Market Lab Report

by Dr. Chris Kacher

The Web3 Evolution Will Not Be Centralized™

Due to a key change made to the Market Direction Model in Feb-2019 almost 5 years ago, whipsaws were minimized as it has aimed since then to capture the major trends in the major averages. The recent slew of perceived bullish data caused the straight up from bottom market action since Wednesday November 1. This was the result of Fed chair Powell's testimony that same day, strong earnings overall since then, and productivity well above expectations that was reported last Friday. Add in a powerful short squeeze due to the high percentage of hedge funds that were short and you have a powerful bounce. But is it sustainable?

Lies, damned lies, and data: Inflation

To take poetic license from the great Mark Twain, there are lies, damned lies, and data. We know the data reported by governments is heavily skewed. A hard landing or worse is still in the cards. Nevertheless, markets use such metrics to gauge the present moment strength or weakness of markets. Overall, markets still remain in a sloppy downtrend with lower highs and lower lows though a potential double top is forming in the NASDAQ Composite and S&P 500 which would make a higher high.

Markets interpreted Powell's testimony given on Wednesday November 1 as dovish that despite moderating inflation, rates would have to remain elevated to accomplish the 2% mandate. This is not much different from his prior stance. Wage inflation stands at 4.5%. The PCE which is the Fed's preferred measure of inflation showed its services component came in above expectations. In consequence, rates could stay elevated for much longer than people think. Nevertheless, Powell implied rate hikes are over, though of course, this is always data dependent.

The Fed's Kashkari on Tuesday said the labor market continues to be quite robust and that he was not seeing evidence the economy is weakening. He said if inflation ticks back up, the Fed's job is not yet done.

Sticky inflation in areas that people need the most including food, energy, transportation, and housing remains an issue so rates may need to stay elevated for longer than expected. While many predicted the cost of housing to drop in 2022-2023, those who financed at very low rates of interest are not about to sell so the supply side of housing remains low despite demand also being pushed lower from rising rates. Meanwhile, the value of fiat continues to degrade due to inflation which, while moderating, is still appreciably increasing, so the price of real estate and rents continues to increase. Faced with soaring inflation and a collapsing bond market, who would sell their property and go to cash or buy bonds?

Friday's jobs report showed a cooling jobs market which implied rate reductions could come ahead of predictions. Unemployment rose to 3.9%, the highest since Jan-2022, from a low of 3.4% set earlier this year. This could be the start of an acceleration in unemployment in the coming months if history is any guide.

CME FedWatch now expects the first rate reductions in May-2024. Keep in mind that history shows that the Fed tends to overshoot when it comes to interest rates which eventually breaks the economy forcing them to lower rates in a hurry. The first rate reduction is therefore typically the first in a string of fast rate reductions as stock markets enter into prolonged downtrends.

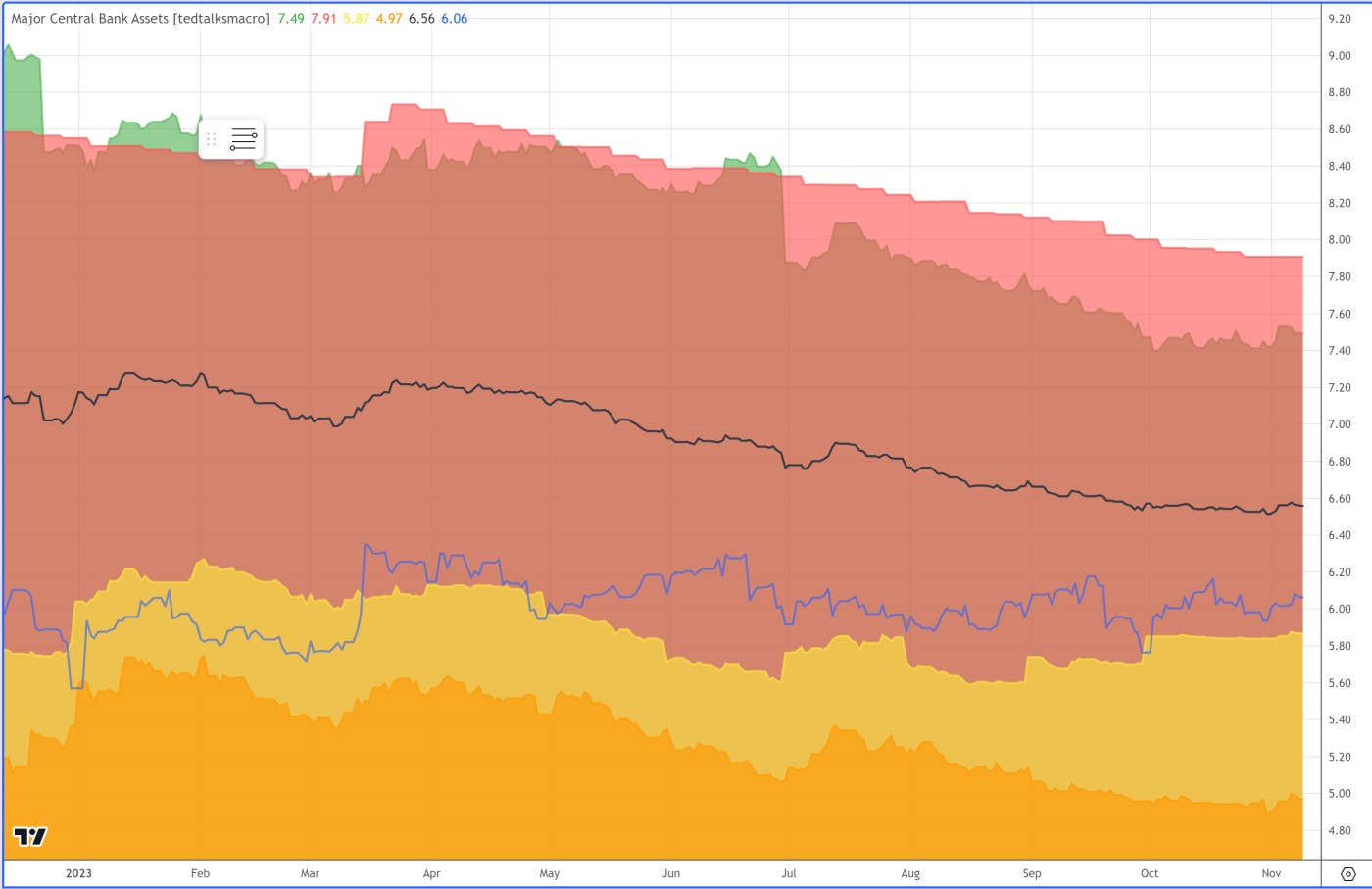

Liquidity

US and global liquidity has been on the rise but nothing substantial has materialized as of yet. This could be another upside blip before the downtrend in liquidity resumes. That said, stealth QE could continue higher. The US will have to print to fund unfunded liabilities such as pensions and IRAs along with servicing its onerous debt interest. The recent bounce in Bitcoin spurred Ethereum to follow along which sent other cryptocurrencies higher. Much of these gains are due to the belief that Blackrock will have its spot Bitcoin ETF approved by the SEC. But when you look at the numbers, because Bitcoin's valuation stands at nearly $700 billion, $25 billion of fast inflows into its Bitcoin ETF may help push Bitcoin 15-20% higher at best then it's back to the normal function of macro, metrics, and market dynamics. It could also be a sell the news event much as happened when the first Bitcoin futures vehicle was launched in late 2021. For those who ask about the bullish nature of Bitcoin's halving event, this is also somewhat minor compared to prior halvings due to Bitcoin's valuation. Additionally, each halving reduces supply by only half as much as the prior halving.

The black line represents global liquidity. It had been on an overall downtrend all year but since late September, it has been flatlining.

Bitcoin miners

While Bitcoin miners have been a high alpha strategy to play Bitcoin, they have been lagging the price of Bitcoin as of late. Mining companies such as MARA, RIOT, and HUT which have been used as rough proxies to gaining exposure to Bitcoin are concerned that the likely spot Bitcoin ETF that could launch in the first quarter of 2024 could steal buying pressure. But should Bitcoin continue higher, these miners will likely catch up as they always have, and any reduced buying pressure as a result of an approved spot Bitcoin ETF would become apparent from that point. Another reason miners have been lagging is due to the Bitcoin halving event on April 24, 2024 which means that miners will have to spend more to receive fewer rewards. But such is similar to prior halving events so there are measures that can be taken.