Market Lab Report / Dr. K's Crypto-Corner

by Dr. Chris Kacher

The Metaversal Evolution Will Not Be Centralized™

Schizo markets

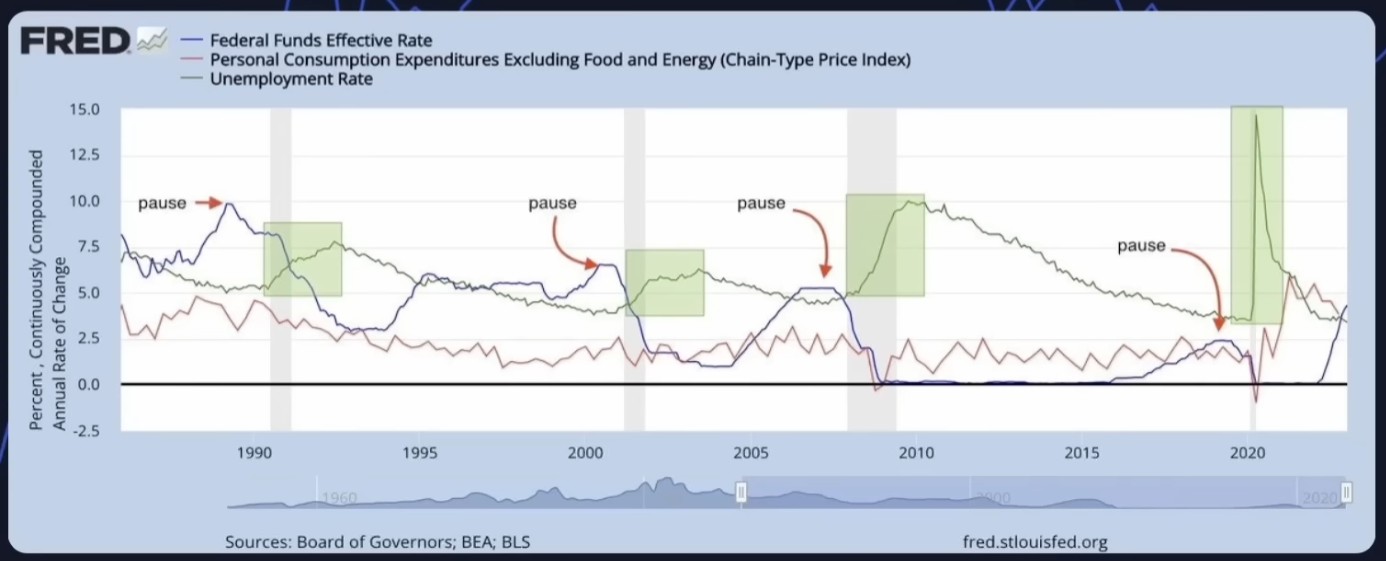

So the Fed went from hawkish words in December to what the market perceived as more dovish body language in January though the words were the same then back to hawkish words as of late. December's drop then January's bounce has been followed by February's hesitation. While unemployment remains robust and GDP remains positive, markets are on tenterhooks because the market currently predicts three more 25 bps rate hikes due to inflation overall being stickier than expected.

Bonds are projecting higher rates ahead while the dollar continues to bounce.

Chinese QE

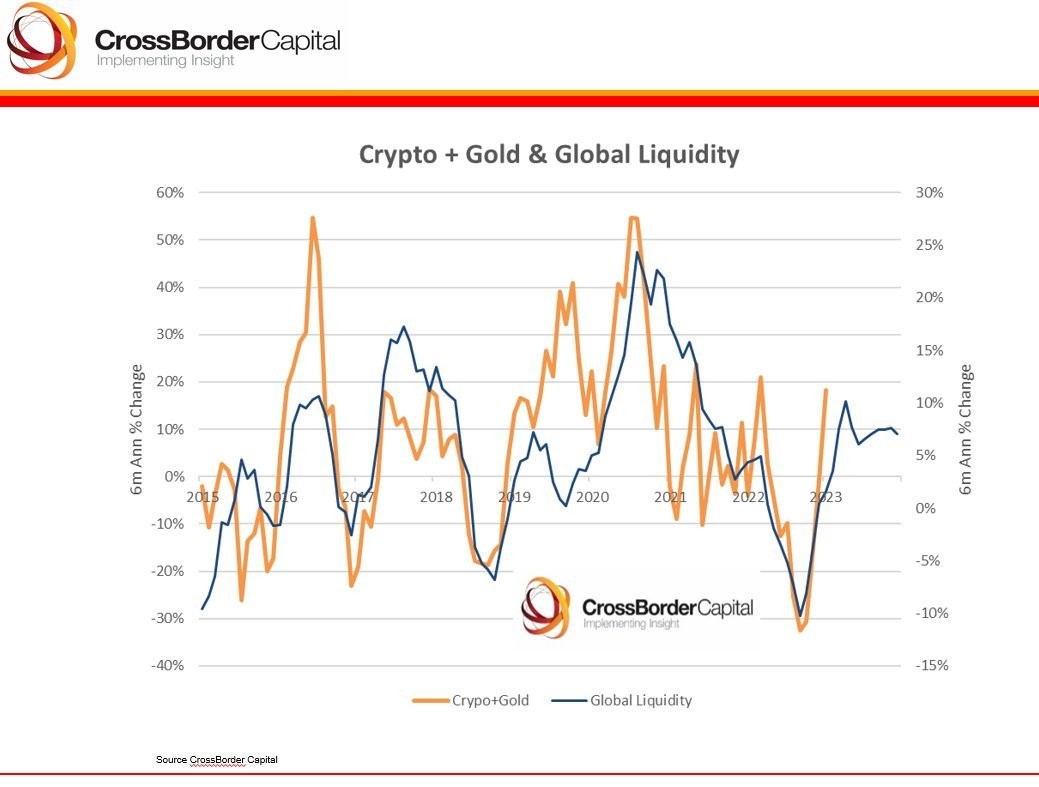

That said, the makings of an economic recovery in China began when the 'zero covid' policy was ended in late 2022. New Chinese bank loans hit a record 4.9T Yuan in January. Since China's economic reopening, it has been printing money to stimulate its economy which more than offsets the tightening going on in the US, UK, and EU. In consequence, global liquidity has been rising since late 2022. Note that global liquidity can lead or lag market direction by many months such as when it topped in mid-2017 and mid-2020, many months before stock and crypto markets topped. And the degree to which the Fed is hawkish or dovish still has a major impact on determining the overall direction of US stock markets.

But China's money printing together with the Fed's QE-lite of tapping into its $2 trillion in repo reserves to service debt can create choppy trendless stock and crypto markets. But it is more likely that another shoe will drop as the world sits on numerous tipping points as well as recession that takes hold sometime in the second half of this year based on my recent analysis. Markets will then start into new downtrends which persist even after the Fed halts then reduces rates. Unemployment then starts to jump as recession takes hold.

Bear market over sooner than later

Global stimulus together with the Fed reducing rates by raising M2 sometime in the second half of this year may put a faster end to any prolonged bear market. While inflation is likely to remain elevated well above the Fed's 2% mandate, they will be forced to lower rates as recession takes hold sometime in the second half of this year. This will push inflation both in the US and the rest of the world higher. This is contrary to history since in today's world, QE out of China matters in addition to record levels of debt, interest rates having been at multi-millenium lows, and soaring inflation.

To those who asked how the policies of ESG (Environmental, Social, and Governance) are creating global inflation, one of countless examples is Sri Lanka. ESG pressured their government into switching to using only organic fertilizers, away from chemical and nitrogen-based fertilizer. In consequence, their crop and rice production plummeted denting global supply. With less supply and rising demand, prices have risen for many crops since fertilizer is a cardinal commodity. This is another reason why food inflation is less likely to abate anytime soon.

This cross current of events between persistent inflation, incoming recession, and massive global debt spurs a tug-o-war between what the Fed wants to do and what it will have to do.