by Dr. Chris Kacher

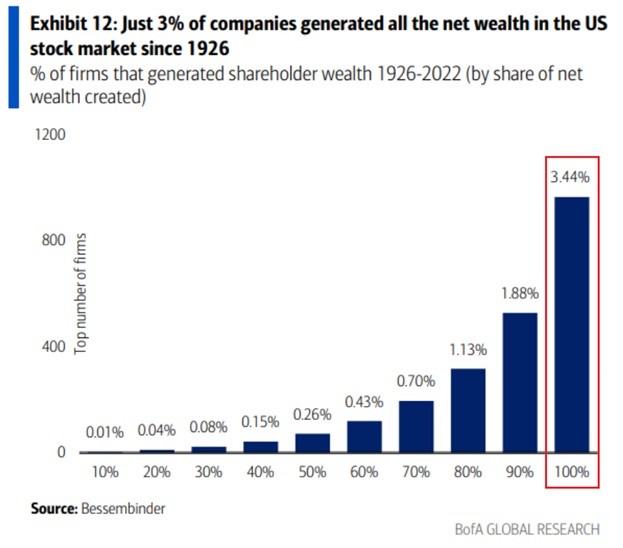

ALL net wealth in the US stock market since 1926 has been generated by just 3.44% of companies. To put this differently, ~97% of all stocks have barely contributed to long-term shareholder wealth creation. The top 1.88% of companies reflect 90% of total gains. Interestingly, just 0.26% of firms have created HALF of all wealth. This highlights the extreme concentration of stock market returns in top-performing companies. While we see the market being more bifurcated than ever by AI-driven big tech, market wealth is often heavily skewed toward a very small minority of companies.

Jobs data show:

The unemployment rate is creeping higher and job growth is stagnant

Companies like Amazon and Meta are initiating layoffs and blaming AI-driven productivity increases

That said, AI is enabling companies to boost productivity with fewer workers, creating a dual effect: it’s both a reason companies give for layoffs and a real justification for trimming staff. Moreover, even businesses that haven’t cut headcount are shifting their hiring focus because of this new technology. Looking ahead, it’s possible that meaningful productivity gains from AI will reduce overall labor demand even as the economy itself grows.

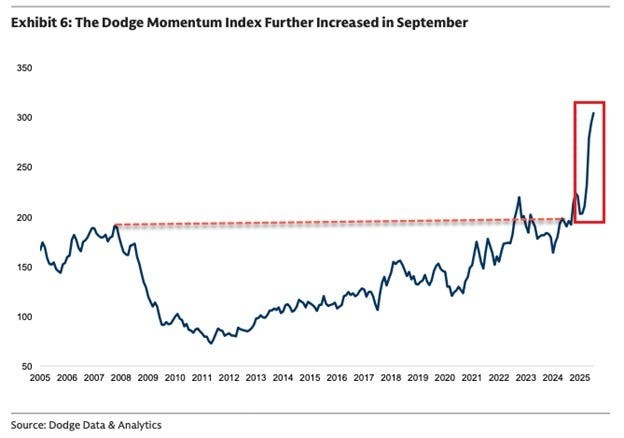

AI data center demandThe surge in AI-driven data center projects is set to translate into a powerful construction boom across the US in 2026. AI’s impact on the real economy is accelerating. This is nicely illustrated by the Dodge Momentum Index which surged +60% YoY in September to the highest on record. This index serves as a leading indicator of non-residential construction, tracking projects that typically move from planning to groundbreaking within 9–12 months.

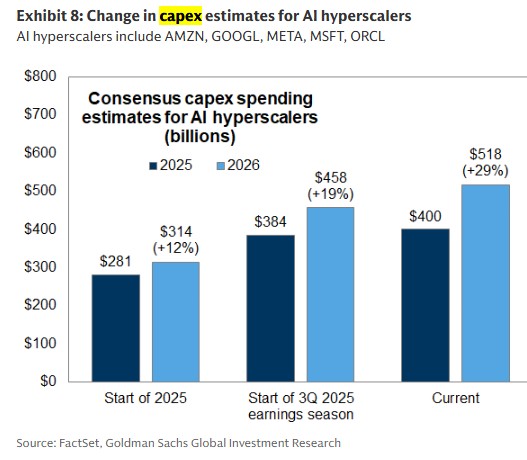

Goldman Sachs said a big reason for this explosion is that mega-cap companies continue to exceed expectations on their AI CAPEX spending.

Companies are sinking massive sums into building data centers and power generation. In fact, the investment in power generation is very important to pay attention to because the market is realizing that power, not chips, are the limiting factor for hyperscalers.

Borrowing to fund AI datacenter spending exploded in September of this year.

The CEO of Microsoft said he has the compute capacity but doesn’t have the data centers and power supply to plug them into.

Thus the leverage moves to whoever controls energy & infrastructure. Every new data center that MSFT, GOOGL, AMZN, META & ORCL are trying to build needs hundreds of megawatts of steady power. Getting that energy online now takes years which means the players who locked in power early & built vertically across the stack are the ones with real control. Hyperscaler growth is no longer defined by how many GPUs they can buy but by how quickly they can energize new capacity.

VanEck’s Matt Sigel points out $15 billion in Bitcoin mining deals in a day. Sector market cap: ~$65 billion. This is equivalent to if the oil majors announced deals worth 20% of their market cap in one day. The speed at which AI is rewiring the global energy stack is beyond breakneck.

The two recent deals come from IREN and CIFR, two bitcoin mining businesses that are making the transition into AI data center providers. IREN announced a $9.7 billion AI cloud contract with Microsoft and CIFR announced a $5.5 billion deal with Amazon’s AWS.

Both had buyable gap ups. We recommended IREN back on May 1, 2025.It’s tough to say the AI bubble is about to burst when demand is screaming louder than supply everywhere you turn. Bubbles burst when the market is flooded with supply and buyers dry up, but right now, we’re nowhere near that scenario. Demand is surging and outpacing every drop of available capacity. Meanwhile, President Trump is creating policies that act as a tailwind for the industry.

Bitcoin correction continues

At the Oct 29 conference, Fed Chair Jerome Powell made some hawkish comments saying, “A further reduction in the policy rate at the December meeting is not a foregone conclusion, far from it.”

Higher rates typically strengthen the US dollar, giving institutional investors more incentive to stay holding dollars and less incentive to invest in risk-on assets such as Bitcoin.

These comments spurred doubt in institutional investors, pushing them to sell their Bitcoin and Ethereum as shown by the outflows in both ETFs.

These corrections with 20-30% depth and 1-4 months in duration have been fairly standard as can be seen in a weekly chart of Bitcoin. The current one has a depth of 22% and has run 1 month. Further, when Bitcoin breaks support as it did a few weeks ago, it tends to fall further in quick fashion before regaining its footing and moving to new highs in the ensuing weeks as it did earlier this year, twice in 2024, and three times in 2023. Nevertheless, continue to steer clear until you see a proper undercut & rally pattern or the cross below then back above $100k as it did on Tuesday when we notified members.

A wave of long positions being wiped out which often signals major lows in bitcoin. This has been the main accelerator of the bearish price action. These liquidations have now largely been burnt through.

Liquidity also continues to flow into Bitcoin showing the bull market is still intact.

Further, a bullish divergence between price and liquidity is quietly forming. This points to a bottoming phase in development where historically price follows 1-2 weeks later.

Bitcoin weekly RSI is in the oversold zone which since 2023 has always produced bounces lasting from a few days to a few months, where in the case of a few days, prior lows act as support.

So while bitcoin could still restest lows, it should find a major floor sooner than later. While no one has a crystal ball, it's always about the odds. Stacking various bullish indicators push the odds in one's favor. But as always, keep your stops tight when it comes to bitcoin or its various related companies and ETFs.

Bitcoin and Fiat Have No Intrinsic Value

No tangible backing: Neither Bitcoin nor fiat currency is backed by physical assets like gold or commodities.

Value based on trust: Both derive value from collective social consensus and trust rather than inherent material worth.

Fiat depends on government authority: Fiat's value comes from legal tender status and trust in government and central banks.

Bitcoin depends on technology and network: Bitcoin's value stems from its decentralized blockchain, cryptographic security, and finite supply.

Both are social constructs: Their purchasing power arises because people mutually agree to accept them as payment.

Why Bitcoin Is Superior to Fiat

Fixed supply ( scarcity ): Bitcoin’s capped supply of 21 million coins protects against inflation, unlike fiat which can be printed ad infinitum, causing devaluation.

Decentralization: No single central authority controls Bitcoin, reducing risks of manipulation and political interference that fiat currencies face.

Transparency and security: Bitcoin transactions are secured by blockchain technology, making it tamper-proof and resistant to fraud.

Global and borderless: Bitcoin operates without reliance on any country or bank, enabling frictionless global payments and transfers.

Digital and programmable: Bitcoin can integrate with new financial technologies and smart contracts, offering innovation beyond traditional money.

Inflation resistance: Unlike fiat, Bitcoin's scarcity and predictable issuance schedule make it a potential store of value against inflationary pressures.

In summary, while both lack intrinsic value in the classical sense, Bitcoin's design features give it superior characteristics as a durable and censorship-resistant form of money compared to traditional fiat currencies.