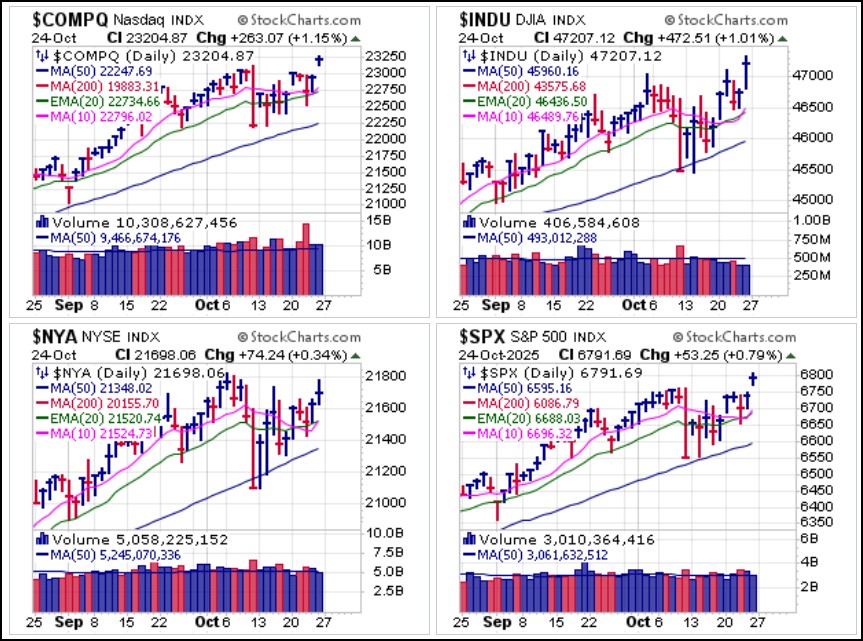

Core CPI printed 0.2% vs. expectations of 0.3% and Headline CPI 0.3% vs. expectations of 0.4%. Annual inflation remains at around 3% as the government measures it, which likely indicates that real inflation is somewhere at 5-6%. Nevertheless, 3% is well above the Fed's alleged long-term inflation target of 2%, but is not likely to keep the Fed from lowering rates again when they meet this week. The market has already taken the liberty of bringing rates down well ahead of the Fed, with the 3-Month ($TYX), 10-Year ($TNX), and 30-Year ($TYX) Treasury Yields trending to lower lows this past week.

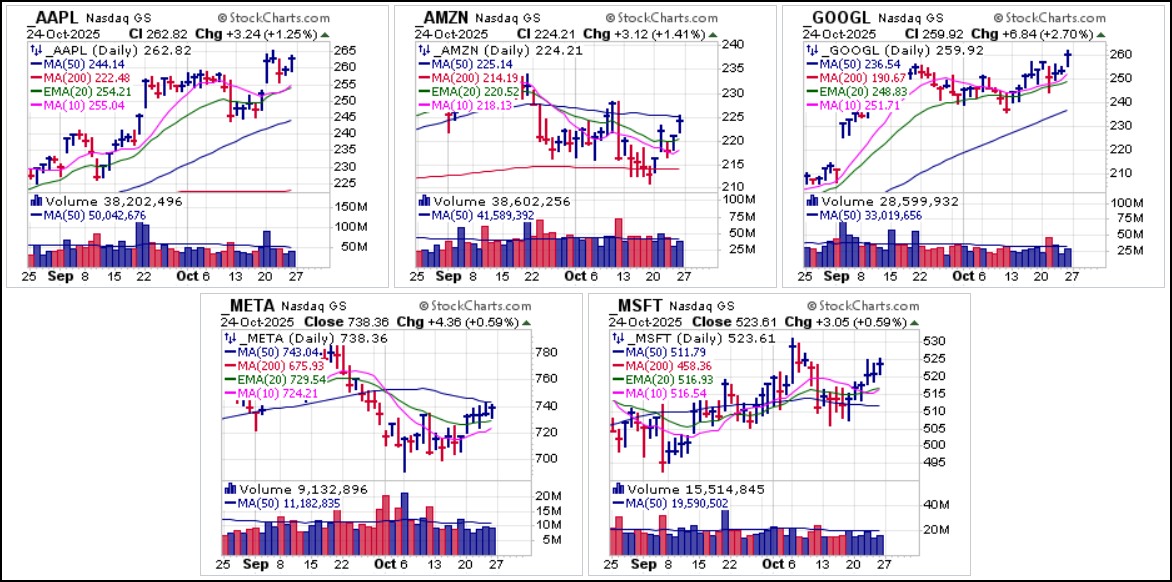

Core CPI printed 0.2% vs. expectations of 0.3% and Headline CPI 0.3% vs. expectations of 0.4%. Annual inflation remains at around 3% as the government measures it, which likely indicates that real inflation is somewhere at 5-6%. Nevertheless, 3% is well above the Fed's alleged long-term inflation target of 2%, but is not likely to keep the Fed from lowering rates again when they meet this week. The market has already taken the liberty of bringing rates down well ahead of the Fed, with the 3-Month ($TYX), 10-Year ($TNX), and 30-Year ($TYX) Treasury Yields trending to lower lows this past week. Earnings season is heating up as several big-stock NASDAQ names and index influencers are set to report this week. On Wednesday, Alphabet (GOOGL), Meta Platforms (META), and Microsoft (MSFT) are expected to report after the close, with Apple (AAPL) and Amazon.com (AMZN) expected on Thursday after the close. AMZN and META have been living below their 50-dmas for several weeks now and on Friday rallied up to 50-dma resistance. AAPL and GOOGL are both in breakout positions while MSFT is splitting the difference as it has recently recovered back above the 50-dma but remains well off its recent all-time highs. How these earnings reports play out, on balance, could have a marked effect on the general market action, so will be worth watching closely this week.

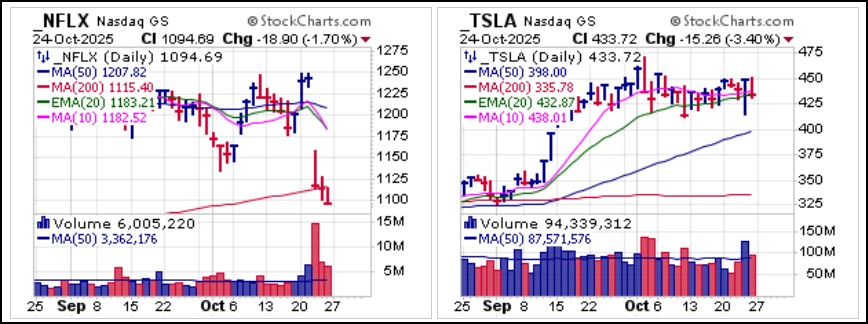

Earnings season is heating up as several big-stock NASDAQ names and index influencers are set to report this week. On Wednesday, Alphabet (GOOGL), Meta Platforms (META), and Microsoft (MSFT) are expected to report after the close, with Apple (AAPL) and Amazon.com (AMZN) expected on Thursday after the close. AMZN and META have been living below their 50-dmas for several weeks now and on Friday rallied up to 50-dma resistance. AAPL and GOOGL are both in breakout positions while MSFT is splitting the difference as it has recently recovered back above the 50-dma but remains well off its recent all-time highs. How these earnings reports play out, on balance, could have a marked effect on the general market action, so will be worth watching closely this week. Two other big-stock NASDAQ Netflix (NFLX) and Tesla (TSLA) reported this past Tuesday and Wednesday, respectively, with mixed results. NFLX gapped down after reporting and then broke below 200-dmasupport in decisive fashion on Friday. TSLA pulled a big outside reversal to the upside after initially gapping down after earnings to post a big-volume pocket pivot and moving average undercut & rally (MAU&R at the 10-dma and 20-dema). No upside follow-through was forthcoming, however, as it sold back into 20-dema support on above-average selling volume, which is either going to play out as a lower-risk long entry if it holds the line or a short-sale entry trigger if it fails to hold the 20-dema.

Two other big-stock NASDAQ Netflix (NFLX) and Tesla (TSLA) reported this past Tuesday and Wednesday, respectively, with mixed results. NFLX gapped down after reporting and then broke below 200-dmasupport in decisive fashion on Friday. TSLA pulled a big outside reversal to the upside after initially gapping down after earnings to post a big-volume pocket pivot and moving average undercut & rally (MAU&R at the 10-dma and 20-dema). No upside follow-through was forthcoming, however, as it sold back into 20-dema support on above-average selling volume, which is either going to play out as a lower-risk long entry if it holds the line or a short-sale entry trigger if it fails to hold the 20-dema. It was an historic week for gold as Spot Gold printed an all-time high of $4,381.51 on Monday before selling off over 5% on Tuesday. Many felt that the $4,000 level would present logical round number resistance for the yellow metal, but it simply streaked through $4,000 last week before finally correcting this week. And while many are trying to call the top in gold, for now the $4,000 level and the 20-dema have held as near-term support.

It was an historic week for gold as Spot Gold printed an all-time high of $4,381.51 on Monday before selling off over 5% on Tuesday. Many felt that the $4,000 level would present logical round number resistance for the yellow metal, but it simply streaked through $4,000 last week before finally correcting this week. And while many are trying to call the top in gold, for now the $4,000 level and the 20-dema have held as near-term support.Meanwhile, Spot Silver, after reaching a new all-time high of $54.49 an ounce two Fridays ago, corrected sharply and is now sitting in a short bear flag just below the 20-dema.

Bitcoin (BTCUSD) regained the 200-dma earlier this past week as it also pushed back above the late August and September lows. It is currently pushing up against 20-dema resistance as it remains in what is now a two-week bear flag after breaking very sharply off the peak two weeks ago. That said, zooming out, BTC typically catches up to the general trends in gold and the recent weakness in BTC was due largely to regional bank blowups which affect risk-on assets such as bitcoin as detailed in our prior reports.

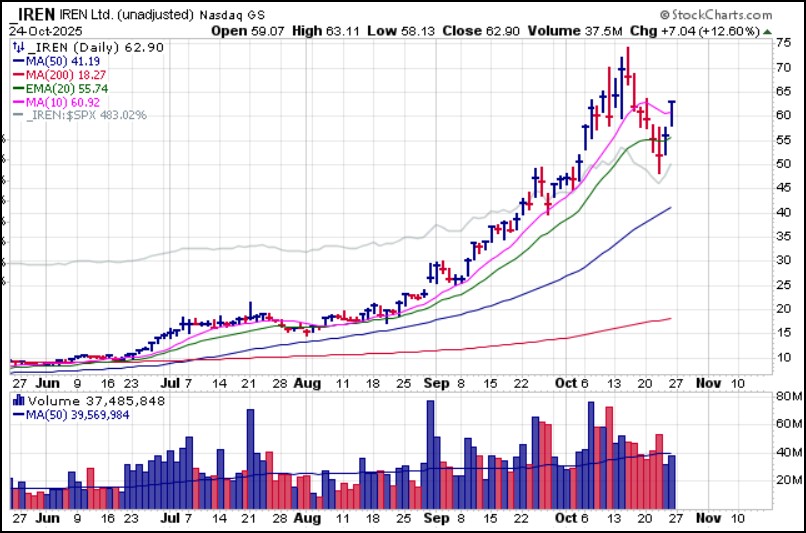

Bitcoin (BTCUSD) regained the 200-dma earlier this past week as it also pushed back above the late August and September lows. It is currently pushing up against 20-dema resistance as it remains in what is now a two-week bear flag after breaking very sharply off the peak two weeks ago. That said, zooming out, BTC typically catches up to the general trends in gold and the recent weakness in BTC was due largely to regional bank blowups which affect risk-on assets such as bitcoin as detailed in our prior reports.  This remains a difficult environment where volatility is the rule of the day against a backdrop of suddenly shifting trade news and tariff threats from Trump. One of our best-performing names, IREN Ltd. (IREN) illustrates this after triggering a Seven-Week Rule sell signal when it violated the 10-dma earlier in the week. That led to a quick shakeout at the 20-dema which was also an MAU&R long entry, and IREN went on to close the week back above the 10-dma. The primary issue here is that holding the stock would have required sitting through a -42% decline off the peak!

This remains a difficult environment where volatility is the rule of the day against a backdrop of suddenly shifting trade news and tariff threats from Trump. One of our best-performing names, IREN Ltd. (IREN) illustrates this after triggering a Seven-Week Rule sell signal when it violated the 10-dma earlier in the week. That led to a quick shakeout at the 20-dema which was also an MAU&R long entry, and IREN went on to close the week back above the 10-dma. The primary issue here is that holding the stock would have required sitting through a -42% decline off the peak! Some of the volatility is being seen in the Market Direction Model (MDM), which switched to a CASH/NEUTRAL signal on Thursday, October 23rd before switching back to a BUY signal on Friday, October 24, 2025.

Some of the volatility is being seen in the Market Direction Model (MDM), which switched to a CASH/NEUTRAL signal on Thursday, October 23rd before switching back to a BUY signal on Friday, October 24, 2025.