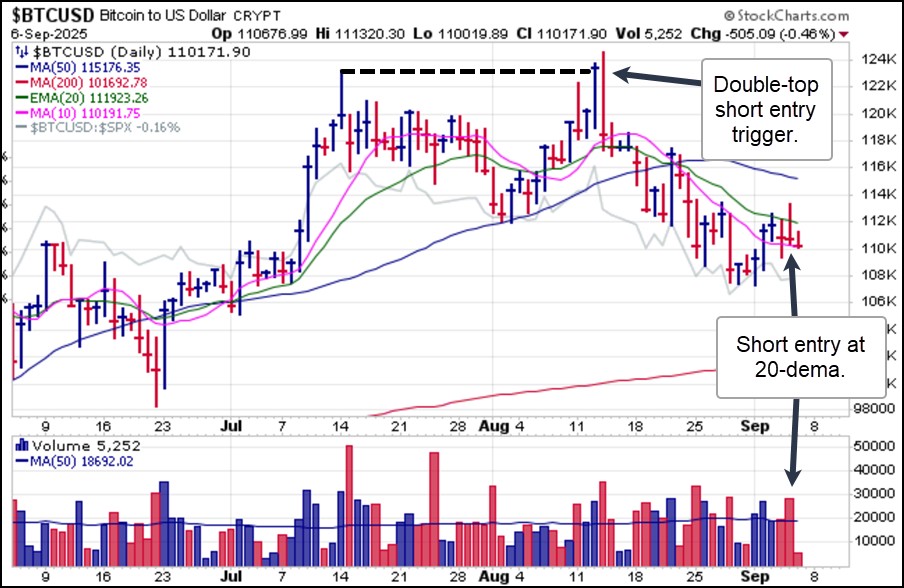

Silver miners are mostly trending higher, but there are two notable exceptions among the six shown below. First Majestic Silver (AG) has pulled into 10-dma support, typically a long entry position using the 10-dma or 20-dema as a selling guide. Endeavour Silver (EXK) has declined nearly 13% off Wednesday's intraday peak on heavy selling volume over those three days. We would want to see volume rapidly dry up here along 20-dema support before seeking entry. Bitcoin ($BTCUSD) remains in a downtrend after double-topping and posting a textbook double-top short-sale (DTSS) entry trigger back on August 14th. On Friday $BTCUSD reversed at 20-dema resistance where another short-sale entry was possible. As of mid-day Saturday it is starting to drift back below the 10-dma as well. It is interesting to note that having Trump as the self-declared Bitcoin President, along with numerous favorable news developments for $BTCUSD and cryptocurrencies stemming from his pro-crypto stance, including an Executive Order establishing a Strategic Bitcoin Reserve and U.S. Digital Asset Stockpile, the Genius Act which created the first federal regulatory framework for digital assets, and the more recent move to allow access to cryptocurrencies in 401(k) retirement plans $BTCUSD has now come all the way back to test the cup-with-handle breakout it posted as the favorable news flow gained momentum.

Bitcoin ($BTCUSD) remains in a downtrend after double-topping and posting a textbook double-top short-sale (DTSS) entry trigger back on August 14th. On Friday $BTCUSD reversed at 20-dema resistance where another short-sale entry was possible. As of mid-day Saturday it is starting to drift back below the 10-dma as well. It is interesting to note that having Trump as the self-declared Bitcoin President, along with numerous favorable news developments for $BTCUSD and cryptocurrencies stemming from his pro-crypto stance, including an Executive Order establishing a Strategic Bitcoin Reserve and U.S. Digital Asset Stockpile, the Genius Act which created the first federal regulatory framework for digital assets, and the more recent move to allow access to cryptocurrencies in 401(k) retirement plans $BTCUSD has now come all the way back to test the cup-with-handle breakout it posted as the favorable news flow gained momentum. On Tuesday and Wednesday we sent out a number of Short-Sale Set-Up reports, and these can be reviewed in hindsight in the group charts shown below. To some extent, this is almost tantamount to throwing mud at the wall and seeing what sticks. Sometimes, the set-up does not play out cleanly - there is often some chopping around before resolving one way or the other.

On Tuesday and Wednesday we sent out a number of Short-Sale Set-Up reports, and these can be reviewed in hindsight in the group charts shown below. To some extent, this is almost tantamount to throwing mud at the wall and seeing what sticks. Sometimes, the set-up does not play out cleanly - there is often some chopping around before resolving one way or the other.Of the reports sent out on Tuesday, we see that Advanced Micro Devices (AMD) worked well as it quickly broke below 50-dma support and broke to lower lows on Friday. Nuclear reactor builder GE Vernova (GEV) rallied back above its 50-dma on Thursday and then reversed at the line where it became a short entry. It reversed nicely but is essentially back to where it was on Tuesday. Meta Platforms (META) was hanging along 50-dma support on Tuesday but then gapped back to the upside on Thursday where it posted a stalling pocket pivot, holding tight along the 10-dma and 20-dema on Friday.

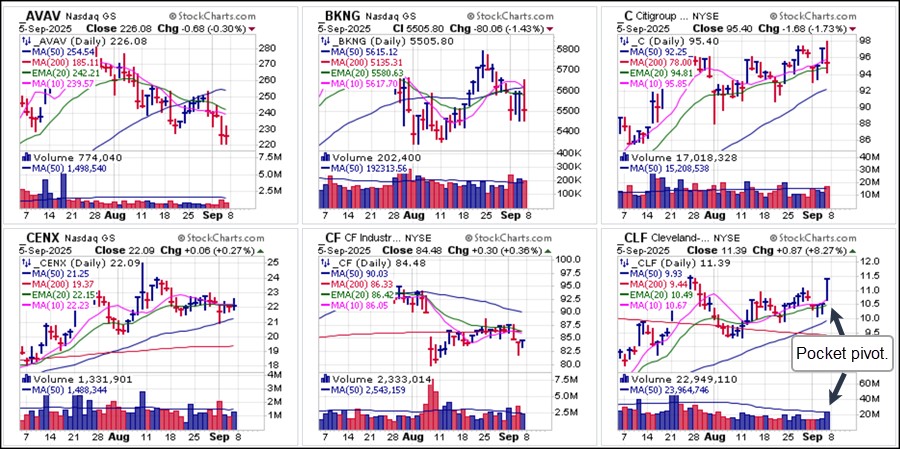

The group chart of 12 stocks we reported on as Short-Sale Set-Ups on Wednesday shown below also present a mixed bag. Of the 12, only six are lower than where they were on Wednesday. And, in most of those cases, not by much.

The group chart of 12 stocks we reported on as Short-Sale Set-Ups on Wednesday shown below also present a mixed bag. Of the 12, only six are lower than where they were on Wednesday. And, in most of those cases, not by much.

Overall this remains a difficult environment on a stock-by-stock basis. The only area of the market that has consistently performed strongly on the upside over the past week has been the precious metals space, including both gold and silver as well as the various mining stocks. We expect that the market will remain challenging, with various set-ups presenting mixed results. Tread carefully.

Overall this remains a difficult environment on a stock-by-stock basis. The only area of the market that has consistently performed strongly on the upside over the past week has been the precious metals space, including both gold and silver as well as the various mining stocks. We expect that the market will remain challenging, with various set-ups presenting mixed results. Tread carefully.The Market Direction Model (MDM) remains on a BUY signal.