Premarket Pulse + Crypto Report

by

Dr. Chris Kacher

Druckenmiller says the running joke is that the stock market has predicted the last 9 out of 5 recessions, but this is still better than the Fed who has gone 0 for 9 in predicting recessions. The inside of the stock market is the best predictor of recessions, as he has used such metrics to predict numerous past recessions.

The cyclicals of the stock market recently showed auto stocks down -30%, building stocks -35%, banks -25%, retailers -20%, yet the S&P 500 was down only -11% at the time. This is because utilities, staples, and pharmaceuticals which are defensive were up for the year. This is not a red flag but what he calls an amber flag. Another amber flag is the flattening yield curve in a low rate environment. He is hoping the bubble can unwind before his indicators turn from amber to red. He is suggesting the Fed stop hiking rates though is not asking for a cut. He also suggests they stop automatically shrinking the balance sheet by $50 billion a month but make it data dependent. With $50 billion a month shrinkage of the Fed's balance sheet right when the ECB and other central banks are not offsetting it as they continue to print money, it comes at a great cost to the U.S. Druckenmiller is concerned but still thinks the air can be let out of this asset bubble without causing a crash. To wit, he thinks the S&P 500 could return 0 to 5% annually over the next 5 years, similar to what Ray Dalio has suggested, ie, a slow grind higher.

We have been in a global bear market for a year now. Global economies have always been deeply connected, even going back to the 19th century, thus it could be argued it's only a matter of time before the rest of the world pulls down the U.S. stock market.

The Fed's mandate is to maximize employment, but uses jobs data which is a lagging indicator, so they are always looking behind, not ahead, thus their awful scorecard in predicting recessions. If anyone suggests Druckenmiller is trying to support Trump by agreeing with his position on halting rate hikes, Druckenmiller makes more money in bear markets, so would on that basis welcome the Fed doing the wrong thing by continuing to hike rates.

If the Fed caved into Trump's demands of halting the hikes, this would be seen as a loss of credibility to the Fed. But it would be just as horrific if the Fed didn't pause because they were afraid the public would think they were being bullied by Trump by halting the hikes. Druckenmiller says the Fed could even reduce rates at some point if things got much worse. But as we have said, they do not have much room to lower rates as rates remain well below the historical norm.

A Christmas Crash?

Major averages have undercut prior lows. From peak to trough, the S&P 500 is off -18.1% , NASDAQ Composite -22.8%, and Dow Industrials -16.9%. The small cap Russell 2000 was the first to reach bear market territory and is currently off -26.0% peak to trough. That said, the Russell 2000 being the more volatile index was off more than -20% in 2011 and 2014-2015. The NASDAQ Composite was also off -20.4% in 2011 and -19.5% in 2016. But after Friday's action, it is fairly evident the general market is finally in a proper bear market after 10 years of QE, whether coming from the Fed or from global central banks.

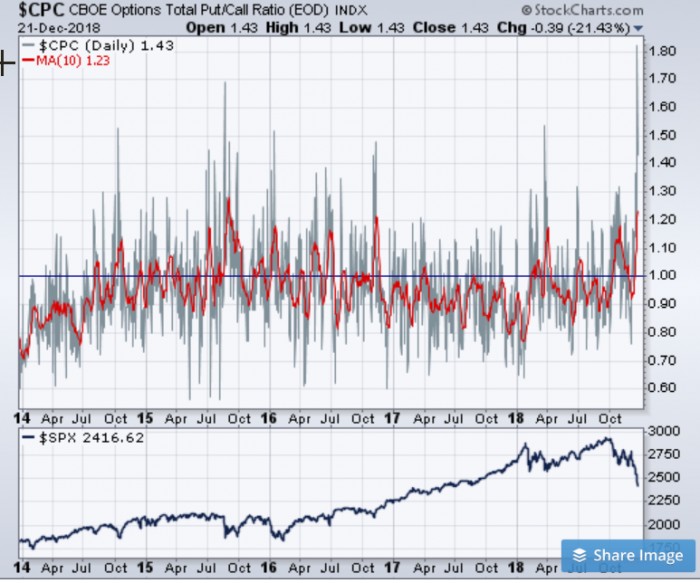

After the bounce leading into December at which point the Market Direction Model went from a buy to a cash signal, the stock market has been hit hard. This has been the weakest market at this time of year in many decades. The CBOE options put/call ratio spiked to 1.37 earlier this week yet it did not produce a bounce. There have been no Xmas crashes on record, yet this one qualifies, underscoring the stark weakness of the current environment. Thursday's pummelling spiked the put/call to 1.82, at least a 5+ year high, yet the market still could not rally. The put/call remained elevated on Friday at 1.43 as new index lows were achieved.

The market reacted poorly to the Fed's announcement on Wednesday. Powell had little to say in the way of justifying the rate hike. For now, Fed chair Powell says that the Fed is now looking at 2 rate increases in 2019 instead of 3. But should the economy weaken, they may not be able to hike at all, and instead be forced to go in the other direction even without much interest rate fuel in their tank with rates nowhere near historical norms. The problem is they have no idea what they're doing. We are in unprecedented times. Why do we assume just because they are Fed-Heds that they know what they are doing? Politico-speak and reputation lends believability to their 'expertise'. But once outside their historical comfort zone, what do they really know? Yet we proscribe superhuman abilities to this group that dictates monetary policy which ends up creating massive diverges and a destabilization of the middle class while having predicted the last zero out of nine recessions, as per the Druckenmiller interview above.

Yields on bonds continue to fall as it appears the Fed will have to slow the pace or bring to a halt its rate hikes. Certainly being a political body, the Fed will do what it takes to insure the ageing bull they have built since QE began in 2009 does not have a heart attack. Or perhaps *roll the conspiracy music* they wish to topple Trump's presidency by clobbering the stock market by maintaining an aggressive stance with respect to interest rate hikes. Without confirming or denying as complete information is still lacking, some have suggested the rabbit holes go deep when it comes to the progressive left which remains formidable.

In any event, nothing in the way of individual stocks has been working thus cash or the short side have been the place to be. The best opportunities have been on the short side in those stocks that rallied up into resistance before the market rolled over again. Stocks remain gutted.

Blockchain Cryptowinter

It is possible the Trump pro-business policies may help keep the economy afloat together with the numerous exponential growth technologies coming online such as blockchain, artificial intelligence, and virtual reality. But even so, one will remember the NASDAQ had its steepest correction of -78% from March 2000-2002 despite the progress made by the internet. Thus, fast growing cutting edge technologies may not be sufficient to stave off a major bear market. Further, there are signs the economy is slowing as on Thursday, the Philly Fed came in at 9.4 vs. expectations of 17.5. Also of note, some may remember that Reagan's pro-business, reduced government policies took some time to take effect after he was elected in 1980 as illustrated by the 1981-82 recession which was long and deep.

The dot-com crash back in 2000-2002 may be illustrative of the current situation in the blockchain/crypto market where most cryptocurrencies and tokens have lost -95% or more of their value. This crypto winter is so far playing out similar to the correction from Dec 2013 to Jan 2015 when bitcoin lost -87% and other coins lost -95% or more from peak-to-trough. Bitcoin is currently off -84% peak-to-trough, though is attempting yet another dead cat bounce. My algorithms have called the few but very pronounced major tops and bottoms in bitcoin since 2011. I have discussed some of them here and here. They show bitcoin needs capitulation, if history is any guide, for a major bottom to be achieved. The current dead cat bounce in bitcoin as it approaches $4000 is only a little less dead than the prior dead cat bounces we have seen all year.  I have consequently been guiding investors since I went to cash on January 30, 2018, prior to the start of the crypto column here on VSI, but with mentions made since its launch to short or buy put options/CME futures on bitcoin.

I have consequently been guiding investors since I went to cash on January 30, 2018, prior to the start of the crypto column here on VSI, but with mentions made since its launch to short or buy put options/CME futures on bitcoin.

If bitcoin corrects -87% as it did in the last bitcoin bear market, it would be at $2950. Of course, there is no rhyme or reason why it needs to match the depth of the last correction. With the wave of regulations being passed into law in 2019, bitcoin could correct -94% which it has done twice before, and would suggest a price of $1180. $600 is also possible as this represents a full round trip when retail investors accelerated the price rise of bitcoin from $600 and up after Trump was elected due to renewed confidence. Thus, alternative speculative assets such as bitcoin came into favor.

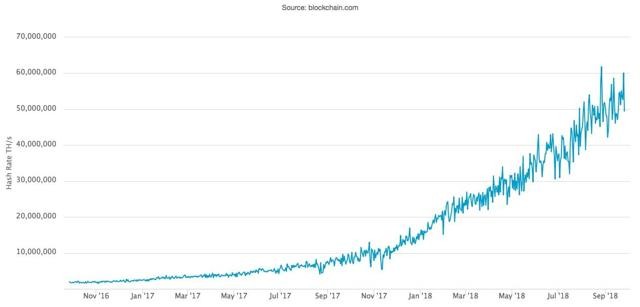

While a wave of regulations will be passed into law in 2019 which could be considered a major headwind, bitcoin's peer-to-peer transaction of value remains live and well as bitcoin's hash value continues to move higher despite the crypto winter this year.

In addition, 3 billion of the world's unbanked are coming online using bitcoin, and institutions ultimately will join in once regulations are set. In other words, regulations which at first will act as headwinds will ultimately be one of the biggest tailwinds for bitcoin and blockchain overall.

And as one of many examples that show how bitcoin and blockchain are being utilized, millions of families in Venezuela had been moving from their native currency into bitcoin starting in 2017 as well as dollars to keep their savings intact, but more recently this year, have been doing an end run around their government who outlawed the use of cryptocurrencies. Families are using the cryptocurrency Dash to move out of their native currency which continues to plummet. Dash which used to be known as Dark enables one to hide all transactions. It is then possible to convert Dash to dollars.

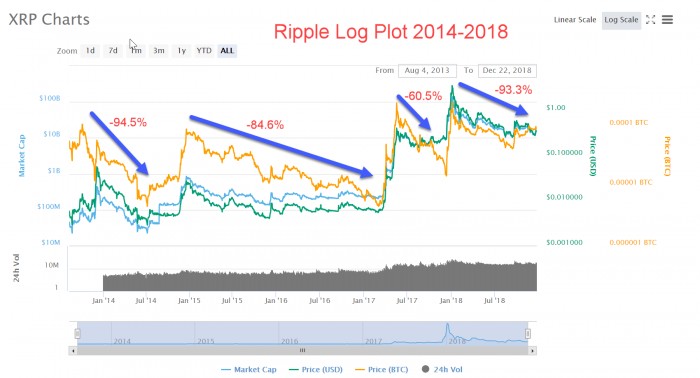

Since 2013, Dash's market value has gone from a few million dollars to roughly $12 billion (at its peak). It still has a value of around $750 million even after correcting -94%. That said, Dash and most other cryptocurrencies are no stranger to steep corrections. Dash and all other cryptocurrencies trading at the time had an equivalent correction back in 2014-2015. Ripple is a great example of having had numerous "devastating" corrections as it is one of the oldest cryptocurrencies. Yet it, together with bitcoin and other major cryptocurrencies, still refuses to 'die'. The correction percentages shown below represent the loss of value in dollars from peak-to-trough:

Regardless of what happens with stocks and cryptocurrencies, our website is about making money on the long or short side based on what individual stocks (and bitcoin via Crypto Reports) are showing. So whether the market is bullish or bearish, we always remind members never to get wedded to either side of the stock market, but to go with what their stocks are telling them to do. Our aim is to help investors learn to fish, thus provide ample guidance through our actionable reports and webinars on both the long and short side.